Source: Content compiled by Semiconductor Industry Watch (ID: icbank) from stratechery, thank you.

Recently, foreign media stratechery interviewed Intel CEO Pat Gelsinger (PG). In the interview, there is not only a discussion about competitors, but also an analysis of the company's future, which we have excerpted below for your reference.

The following is a condensed version of the interview:

Stratechery: Pat, it's nice to talk to you. Thank you for taking the time. Last week, AMD briefly surpassed Intel in terms of market capitalization, and I think Nvidia is even more so than before, and none of these companies make their own chips. It's a bit like Jerry Sanders saying ,"Real men own factories!" The opposite of " When you came back to Intel and considered your strategy, did you ever consider going the same way: becoming a fabless company and leaning towards your design?

Pat Gelsinger: Let me give three different answers to this question, and as we go along, those answers will become more sensible.

The first one was that I wrote a strategy paper for the board and I said that if you want to split the company in two, then you should hire a PE type of person to do it, not me. My strategy is to become IDM 2.0, which I described. So if you're going to hire me, it's strategy, and 100 percent of the board of directors asks me to be CEO and supports the strategy I've developed, and that's one of them. So the first thing is that all the discussions happened before I became CEO, so there was no debate, no contemplation and so on, and that's it.

Second, let's think about it. Let's ignore the fact that we already have an IDM 2.0 strategy in place and let's use AMD as a case study for the time being. When did they sell their fabs? 2008. Good. So how many years has AMD been a huge success?

So it took them 11 years to get to that level, so I just want to say that in those 11 years, when they spun it off, there was an important promise that the company that became GlobalFoundries would be their leading supplier of process technology.

GlobalFoundries failed to stay at the forefront of technology in the process, and now, they're clearly the second-tier established node foundries in the industry and doing a great job, but they're having to redefine their business model because they can't compete with TSMC or be part of the Big Three, which I call Samsung, TSMC and Intel are in the lead.

So the strategy they originally envisioned — to spin off the company and make it their leading supplier — has failed, and even lawsuits have been filed between them to clean up the mess because they can't stay ahead of the curve and they have to basically follow.

At the same time, I also believe that Apple has made TSMC a viable leading foundry. I can argue that if that hadn't happened, we still wouldn't have a leading, viable foundry at TSMC. Apple drives their success in volume and capacity.

Second, the strategy they envisioned when they disintegrated was a failure. Today, AMD is successful as a fabless supplier, but not because of spin-offs, but because they were able to essentially create a second entity and rely on TSMC, so I would say that the proof point of this strategy is zero. They're a successful company now, but not because they spun off into a fabless back then.

And then the third, when we look at this, for me, it's almost a global national perspective, because I'm convinced that the West needs a world-class technology provider, and I don't think that splitting Intel in two can survive for many, many, many years until it becomes like that and you can stick with it. Remember, given that cash flow, R&D flow, products that allow us to drive that, I'm committed to fixing it, and I think we're on a good path to fixing it because I've been here as well. So, for these three different reasons, we chose the IDM 2.0 path, but not because we didn't consider alternatives, partly because we did.

Stratechery: I think you made Intel's geopolitical importance clearer than ever at the Intel Investor Conference, and you just reiterated that, and obviously that played a role in getting things like the U.S. Chip Act passed and things like that, but I'm curious to see how much of a role it has played in talent acquisition?

PG: It's an angle, but most engineers come up because the work they do is cool. That's part of the reason we're here, but if you ask my CFO Dave Zinsner. If you ask my head of personnel Christy [Pambianchi]. Even people like Nick [McKeown] are here to change the network. So I would say it's a factor. It's not the most important, but it's on the list of why people come back, and there's a lot of comments that I get from people – sometimes what makes me angry is stocks falling, investors being negative, and everyone is cheering for us. "Oh, Pat, you have to succeed!" "Well, buy my stock. (Laughs) If you're going to say something, put your money to your lips", but our enthusiasm for success couldn't be higher.

Even people who say, "Hey, I'm not sure Pat can do that. I'm not sure, two or three years is dead money," wait, "but oh, of course I want him to succeed." ”

Stratechery: Including Intel Foreign Media, more and more manufacturers are outsourcing their products to TSMC. In your investment presentation, there is one of your future architectures, the CPU chip is N3, which is TSMC nomenclature.

