(Report Producer/Author: Minsheng Securities, Zhou Tai, Li Hang)

1 Thermal coal production is the main industry, and the coal chemical industry is growing rapidly

1.1 Yitai Coal: a large private enterprise integrating coal mining, coal transportation and coal chemical industry

The company mainly focuses on the production and sales of thermal coal, integrating coal transportation and coal chemical industry. Founded in 1997, Yitai Coal is mainly engaged in coal production business, which was exclusively initiated by Inner Mongolia Yitai Group Co., Ltd. and was established through the public offering of B shares. In 2001, the company's Yitai No. 1-8 coal products were certified by the China Quality Inspection Association. Since 2003, the company has begun to invest in the acquisition of railway transport companies, forming its own coal transportation capacity and expanding its business coverage. In 2006, the company established yitai coal-to-oil subsidiary, put into operation coal-to-oil project, and in 2009 trial operation, with coal chemical business extended downstream, to achieve the company's industrial upgrading. In the 2010s, a number of the company's pre-production projects have entered the formal operation stage and realized the realization of investment.

The actual controller of the company is an individual, holding a number of coal industry subsidiaries. The major shareholder of the company is Inner Mongolia Yitai Group Co., Ltd., which held 49.17% of the company's shares by the end of 2021; the actual controller is Zhang Shuangwang, who indirectly holds 18.39%. The company currently has 3 types of shareholdings, namely non-tradable domestic shares, 1.6 billion shares held by major shareholders, 1.328 billion B shares publicly issued, 326 million H shares listed overseas, and all three types of shares are ordinary shares of the company, and the shareholders enjoy the same rights, but they cannot be replaced or converted. The company has a number of coal-related industry subsidiaries, acid thorn gou mining company, Baoshan coal company, etc. engaged in coal mining, washing and production and sales; Huhuai Railway Company and Huaidong Railway Company engaged in coal railway transportation, of which Huaidong Railway Company was absorbed and merged by Huhuai Railway Company in 2019; in addition, Yitai Coal-to-Oil, Yitai Chemical, etc. are mainly engaged in the production and sales of coal chemical industry.

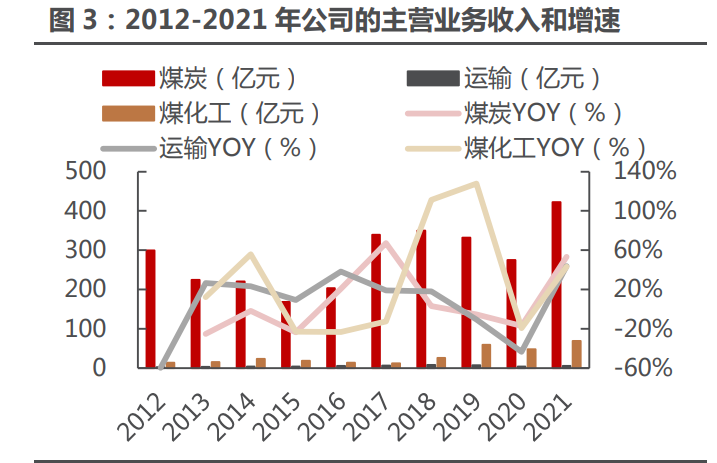

1.2 The contribution performance of coal business is elastic, and the scale of coal chemical revenue is expanded

The coal business is the main source of income, and the scale of coal chemical industry is increasing year by year. The company's main business includes the production and sales of thermal coal, the production and sales of chemical products such as coal-to-oil, and the provision of coal transportation services for third parties. Among them, the coal business revenue accounted for more than 80% continuously, which is the main source of the company's revenue. In 2021, the company's coal business revenue was 42.205 billion yuan, an increase of 53.24% year-on-year, mainly due to the high coal price in 2021, and the company's coal sales in 2021 actually showed a decline of 62.9105 million tons, a year-on-year decrease of 14.13%. Since 2017, the revenue scale of coal chemical business has grown rapidly, from 1.241 billion yuan to 6.901 billion yuan in 2021, with a four-year CAGR of 53.56%, and the proportion of revenue has increased to 13.87%.

The contribution of the coal business was mainly elastic in performance, and the gross profit margin of the coal chemical business declined significantly. The company's coal business contribution gross profit continued to maintain at about 90%, accounting for a relatively high proportion of 97.36% in 2021, the gross profit margin was basically stable since the supply-side reform, about 30% left and right; from 2015 to 2019, the gross profit margin of the coal chemical business fluctuated around the level of 15%, and the gross profit margin level in 2020 and 2021 fell sharply compared with the previous period, 2.36% and 3.88%, respectively, mainly due to the impact of the epidemic, and the longer shutdown period led to faster revenue and cost reduction. And the cost of purchased raw coal is high. In 2021, as oil prices rebounded, the gross profit margin of the coal chemical business rebounded.

