Abstract: The market's biggest fear has happened: digital advertising giant Meta warned that by high inflation and supply chain bottlenecks on advertiser budgets, at a time when the meta-universe has not yet been built, the monetization ability of users' preferred short video products is weak, falling 23% after hours, the market value erased $165 billion, dragging the NASDAQ 100 ETF QQQ down more than 1.8%.

On Wednesday, February 2, after the U.S. stock market, facebook and digital advertising giant Facebook, whichse strategic focus shifted to "meta-universe first", announced its fourth-quarter fiscal 2021 financial report, which is also the first quarterly financial report since it renamed its parent company Meta Platforms last October, giving investors a window to observe the financial impact of Facebook's transition to meta-universe.

Meta Platforms revenue rose 20% year-on-year in the fourth quarter of last year, slightly exceeding expectations, and the year-on-year decline in earnings per share doubled from market expectations, the first net profit decline since the second quarter of 2019. Core app Facebook's user metrics were weaker than expected, and it was not good for revenue guidance in the first quarter of this year.

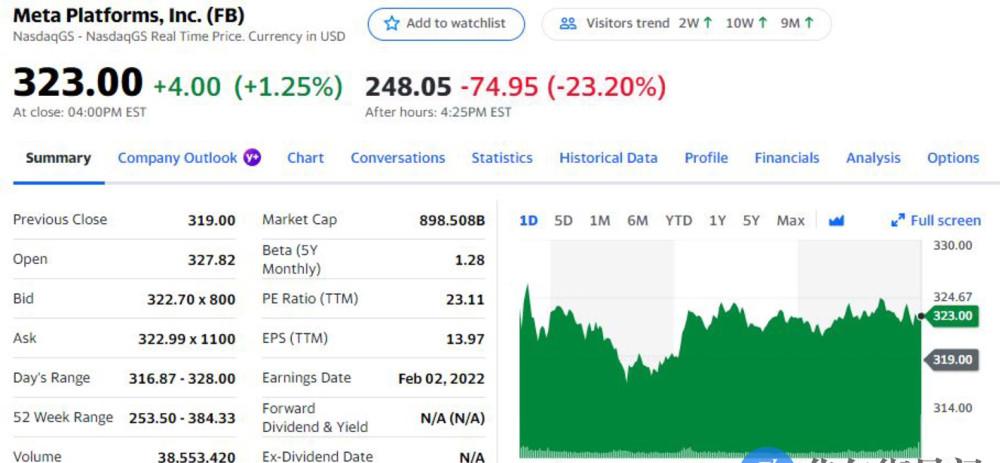

The company warned that due to the negative impact of high inflation and supply chain bottlenecks on advertisers' budgets, users preferred short video products with weak monetization capabilities compared to other mature features, plunging 23% after hours, falling $75 to a one-year low, dragging nasdaq 100 ETF QQQ down more than 1.8%, becoming the second tech giant to plummet after Netflix's earnings report.

According to financial blogger Zerohedge, a 23 percent drop that occurred during the day trading session would create the largest one-day drop in the company's history, equivalent to erasing $165 billion in market capitalization, or half of the market value of the second-largest digital currency, Ethereum.

Facebook's parent company, Meta, rose more than 1 percent on Wednesday, up five days in a row, recovering most of the losses it had fallen since Jan. 14, down 4 percent so far this year, down 16 percent from a record high of September 7 last year and up 3.5 percent since October 27 last year, the day before it was renamed Meta. 41 of the 53 analysts counted by FactSet rated "buy," with an average price target of nearly $398 with a 23 percent upside.

The stock is currently the cheapest valued of FAAMNG's large technology stocks, at a 20% discount from the NASDAQ 100 and a price-to-earnings ratio of 21 times its earnings forecast for next year, while the NASDAQ's 100 P/E ratio is nearly 26 times. Matt Peron, head of research at asset manager Janus Henderson, said the relatively cheap valuations of companies with strong fundamentals were one of the reasons he liked Meta shares.

Q4 revenue growth rate slowed significantly compared with the first three quarters of last year, the first net profit in two and a half years declined, and the key user indicators were not good

According to the financial report, Meta's revenue in the fourth quarter of last year was $33.67 billion, slightly higher than analysts' expectations of $33.4 billion, an increase of 20% year-on-year. However, revenue growth slowed significantly from the first three quarters of last year, after 47.6%, 55.6% and more than 35%, respectively, and the revenue growth rate in the second quarter of last year was the fastest since the third quarter of fiscal 2016.