What intrigued me was the double benefit that Intel gets from it, on the one hand, you get the fastest process in the industry right now, and on the other hand, Intel is forced to adopt these industry-standard tools and methods, which Intel talked about before, but now you have no choice if you want to be modular. You can't rely on integration and collaboration with manufacturing to solve problems, but it also gives manufacturing a wake-up call because if the design team is an external customer, they can't get the design team to bend to their wishes, and now, if it's an internal customer, they can't do it either. Or, in a suboptimal situation where you have to outsource something like this, is this too much of a silver lining?

PG: No, it's not. This is part of my conscious strategy because I have a slide in my slide saying that IDM makes IFS better and IFS makes IDM better.

That's part of it. Some of the things I say are, "Hey, IDM makes IFS better." At that level, it could basically inherit $10 billion in research and development for free. Huge capital expenditures and so on make IFS possible, but IFS also makes IDM better, which is exactly why you describe it. I don't have to benchmark my TD team, my IFS client is doing it for me. I find some of these conversations interesting. We've talked about these five whale customers and these are all positive conversations. The active, everyday thing, the team is now saying, well, what about the ultra-low voltage threshold of the thin-pitch library that we're going to use in this particular unit? "TSMC gave us these characteristics, and you didn't portray that corner." Well, guess what? Go to the Characterization Corner! "Your PDK is not as powerful as Samsung or TSMC's PDK and cannot describe the process technology my team simulated." Well, guess what? You know, all of this is described in conversations that make my TD team better and make my design team more efficient because they're going to push my TD team before to say, "Hey, we need a low-profile battery library" and they're not going to get it.

Because it didn't become mainstream in processors. It's kind of like, "Hey, here are some use cases." Well, now they understand that all of this is pushing us to get better. So in some ways, in a less subtle way, I released market forces to break down some of the NIH of Intel's core development machines, which is part of ifS making IDM better.

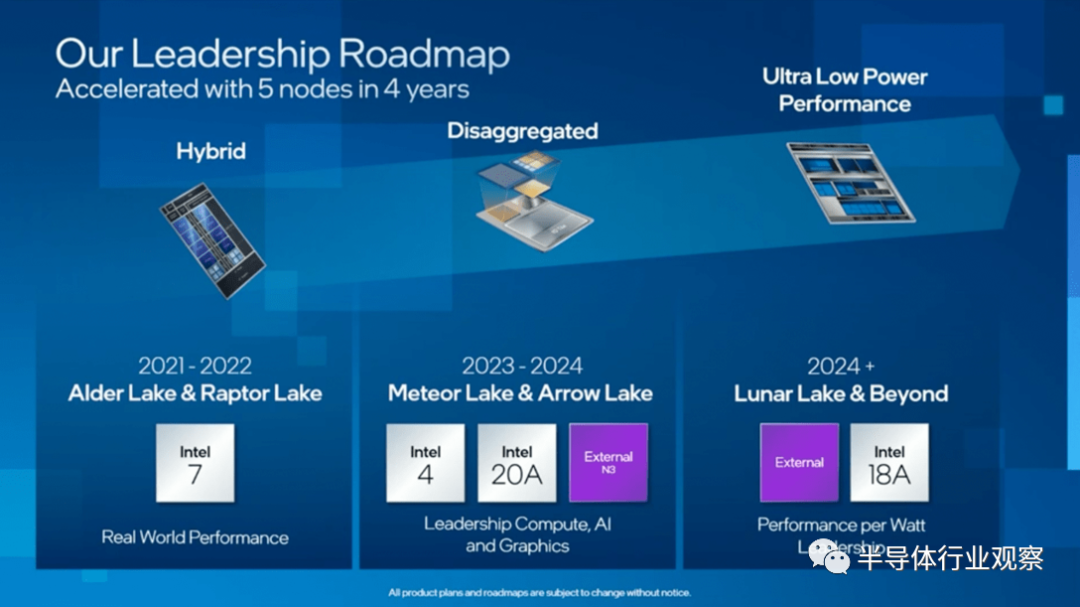

Stratechery: Yeah, that makes a lot of sense. You have this super radical roadmap, five nodes in four years, and I have two questions about that. The first one goes back to what you mentioned earlier about Apple being a partner of TSMC to get to the next node and how important it is for TSMC. I think I noticed that in this new Tick-Tock strategy, Tick-Tock 2.0, Intel's role is intel pushing it and then opening it up to your customers. I think it's an example of how Intel as the same company can really benefit itself, you can play the apple role that Apple did for TSMC, you just have to play for yourself.