1.3 The net profit margin has been significantly improved and the capital structure has been continuously optimized

Impairment impact 2020 net profit is negative, 2021 net profit margin reached a recent high. After the supply-side reform in 2016, the company's revenue has achieved steady growth, and the level of net profit margin has been basically stable. In 2020, the company suffered a loss due to the impairment of 3.078 billion yuan in the construction project of Xinjiang Energy Ganquan fort 2 million tons of coal-to-oil project; in 2021, after the sale of the long-term assets of the project, an impairment of 780 million yuan was recorded, and the net profit margin in 2021 was 17.06%. Excluding the impact of the impairment of Xinjiang Energy's 2 million tons of coal-to-oil project, the company's net profit margin for 2020-2021 is about 5.3% and 18.3%.

Capital expenditure and asset-liability ratios are on a downward trend. In 2017, in response to the supply-side reform policy, the company resolved excess capacity, replaced the capacity of the Tara Trench Coal Mine and the Acid Thorn Valley Coal Mine, and built the second line of the Huhuai Railway project, and the capital expenditure increased significantly, and then showed a downward trend. The company's asset-liability ratio has decreased from 60.73% in 2015 to 46.29% in 2021, and the capital structure is constantly optimizing. (Source: Future Think Tank)

2 The supply and demand in the short and medium term maintain a tight balance, and the policy supports the central increase in coal prices

2.1 Supply side: The supply of coal at home and abroad is limited, and the tight supply situation may continue

2.1.1 The increase in new domestic production capacity is limited, the elasticity of existing production capacity is weakened, and the pressure to ensure supply still exists

The industry's fixed asset investment showed a downward trend, and under the background of high capital cost + double carbon, the industry's willingness to build new production capacity weakened. After 2012, the industry's fixed asset investment continued to decline, and began to turn positive in the second half of 2018, with investment in 2021 increasing by 8.20% year-on-year, but the absolute value level was still lower than that in 2015. From the company's point of view, the cash flow of coal listed companies to purchase and build fixed assets is also at a relatively low level, mainly in the context of double carbon, coal consumption will show a downward trend, the company's new supply of heat is low, and the overall debt ratio of the industry is at a high level, the external financing cost is high, forming a certain capital constraint on listed companies; at the same time, the industry project construction cycle is long, the policy end control is strong, and the barriers to entry of new enterprises are high. Therefore, the industry's willingness to build new production capacity is weak, and the investment amount is expected to remain at a low level. Even considering the increase in production capacity from the current level on the industrial side, considering the 5-year construction cycle, it is expected that the growth of the industry's supply side will remain low in the next 5 years.

In 2021, the domestic capacity will exceed 30 million tons, and the capacity contraction is still in progress. At present, there are still a large number of small and medium-sized coal mines and mines with a production capacity of less than 600,000 tons on the mainland, which have outstanding risks and poor economic benefits, and are facing the problem of resource depletion. According to incomplete statistics, in 2021, the mainland coal production capacity will be withdrawn from 140 places, involving a production capacity of more than 30 million tons / year, and the average single well size is about 220,000 tons / year.

According to estimates, it is estimated that the new production capacity in the country will not exceed 100 million tons in 2022. According to incomplete statistics, we expect the supply increase of new production capacity from 2021 to 2023 to 78.11 million tons, 84.51 million tons and 102.83 million tons, respectively. Since the capacity utilization rate of backward production capacity is much lower than 100% due to resource depletion, we assume that the capacity utilization rate of backward production capacity is 60%. After offsetting the withdrawal from capacity, we expect the supply increase of new production capacity in 2021-2023 to be 60.48 million tons, 68.91 million tons and 89.03 million tons, respectively. Therefore, the new production capacity in 2022 may not exceed 100 million tons, and many production capacities have been trial produced when supply is guaranteed in the fourth quarter of last year, and the actual increase is limited.

The overproduction of coal mines that have not occurred but are in real danger is punished to limit the elasticity of the supply of existing production capacity, and some of the guaranteed supply and production are facing withdrawal. First of all, the "Criminal Law Amendment (XI)" stipulates that criminal responsibility shall be pursued for illegal acts that have not occurred in production accidents but are in real danger. This provision directly reduces the willingness of coal mine to overproduction, and the elasticity of the supply of stock capacity shrinks. Secondly, some mining areas rely on reducing maintenance to increase production, which cannot be maintained by itself, and the postponed suspension and maintenance after the Spring Festival is put on the agenda, and the capacity utilization rate of nearly 75% in 2021 is difficult to replicate in the short term. In addition, under the supply guarantee policy, the Inner Mongolia Autonomous Region approved the land use procedures for 38 open-pit coal mines in Ordos City that had previously stopped production due to incomplete land use procedures, involving a production capacity of 66.7 million tons per year. The approval of the guaranteed supply capacity is one of the factors for the production guarantee in 2021, and it is expected that it will be difficult to maintain the high output in the fourth quarter of 2021 in 2022, and from the perspective of coal production in Ordos City, the daily output has not yet recovered to the high point level at the end of 2021 after the low point of the suspension of production warranty in February.