PG: Yeah, well said. Now let's say, because I expect the Intel 18A to be a really good foundry process technology – I'm not against customers using the 20A, but for the most part, most customers don't want to experience that kind of pain on the front end. So usually my in-house design team pushes for things like those groundbreaking painful early product lines, much like the Apple character that TSMC also benefits from. Now, if Apple shows up and says, "Hey, I want to do something in 20A," I'd say yes.

If you list them, there are ten companies that can play this role – Qualcomm, NVIDIA, AMD, MediaTek, Apple, and they're really driving these front-end design cycles, and if one of them wants to do that on Intel 4, I'll do that, but I hope Intel 3 is a better node for most foundry customers, just like Intel 18A is a better node for most foundry customers.

Stratechery: I think it's just Apple, and I think that's actually one of the strong reasons Intel itself is doing this, and frankly, it's beneficial to have TSMC join Intel as a counterpoint.

One more thing, in a way, wouldn't it be nice to get second place? You did highlight a lot about how you can learn from and benefit from vendors in ways that Intel didn't have before, and I do want to dive into that. These vendors have learned a lot from TSMC and Samsung – and you believe you can learn from your vendors, to what extent do you believe you can really achieve this super radical rate of progress?

PG: It's a meaningful benefit. My team doesn't like the idea of finishing second in a competition, so they're very enthusiastic. We do believe that at 18A, we are undoubtedly back in a leadership role, but as an example, keeping the EUV healthy on Intel 4 is due to the fact that TSMC and ASML have also driven the learning curve up. I just asked ASML, "How many layers I have on the EUV per day, are they competitive?" ” 。 If not, why not? I would say that we are now having a very heated debate on such issues. "Well, the way they measure it is different from the way we measure it" and "How do you measure downtime and maintenance windows and all that sort of stuff," I thought, "Hey, I don't care." Show me these damn stats. You know, I went to AsML's Peter [Wennink] and Martin [van den Brink] and asked, "How are we doing?"

Stratechery: One of the very interesting things about Intel is that before that, since you didn't have a foundry business, you couldn't make a lot of money on an old foundry that was depreciated and produce something almost purely profitable. Instead, Intel has taken a different strategy of reusing the device and reusing it to the next node, and rolling back into the design because they have to adapt to longer device usage and so on, and I think from my point of view, that's one of the reasons Intel runs into a wall because they're dragging a lot of old devices, so it's not the most advanced.

My question is, when you look back at the history of wall-hitting, there are obviously a lot of factors that contributed to this, but do you think it's even possible to just do IDM like Intel? Or is it so hard to be at the forefront right now that you really need to start over every time? This means that in order to be profitable, you need to keep all past processes in use for a longer period of time, which is by definition a foundry business. Everything else, EUV delays, things like that, can Intel's old strategy be stopped being enforced?

PG: Well, I think it's possible. I think if Intel hadn't messed up at 14nm to 10nm, I think they'd still be doing well and we wouldn't be in such a tight state of crisis. That being said, what lies ahead of us is a better business model and we will seize it. I do think we've made some bad device choices because we're reverting to new places where we should be. If we had a natural path of operation for these processes and equipment, I think we would have less burden on the front end, so I think that hurts us in that regard. I do think the idea of minimizing equipment turnover by trying to roll from 17 to 14 to 10 that you know is a bit problematic for companies. "We know how to make this tool work, we know how to do qual patterns, so we don't need those crazy EUV stuff." But you know, I don't think the business model has been fundamentally broken. Intel has failed to continue to execute it well, partly driven by these isolated natures.

The first time I met [TSMC CEO] CC [Wei], he said, "Pat, you really make me angry. You make money on the front end of the technology. ”

I said, CC, you me off. You make money on the back end of the technology! By the way, we now do both. We're both doing it now. TSMC has raised its price sharply in the front-end node, and he is now pricing him to make money on the front-end, which he didn't do before, while I added a foundry on the back-end, and I'm making money in the back-end node moving forward. So in a way, we're all modifying our business model. By the way, this is such a large and expensive business that it is suitable in both directions.