The supply guarantee policy continued, the long-term price increased the gross profit level of the industry, and some of the negative sentiment of supply was alleviated, but the pressure of supply assurance still existed. In mid-March, the state proposed "four increases and one control" to further ensure coal supply, requiring 300 million tons of new coal production capacity in the country in 2022, daily output from 12 million tons to 12.6 million tons, and the benchmark price of the long-term association of 675 yuan / ton, an increase of 26.17% compared with the previous 535 yuan / ton, which is conducive to improving the industry's profitability center and alleviating some of the negative sentiment of supply. According to the coal market network and coal resource network data, from January to February 2022, the national raw coal output was 687 million tons, of which the cumulative output of Ordos City was 144 million tons, accounting for 20.98%, according to this proportion, when the national daily output was 12.6 million tons, the average daily output of Ordos was about 2.64 million tons, and in the first two months of 2022, the average daily output of Ordos was 2.44 million tons, excluding the impact of the low production factor of suspension and maintenance in February, the average daily output of Ordos in January 2022 was only 256 10,000 tons, the daily output continues to increase the space is limited, the pressure to improve production and supply is still large.

2.1.2 The international coal supply and demand relationship is tense, and the high price of coal will not decrease, and coal imports will decline

Overseas coal demand is strong, and the ability to regulate imported coal is weakened. After the implementation of the domestic price limit, the import coal price fell synchronously, and then in the second half of November 2021, there was a divergence with the domestic coal price, and the international coal price took the lead in rebounding, reflecting the strong demand for overseas coal market; since 2022, the domestic and foreign coal prices have risen synchronously, reaching a new round of highs in March, and the price of thermal coal in Australia and South Africa has reached 414.3 and 357 US dollars / ton, and the overseas demand has not decreased.

The essential factor of the continued high price of overseas coal is the long-term lack of capacity investment. For a long time, represented by developed countries in Europe, it has adhered to the strategy of de-coalization. In particular, ESG investment decisions have led to a long-term decline in coal investment. Since 2021, demand in the Asia-Pacific region has recovered, bringing with it a sustained strengthening of global coal prices. Since the fourth quarter, as prices such as natural gas have continued to reach new highs, European countries have generally begun to resume coal-fired power plants to stabilize energy shortages. In the medium and long term, it has ensured the high level of global coal prices.

The continued anxiety of the Russian-Ukrainian conflict will have an impact on Russian coal exports. Since February, the United States and many Western countries have imposed a series of sanctions on Russia, restricting Russia's energy exports to boost the economy on the one hand, and restricting the international financing ability of domestic enterprises on the other hand. According to logistics, in early March, the world's three major container shipping companies suspended bookings to and from Russian ports, namely Maersk, Hapag-Lloyd, and CGM, in addition, Mediterranean Shipping also suspended the booking of some goods. As the world's third-largest coal exporter, Russia's limited energy exports have exacerbated tensions in the global energy supply chain. At the same time, in the future, to get rid of the dependence on Russia's oil and gas resources, the countries represented by Germany and Italy began to have an energy substitution strategy, although the long-term plan is to increase new energy power generation, but the main measure in the short and medium term is to increase the use of coal-fired power plants.

Imported coal has no advantage over the price of domestic self-produced coal, and coal imports will be sharply reduced. The high international coal price makes imported coal inferior to the domestic coal price, and it is expected that coal imports will decrease sharply. In 2021, China's coal imports from Russia will be 54.5513 million tons, although the Russian energy department said that Russia's coal supply to China will increase to 100 million tons in the future, but compared with the perfect pipeline infrastructure and sea and land transportation construction of Western countries, Russia's exports to China will still be limited in the short term.

2.2 Demand side: A number of favorable policies have landed, and downstream demand has continued to be stable

2.2.1 At the beginning of 2022, the demand for thermal power continued to exceed expectations, and it is expected that the follow-up will increase steadily

Thermal power generation maintained a high proportion, and demand continued to exceed expectations。 In 2021, thermal power generation accounted for about 67%, and the proportion continued to decline, but still maintained a high share level. In 2021, the demand for electricity in the residential sector exceeded the historical trend, with a growth rate of 10.3%, while hydropower generation fell sharply, and the demand for thermal power exceeded expectations. In this context, thermal power generation in January-February 2022 still reached 986.4 billion kWh at a growth rate of 5.05%, and demand continued to exceed expectations.

From May to June, there will be a small peak of thermal coal replenishment. According to the data of Ordos Coal Network, as of March 28, the coal inventory of key power plants in the country was 70.44 million tons, a decrease of 7.52 million tons compared with the end of February; the coal inventory of Qinhuangdao Port was 5.05 million tons at the weekend, which was at a low absolute level, affected by the epidemic and power plant maintenance and other factors, the daily coal consumption of power plants decreased, and the enthusiasm for replenishment was low, but compared with previous years, the coal inventory of Qinhuangdao Port reached a low point and gradually recovered, and the inventory of Qinhuangdao Port began to show a rebound trend at the end of January this year. The willingness of coal enterprises to store inventory has increased, which also reflects that the decline in industry demand in the off-season is lower than expected, and downstream demand is relatively strong. Follow-up into May, as downstream demand once again enters the peak season, thermal coal will usher in a small peak of replenishment.

The total amount of energy consumption has been liberalized, and the demand for thermal power has increased steadily。 In January 2022, the State Council issued a plan related to energy conservation and emission reduction, which liberalized the total amount of energy consumption, relaxed energy consumption restrictions in areas with higher economic growth and lower energy intensity, and expected to increase downstream demand for coal. With the expected recovery of hydropower loads in 2022, the demand for thermal power will grow steadily, at a rate lower than 9.45% in 2021, and we expect to reach 5.8% in 2022.

2.2.2 The pace of real estate and infrastructure investment has accelerated, supporting the recovery of demand for construction coal

The goal of stable growth releases the "policy bottom" signal. Affected by factors such as the non-speculation of housing in the early stage, the monitoring of funds of key real estate enterprises and the financing management rules, the growth rate of real estate investment and infrastructure investment will continue to slow down in 2021. The two sessions in 2022 stressed that this year's work should adhere to the principle of being steady and steady, seeking progress in stability, macroeconomic policies should be steady and effective, micro policies should continue to stimulate the vitality of market players, structural policies should focus on smoothing the national economic cycle, and the expected GDP target is 5.5%. Due to the large uncertainty of consumption under the background of repeated epidemics, and the tightening of real estate in the early stage and the tight source of infrastructure funds, investment will become the focus of steady growth in the new year.

A number of real estate policies have been introduced, and the real estate market is expected to recover. In terms of real estate, the direction of regulation and control of real estate by the two unions has changed from "housing is not speculated, ensuring the housing needs of the masses" in 2021 to "housing is not speculated, exploring new development models, promoting the construction of affordable housing, supporting the commercial housing market to better meet the reasonable housing needs of home buyers, and promoting the virtuous circle and healthy development of the real estate industry due to urban policies" by the city. In late March 2022, the central bank launched a reverse repurchase of 700 billion yuan in five days to ensure stable interbank liquidity and maintain the investment stability of the capital market. At the same time, since February, many regions have received the signal of the meeting released by the Political Bureau of the CPC Central Committee in late 2021, and have successively introduced a number of measures such as reducing mortgage interest rates, giving loan support to housing enterprises, and streamlining the approval procedures for housing construction projects. The two sides of real estate supply and demand go hand in hand, and the market may usher in a recovery.

The role of fiscal leverage in infrastructure investment has been significantly strengthened, and infrastructure investment will usher in a turnaround. In March 2022, the Fifth Session of the 13th National People's Congress proposed to actively expand effective investment, moderately advance infrastructure investment, and build key water conservancy projects, energy bases and other facilities in terms of projects; in terms of funds, the amount of special debt issued in advance is 1.46 trillion yuan, and it is expected that 1.4 trillion yuan of special debt projects under construction in 2021 will be carried forward to continue construction in 2022, and both amounts will reach the highest scale in history, ensuring that infrastructure investment will rise steadily in the new year.

Steel and cement benefit from the recovery or marginal improvement of the real estate and infrastructure industries, and the demand for upstream coal will grow steadily and synchronously. In February 2022, the Ministry of Industry and Information Technology, the National Development and Reform Commission and the Ministry of Ecology and Environment jointly issued the Guiding Opinions on Promoting the High-quality Development of the Steel Industry, which delayed the carbon peak of the steel industry by 5 to 2030. In terms of cement, it reached its peak in 2014 and then entered the platform period, with growth rates fluctuating between plus and minus 6%. Taking into account the support of steel and cement demand supported by the recovery of real estate and infrastructure, the demand for construction coal will grow steadily in 2022. We expect steel and cement production to grow by 1% in 2022.

2.2.3 Favorable policies + high oil prices, coal chemical industry advantages are significant

Modern coal chemical industry is developing rapidly, and coal-to-chemical production capacity accounts for a relatively high proportion. With the gradual improvement of the importance of coal chemical industry under the background of internal circulation, the modern coal chemical industry in mainland China has developed rapidly, and China has the world's leading level of large-scale coal gasification, million-ton coal direct liquefaction and other industrial technologies. According to the data of the new energy network, as of 2020, the four major types of production projects such as coal-to-oil, gas, olefins, and ethylene glycol have completed a cumulative investment of about 606 billion yuan, produced 26.47 million tons of major products, converted about 93.8 million tons of coal (standard coal) per year, and achieved annual operating income of 121.2 billion yuan. Among them, the operating rate of coal-to-natural gas and coal-to-olefins in 2020 will exceed 90%, the coal-to-ethylene glycol production capacity will account for 38.1% of the country's total ethylene glycol production capacity, and the coal (methanol) route ethylene and propylene production capacity will also account for 20.1% and 21.5% respectively. According to the "China Petroleum and Chemical Industry Observation", the current output of modern coal chemical products has reached 40 million tons of crude oil equivalent, more than 1/5 of domestic crude oil production in 2021. The enthusiasm for the production of coal chemical products is relatively high, and the industry is developing rapidly.