Stratechery: The acquisition of Tower made a lot of sense to me because Intel not only needed to flesh out the portfolio it had as a foundry, especially in terms of simulation, but it also needed to build the ability to serve external customers. That's why I'm cheering at some point for a potential acquisition of Intel GlobalFoundries. While they don't have a lead, in your opinion, they've spent 14 years figuring out how to serve external customers and build IP around those things. Tower does meet some of those needs, but my concern is that it's much smaller than Intel, so how do you capture the customer service part you need without being suppressed by Intel culture?

PG: Was Tower merged into Intel Foundry or Did Intel Foundry merge into Tower?

The answer is that the latter is more than the former. I've said I would totally like to merge these businesses together, but that doesn't mean it's a small satellite under what we started at IFS. We're going to put that together, and I fully expect the result to be a fully integrated business unit that can take advantage of Tower's 5,000 people. It's 30 years old, israel-centric, and we know very well that there is good Israeli discipline in our team.

Another thing I've said is, "Hey, I also want to make a Mobileye-like shift to our foundry business at some point." "I'm going to keep the structure, rather than integrating as many structures as possible, and I'm going to make it more independent to achieve this, which means I'm going to leverage more towers and the expertise they've built over time as part of that."

The comparison with GlobalFoundries is also interesting, I mean, I'm interested in GF. When we look at Tower, it's clear that it's more natural here than the first time we see it. One of them is, "Hey, that's going to cost me $30 billion, it's going to cost me $5.5 billion—"

Stratechery: You need money to build a fab.

PG: It's important.

But over time, I created a natural way out, into the mature node. It's not that I need GlobalFoundries to help create 16nm, I'm going to have a lot of the future and 10nm. So Global needs to move on, but they hit a wall at 10 nanometers because they can't cross an EUV, so naturally their business is compressed between customers who need to move on and hit a 10nm wall, and I tackle it easily. So in a way, they have more expensive depreciating assets. And the expertise will always be there, and will always be doing our RF technology and so on, and all the nodes there. Over time, they're actually more sustainable and sticky and can scale up, and I would say mature nodes have natural pressure.

Another thing that is happening in the market is that China is injecting extraordinary capital into its semiconductor business. They can't be below 10nm because they can't get EUV, and they have a hard time replicating professional nodes. Where did it go? It enters memory or into mature nodes. I see this business because we look at it more closely and you look at where GF's value proposition is now and it's like "Dude, this is, in a very good position in 22 and 23 years. But '24,' 25, '26, hmm. ”

So, if I can get dna from Tower and make sure I keep it alive and healthy and ready for me to have Intel and professional supplements, I never want to stay in memory, and you see I'm doing everything I can to pull out of our memory business in this area.

Stratechery: You don't want to undo Andy Grove's most famous decision, do you?

PG: Yes, that's right. As my frontier capabilities mature and depreciate over time, it naturally fills the mature node space over time. So I think I'm actually in a better place in the end thanks to the acquisition of Tower.

Stratechery: I'm curious about this mature node problem. Intel actually built it 14 or 16 nanometers after they started it, because they hit the wall with 10 nm, so you're going to have enough capacity there, but when it comes to 28 to 45 nanometers, I mean, you really didn't, because you pushed it all forward. Should Intel have made this shift before? Because these are nodes where a lot of activity occurs. Are you a little too late or just in time?

PG: That's a good question because I want to have some 28nm capacity to compete with it? Yes, I want to be more effective in the foundry business. But what happened, Ben, I think the Intel 16 nm performed well because why start a new design at the 28 when the customer can choose 16 nm?

Stratechery: You're going to have a lot of capacity, and you're going to have a lot of pricing power and stuff like that.

PG: Now, if I'm a TSMC customer today, that's a sweet spot node for TSMC, so 28 nm is really good. If you have something older than that, because of the overall semiconductor shortage, you're going to push those designs forward. I guess I'd say, "Hey, all the way. Move to 16nm or move to the last great FinFET technology 3nm. "Each transistor has a different price point as well as performance and density, etc., but if you're going to move your design, I think we actually have a good option. We will also do automatic grading at 3 nm and 16 nm. So I think if you push for design, I can compete very well. If you're on an existing node, what I really need to do is basically compatible with TSMC's 28nm process. So for that, I wish I could have it, but I'm not sure if it's worth $30 billion.