Raw material energy consumption is not included in the total energy consumption control + the "14th Five-Year Plan" output target doubled, which is conducive to the development of the coal chemical industry。 In january 2022, the State Council issued the "14th Five-Year Plan" comprehensive work plan for energy conservation and emission reduction, which proposed that the use of raw material energy should not be included in the national and local energy consumption dual control assessment. In coal chemical coal, the proportion of raw materials is higher than the proportion of fuel, and the liberation of raw material energy will help promote the coal chemical industry to drive the demand for raw coal upstream. In addition, according to the "14th Five-Year Plan" Development Guidelines for Modern Coal Chemical Industry, the development goals of the "14th Five-Year Plan" coal chemical industry are: 30 million tons / year coal-to-oil, 15 billion cubic meters / year coal-to-gas, 10 million tons / year coal to ethylene glycol, 1 million tons / year coal to aromatics, 20 million tons / year coal (methanol) to olefins by 2025. The policy is good for the coal chemical industry, and there is sufficient space for the development of coal chemical industry.

The background of high oil prices stimulates the substitution effect of coal chemical industry on petrochemical industry. Coal chemical products and petrochemical products have high overlap, and when the international crude oil price is low, coal chemical products do not have a price advantage. According to the Shenhua Institute of Science and Technology, the price of oil that puts coal-to-oil and coal-to-chemicals at the break-even point ranges from $45 to $65 per barrel. Since 2021, the overseas economy has recovered, international oil prices have continued to rise, and the growth momentum in 2022 has not decreased, has exceeded 90 US dollars / barrel, the current oil price level makes coal chemical tools have strong competitiveness, and accelerate the development of the coal chemical industry. It can be seen from the operating rate of olefins that before the strict implementation of the dual control of energy consumption, the operating rate of olefins continued to be higher than that of the same period last year, and the operating rate of olefins rebounded rapidly after the relaxation of power curtailment.

Considering that the use of raw material energy is liberated from the dual control of energy consumption, the operating rate of new coal chemical industry is expected to increase in 2022, while the construction space of coal chemical industry during the "14th Five-Year Plan" period is still large, and the increment and stock will contribute to the demand for coal consumption at the same time, and we expect that the coal chemical industry will increase by about 15% in 2022.

2.3 There is still a short-term gap, and the price center is about 1100 yuan / ton or more

According to the relevant data of the coal resource network and the relevant assumptions above, we expect the total coal demand in 2022 to be 4.554 billion tons, an increase of 4% year-on-year, and the supply gap still exists; the average price of thermal coal in Qinhuangdao Port in 2022 is expected to be about 1100 yuan / ton, an increase of 28% compared with the average price of 857 yuan / ton in 2021. (Source: Future Think Tank)

3 The profitability of the coal business has been enhanced, and the coal chemical industry has helped to achieve performance thickening

3.1 Abundant coal reserves, new production capacity to consolidate the leading position of regional coal private enterprises

The output ranks in the forefront of the region and is the leader of coal private enterprises in inner Mongolia Autonomous Region. According to the sample coal mine production data statistics of the coal market network, the company's coal production in 2021 will account for 6.85% in the Inner Mongolia Autonomous Region, and shenhua group, Huaneng Hulunbuir, Huo coal group and Pingzhuang coal industry with higher output in the autonomous region are all state-owned enterprises, while the actual controller of Yitai coal is Zhang Shuangwang, a natural person, and the company maintains a regional leading position in the private coal enterprises in Inner Mongolia.

The company's approved production capacity is 38.6 million tons / year, and the excellent and low-quality coal structure strengthens the anti-risk ability. As of the end of January 2022, the company has 9 holding coal mines in normal operation, of which 7 are in production coal mines, including the acid thorn ditch coal mine with an approved production capacity of more than 10 million tons; there are 2 coal mines under construction, the Baijialiang coal mine is in the stage of technical transformation, the approved production capacity will increase by 300,000 tons to 900,000 tons / year, and the Almale integrated mine is a new coal mine with an approved production capacity of 4.5 million tons / year. The total approved production capacity of coal mines in production is 38.6 million tons per year, and the equity production capacity is 29.96 million tons per year。 The main mine coal type calorific coverage of less than 5000 to more than 6000, diversified coal varieties are conducive to strengthening the company's ability to resist risks.

Disaster control projects are expected to produce more than 10 million tonnes in 2022. Coal mine disaster control projects are mainly aimed at goaf coal mines, because of the geological conditions or the original technical conditions of the coal mine, there are still coal pillars in the ground after the goaf of this type of coal mine, and more coal resources can be obtained by digging up the surface of the coal mine. Disaster control generally adopts the method of open-pit excavation, and the specific steps are - open-pit excavation, backfilling, peeling pits, and reclamation management. There are no capacity restrictions on coal mines for disaster control, and their coal mining rights come from temporary land and other formalities。 Since the disaster control project is different from the well mine and the open pit mine, and is generally within the original mining area, if the mining area and the original mine do not overlap during the project, the two mining can be carried out at the same time. In 2019, the company's coal output was 56.41 million tons, far exceeding the approved production capacity, because well mining and disaster control were carried out at the same time. At present, the company's Narinmiao No. 1 and No. 2 wells and Baijialiang coal mines have entered the disaster control period, considering that the recoverable reserves of the Narinmiao No. 2 well and the Baijialiang coal mine can still support their existing production capacity mining for more than 5 years, therefore, it is expected that the Narinmiao No. 2 well and the Baijialiang coal mine will follow the same way of well mining and disaster control, and the recoverable reserves of the Nalinmiao No. 1 well are still 11.25 million tons, so we expect that the three disaster control projects in 2022 will bring more than 10 million tons of production.

The 4.5 million tonnes of capacity under construction at the Almar coal mine will contribute incrementally in 1-2 years. As of the end of 2021, the company's new integrated coal mine (open pit part) and coal preparation plant project in the Yining mining area is 40.9%; in January 2022, the project obtained the approval of the Ministry of Ecology and Environment of the People's Republic of China, and obtained a mining license in March, and the coal type is mainly non-stick coal with a calorific value of less than 5,000 kcal. According to the Tara Trench Coal Mine production timeline - mining license received in 2015 and trial production in 2016, it is expected that Almar Coal Mine will start trial production in 2023 and gradually release production of 180, 360 and 4.5 million tons in 2024-2026.

3.2 Strong cost control + long-term price center moved up, and the gross profit margin of tons of coal may be further improved

Endowment advantage + technical advantage to reduce costs and improve efficiency, the gross profit margin of tons of coal continued to rise. The geological conditions of the company's mining area are superior, with stable surface conditions, simple geological structure, shallow burial depth of coal seams and small inclination angles, relatively thick coal seams and low gas concentrations, which reduce the difficulty of mining and reduce production costs, and greatly reduce safety risks. The raw coal quality of the company's coalfield is better, the average ash content of coal production is about 12.49%, the average sulfur is about 0.34%, the average high calorific value is about 6100 kcal/kg (about 25.50 MJ/kg), compared with the national standard - 10.01% ~ 20.00% is low ash, less than 0.50% is ultra-low sulfur, 24.31 ~ 27.20 MJ / kg is the medium and high heat value, the company's coal coal quality is better, washing cost is small. In addition, the company's coal mines have achieved mechanized mining, mining equipment and mining technology advanced, recovery rate of more than 80%, mining efficiency is high, at the same time, the company has completed the acceptance of the construction of intelligent mines in the acid thorn ditch coal mine, and accelerated the promotion of Tara trench coal mine, Kaida coal mine and other intelligent construction, to further achieve cost reduction and efficiency. Under the company's cost control, the cost of tons of coal is basically stable, and it is currently at the average level of the industry; from the perspective of gross profit margin, the company's gross profit margin of ton coal is stable and rising, and its ability to resist volatility is strong.

The proportion of long-term associations remains at a high level, and the profit center benefit policy is expected to increase. The company's 2012-2020 price per ton of coal is relatively stable, maintaining a range of 280-420 yuan / ton. In 2021, affected by the large increase in the market price of coal, the company's price of coal per ton reached 671 yuan, an increase of 78.45% year-on-year. As we infer that the industry supply and demand gap still exists in 2022, the price center has moved up by 28%. Since the company's long-term association accounts for about 80%, and considering that the state encourages the proportion of long-term cooperation to increase, therefore, assuming that the company's coal sales in 2022 account for 90% of the long-term association and the spot account for 10%, based on the long-term benchmark price and the expected market price, respectively, the average sales price of ton of coal is expected to reach 718 yuan / ton.

3.3 The distribution network is complete, and the low-cost transportation business has formed multiple revenue points

The railway transportation capacity exceeded 200 million tons / year, supporting highways and container stations, and the transportation and marketing network was perfect. The company has 3 holding railways with an annual transportation capacity of 220 million tons / year, covering the company's main mining areas, forming a transportation network centered on the Jungar and Dongsheng coalfields, connecting the Dazhun and Daqin lines in the east, the Dongwu line in the west, the Beitong Jingbao line and the Nanda Shenshuo line. Among them, the special railway line of the Acid Thorn Gou Coal Mine takes the Acid Thorn Gou Coal Mine as the starting point and ends in Zhoujiawan, and forms an external transportation channel by docking the Zhuandong Railway and the Huzhun Railway; the Zhundong Railway directly connects the company's coal mine in dongsheng coalfield to the Dazhun Railway and the Huzhun Railway in Zhoujiawan, and then connects to the Daqin Railway through the Dazhun Railway, leads to Tianjin Port, Qinhuangdao Port and Caofeidian Port, and connects to the Beijing-Baotou Line through the company-controlled Huzhun Railway, leading to major markets such as East China and North China.