Stratechery: Taking a step back, a key factor that makes this strategy work is calculating the long-term stakes that will increase significantly. TSMC apparently made the same bet that their capital expenditures were stratosphere. Now we're seeing a shortage of this chip, very serious, but at the same time, IFS won't reach scale for years. Are you worried that we're going to have a situation where all of these TSMC's capacities are online, IFS is online, Samsung is also online — it's a classic in the semiconductor industry — and suddenly there's too much capacity? In that case, are you worried about an economic downturn?

PG: I'm not really, but let's separate it a little bit more, I'm sitting here. The first thing I have to ask you, because the semiconductor industry is cyclical, when was the last time we had a logic surplus instead of a memory glut?

The last time there was a memory glut was about three and a half years ago. The last logical surplus was more than a decade ago. So, as I asserted at the investor campaign, the idea is an insatiable need for computing and high performance.

Stratechery: Even though you've had smartphones for the last decade; going forward, everything is high-performance machine learning, and that's where you see all your needs coming from.

PG: Yeah, I just see that I want my phone to be more powerful at lower power. I want my cloud to be more powerful at lower power, my car – we've talked about the automotive industry going from 4% to 20% of BOM by 2030. Where is the bill of materials for semi-finished automotive products? High-performance connectivity, the characteristics of autonomous vehicles, which were the highest points of hundreds of performance requirements, advanced infotainment systems, and EVs, i.e., the electrification of cars, were primarily professional nodes at the time. None of them go to mature nodes, and all of them go into advanced computing. When we parted it, we weren't so worried.

Now, let's look at capital expenditures. Only three companies are less than 10 in size. Samsung, TSMC and Intel. Obviously, Samsung's capital budget is clearly divided between memory and logic, which accounts for the majority. My budget is not divided between memory and logic, but rather logic. TSMC's capacity is divided between maturity — they now have to go to the mature node where they can reinvest in maturity — and the leading node, so I think in this picture, as we can see, we're not bad, and we have ace, a Western foundry. People will become less and less accustomed to South Korea and Taiwan. Where are you going to put your second source and your second ability? We will also soon announce our Plans for European Expansion, with biased Western foundry capacity. I think in this, we look pretty good.

Obviously, we have a lot of work to do and these things take time to establish, but when the pressure comes, I think I'm ready.

Another point I'm making here is let's imagine I have an extra fab sitting right here, filled with EUV equipment, ready to make wafers in 2026. I can use one of three ways. One is I'm going to win back more shares from AMD. Hey, maybe I'll do this at a lower profit point, but I can accept it. Second, I go and win more foundry business at a lower profit point, but to win more foundry, or third, I pull chips back from an external foundry back to my own fab. Regardless of any of these three strategies, they have a great cash-added effect on the company. So, I aspire to have a backup fab that day because I think it means an increase in market share and company profit margins.

Stratechery: Is x86 still a trump card, or is it in decline?

PG: Hey, I have a 486 on my wall. I'm not ashamed of emotional bias here, but at the same time, architecture franchises aren't what they used to be because there are RISC-V, ARM, x86. There are more and more families of accelerators that can run more meaningful workloads. You can't simply say it's not good if it's not x86, which is why we support RISC-V, ARM, and x86.

At the same time, the long tail of the software ecosystem is still a very strong long tail. Every day I sell another x86 socket, which is the most profitable and strategic thing Intel can do. So, in that regard, I'm going to be less inclined to support other architectures, GPUs, etc., and bundle all of that together using oneAPI, but the x86 franchise is still there and it's very good. In terms of compute workloads, if you look at the overall situation, it's as fast as Nvidia is adding GPU workloads, and the x86 workload has a much larger cardinality, and the x86 workload is all that time.

★ Click [Read the original] at the end of the article to view the link to the original article!

*Disclaimer: This article is original by the author. The content of the article is the author's personal opinion, semiconductor industry observation reprint is only to convey a different point of view, does not mean that semiconductor industry observation endorses or supports the view, if there is any objection, welcome to contact semiconductor industry observation.

Today is the 2962nd content shared by Semiconductor Industry Watch for you, welcome to follow.

Wafer | integrated circuit | devices | automotive chips | storage | TSMC | AI | packages

Link to the original article!