In addition, the company has built a 150-kilometer mining area road with Caoyang Highway as the main line and radiating the surrounding mining area in the Narinmiao area, which is rich in high-quality coal, and the company's railway system cooperates with the company to ensure smooth transportation. At the same time, the company has established or leased 10 container transport stations along the Beijing-Bao, Baoshen, Dazhun, Huzhun and Zhundong railways, set up freight yards and transshipment stations in Qinhuangdao, Jingtang Port, Caofeidian and other ports, and set up sales agencies in Beijing, Tianjin, Shanghai, Guangzhou and other places, forming a complete marketing system of production, transportation and sales.

The construction of the transportation system has led to the growth of purchased coal sales and transportation charges, and the low-cost business has helped the company achieve multiple revenue points. In 2012, the company completed the construction of the second phase of the Zhuandong Railway, further improved the transportation capacity, and achieved simultaneous growth in the sales of purchased coal, which supplemented the company's coal supply when the company's own coal production was low and expanded the company's revenue sources. In addition, the company's transportation business is also developing steadily, in 2021 the company for the third party transportation of coal is 35.22 million tons, accounting for 40.23% of the total railway transportation; at the same time, the revenue and gross profit of the transportation business showed an upward trend, at present, in addition to the 2020 epidemic impact gross margin decline is obvious, the company's transportation business gross margin level is basically stable at about 40%.

3.4 Coal-chemical integration has synergistic advantages, and the output of coal chemical industry under the background of high oil prices is expected to increase

The company's 3 coal chemical projects have been put into operation, and 6 projects to be put into operation are being promoted. At present, the company's Yitai coal-to-oil and Yitai chemical subsidiaries' 160,000 tons/year coal-to-oil project and 1.2 million tons/year fine chemical project, and Sun Company's Yitai Ningneng 500,000 tons/year Fischer-trophic hydrocarbon fine separation project have been put into operation. In 2021, the company's coal chemical revenue was 6.901 billion yuan, and the gross profit was 268 million yuan. In addition, the company began to lay out the coalification industry chain in Xinjiang, the integrated mine in the Yining mining area acquired mining rights in 2022, and the Yili energy subsidiary filed 4 coal-to-oil downstream extension projects with high carbon alcohol, alkylbenzene, Fischer-Tropsch wax, stable light hydrocarbons and liquefied gas modification. In addition, Yili Energy's 1 million tons/year coal-to-oil demonstration project was suspended in 2020, and the company is currently conducting research and demonstration of products and seeking strategic partners, and the progress of the project is relatively slow.

In the short term, itinine can still have room for production release. Since 2017, the company's coal chemical business revenue has maintained rapid growth, in 2019, due to the 1.2 million tons of fine chemicals project and 500,000 tons of Fescher-Tropsch alkane fine separation project officially put into production, the company's revenue and gross profit to achieve a significant increase, in 2021, the two projects produced 959,700 tons of chemicals and 273,300 tons of chemicals, in 2022, the background of high oil prices, it is expected that the project output will increase, driving the growth of coal chemical business revenue.

The completion of the Almarles coal mine in the medium term may lead to a further recovery in gross profit margin. From 2016 to 2019, the company's gross profit margin was basically stable at a level of about 15%, and in 2020, due to the impact of the epidemic, the sales price of coal chemical products fell, the revenue reduction rate was faster than the cost, and the gross profit margin fell significantly; in 2021, due to the high cost of purchasing raw material coal, the gross profit margin was still at a low level. About 80% of the company's current coal chemical raw material procurement comes from external enterprises, and the cost of raw coal purchased is much higher than the unit production cost of self-produced coal. In the future, with the gradual release of integrated mineral energy in the Yining Mining Area, the cost of raw materials for the coal chemical business is expected to decline, bringing about a further recovery of gross profit margin.

4 Stable operating ability, strong willingness to dividend

The dividend payout ratio is stable at about 30%, and the company's willingness to pay dividends is strong. Since 2012, the company's cash dividends have fluctuated greatly, mainly in the macro context of frequent mine safety accidents and capacity reduction, but the company's dividend payment rate has basically stabilized at about 30%. In 2020, the company's performance showed a loss, with a net profit of -781 million yuan, but the company still paid cash dividends, with a total dividend of 893 million yuan; in 2021, benefiting from the rise in industry prosperity, the company's dividend payment rate increased to 35.21%, and the total cash dividend was 3.026 billion yuan, and the dividend per share was 0.93 yuan, showing that the company's willingness to pay dividends was strong.

Compared with the same industry, the company has strong operating ability, high dividend frequency, and dividend yield is higher than the industry average. The company's profitability in the industry is relatively leading, compared with other thermal coal enterprises, the company's ROE level is basically maintained as positive, and the fluctuation is relatively small, the company's ROE in 2021 is 23.38%, compared with the industry's large state-owned enterprises China Shenhua and China Coal Energy nearly 10pct higher. From the perspective of dividend payment rate level, the company's dividend payment rate is lower than That of China Shenhua, but basically remains around the industry average, and compared with other regional coal companies, the company has carried out cash dividends every year, of which, in 2020, the company's net profit due to asset impairment losses is negative, but cash dividends are still at a high level, the total dividend is 735 million yuan, if the impact of asset impairment is excluded, the company's dividend payment rate in 2020 is about 40.73%, the company's dividend frequency is higher, and the willingness to pay dividends is stronger. From the perspective of dividend yield level, since 2015, the company's dividend yield has basically shown an increasing trend, and continues to be higher than the industry average, benefiting from excellent operating performance in 2021, and the company's dividend yield reached 10.99%.

5 Profit forecasting and investment analysis

5.1 Profit forecasting assumptions are split from the business

1) Coal business:

Output: 2022-2023 is expected to be new capacity has not yet been released, in 2020 and 2021 local investigation and punishment of illegal production led to low output of the company, assuming that the capacity utilization rate in 2022-2023 increased to 95%, disaster treatment projects brought output of 10 million tons; in 2024, Almale coal mine began to put into operation, according to the assumption of capacity utilization rate of 40%, 80%, 100%, it is expected to release an annual output of 1.8 million tons in 2024. We expect the company's coal production in 2022-2024 to be 4667/4667/48.47 million tons, respectively.

Sales volume: Assuming that the production and sales rate of self-produced coal is 100%, we expect the company's self-produced coal sales to be 4667/4667/48.47 million tons in 2022-2024; in terms of purchased coal, we expect that under the background of high coal prices, the company may use transportation advantages to increase purchased coal sales, assuming that the sales volume of purchased coal in 2022-2024 is 2068/2151/2194 million tons. Therefore, the company's total coal sales volume from 2022 to 2024 is 6735/6818/7041 million tons.

Unit price: As the benchmark price of the Long-term Association rises from 535 yuan / ton to 675 yuan / ton in 2022, the company's price center has benefited. Assuming that the company's long-term association accounts for 90% and the market price is 1100 yuan / ton, the company's coal sales unit price will increase to 718 yuan / ton in 2022; the growth rate of the price will slow down in 2023 and 2024. We expect the company's coal sales unit price to be 718/732/739 yuan / ton in 2022-2024.

Unit cost: It is expected that the rise in fuel coal, electricity prices and other expenses will increase the cost of raw materials, assuming that the unit cost of self-produced coal will increase by 8% in 2022; with the slowdown in industry growth and the intelligent construction of the company's coal mines, it is assumed that the unit cost growth rate of self-produced coal will decline in 2023 and 2024. We expect the unit cost of self-produced coal from 2022 to 2024 to be 234/239/236 yuan, respectively. Assuming that the purchase discount of purchased coal in 2022 is the same as that in 2021, and the market price is 1100 yuan / ton, the growth rate of purchased coal costs in 2023 and 2024 will decrease year by year, so the estimated unit cost of purchased coal in 2022-2024 is 699/713/721 yuan, respectively。

Based on the assumptions of production and sales, unit selling price and unit cost of the coal business, we expect the coal business to receive 48.3/499.0/52.05 billion yuan in 2022-2024, respectively, with a year-on-year growth rate of 14.5%/3.3%/4.3%, respectively.

2) Coal chemical business:

Considering the continuous increase in oil prices in 2022, it is expected that the company's coal chemical business revenue will maintain a high growth rate in 2022. Look at the sub-projects:

The 160,000-ton coal-to-oil project was put into operation earlier, and the project entered a mature stage, assuming that the revenue growth rate from 2022 to 2024 was 8%/3%/1% respectively;

The 1.2 million tons of fine chemicals project was put into trial production in 2018, officially put into production in 2019, and the chemical production in 2021 was 960,000 tons, and it is expected that the output in 2022 will increase to drive the project revenue growth, assuming that the revenue growth rate in 2022-2024 is 20%/5%/2%;

500,000 tons of Fischer-Tropsch alkane fine separation was officially put into operation in October 2019, the output is only 74,000 tons, 2020-2021 is 206,000 and 273,000 tons, respectively, is expected to be further increased in 2022, and the background of high oil prices is superimposed, it is believed that 2022 can continue the high growth rate in 2021, assuming that the revenue growth rate in 2022-2024 is 60%/10%/5%, respectively.

3) Transportation business: Due to the good prosperity of the industry, it is expected that the company's transportation business revenue will grow steadily, with an increase of 10.0%/8.0%/5.0% in 2022-2024, and revenue of 6.5/7.0/740 million yuan, respectively.

On the whole, we expect that from 2022 to 2024, the company's main business income will be 57.6/598.1/62.28 billion yuan, respectively, an increase of 15.9%/3.7%/4.1% year-on-year.

(This article is for informational purposes only and does not represent any of our investment advice.) For usage information, see the original report. )

Featured report source: [Future Think Tank]. Future Think Tank - Official website