Quarter-adjusted EPS was $3.67, weaker than market expectations of $3.84, down 5 percent year-over-year and significantly double the 2 percent decline expected. Net profit was less than $10.3 billion, significantly weaker than expected at $10.9 billion, down 8 percent year-over-year and the first net profit decline since the second quarter of 2019.

Poor key user metrics. Facebook's daily active users in the fourth quarter were 1.93 billion, unchanged from the previous quarter, up 5% year-on-year and weaker than the market expectation of 1.95 billion. The monthly active users who were more concerned were 2.91 billion, also flat in the third quarter, up 4% year-on-year, and expected to be 2.95 billion.

But another core measure of the ability to monetize the user base: average revenue per user (ARPU) of $11.57, up 14 percent year-over-year and slightly higher than expected at $11.38.

The daily active users of all-app families, including Facebook, Messenger, Instagram and WhatsApp, were 2.82 billion, up 85% year-on-year, up slightly from 2.81 billion in the previous quarter; monthly active users were 3.59 billion, up 9% year-on-year and slightly up from 3.58 billion in the previous quarter.

In addition, the company's operating margin was 37% in the fourth quarter, slightly higher than the 36% in the third quarter, but significantly weaker than the 46% in the same period last year. Capital expenditures for the quarter and full year, including principal payments for financial leases, were $5.54 billion and $19.24 billion, respectively.

Repurchased $19.18 billion and $44.81 billion of Class A common stock in the fourth quarter and full year of last year, respectively, with $38.79 billion of authorized lines remaining to be used. Cash and equivalents at the end of last year fell to $48 billion from $58.08 billion at the end of the third quarter, and the number of employees further increased from more than 68,000 to nearly 72,000, a 23% year-on-year increase.

In terms of full-year revenue, Meta's total revenue in 2021 exceeded $117.9 billion, up 37% from $85.97 billion in 2020 and 20% more than the market originally expected.

Weak Q1 guidance, inflation and supply bottlenecks disrupt advertiser budgets, and the first half deal code was changed to META

It is worth noting that Meta's guidance for the first quarter of this year is weaker than expected, and revenue is expected to be in the range of $27 billion to $29 billion, which is equivalent to a year-on-year increase of 3% to 11%, while the market generally expects to exceed $30.1 billion.

The earnings statement said that the year-on-year increase in revenue in the first quarter of this year was mainly dragged down by the number of ad impressions (that is, the number of times the ads were seen by users in social content distribution) and pricing growth.

In addition to the increased competition for user time, the newly launched Reels short video feature is more popular, but the monetization ability is lower than that of more mature core products such as Feed and Stories. At the same time, its advertising pricing power continues to be negatively impacted by Apple's privacy changes, macroeconomic challenges such as high inflation and supply chain bottlenecks are affecting advertisers' budgets, and foreign currency exchange rates will also become a resistance to year-on-year revenue growth.

The company expects total spending of $90 billion to $95 billion in 2022, compared with previous forecasts of $91 billion to $97 billion, and spending growth will be driven by investments in technology, products, talent and infrastructure. thereinto. Capital expenditures are expected to be $29 billion to $34 billion this year, unchanged from previous estimates, largely from investments in data centers, servers, network infrastructure and office facilities.

The earnings report said the company's investment in artificial intelligence and machine learning has "increased significantly," but the main focus of capital spending this year does not include "metacosms": "While Reality Labs products and services may require more infrastructure capacity in the future, they don't need a lot of capacity now and are therefore not a significant driver of capital spending in 2022." ”

Company executives said on an earnings call:

Artificial intelligence will play a major role in the process of creating a "metacosm".

Given TikTok's popularity with consumers, the company will focus on Instgram's Reels short video brand in the future.

The company is also preparing to change the stock trading code to "META" in the first half of this year, replacing the code "FB" since the 2012 US stock IPO, and the exact time details are to be announced in the future.

Meta disclosed for the first time the results of the division that included the meta-universe strategy, and the revenue doubled throughout the year, but last year's net loss exceeded $10 billion, and the loss widened year by year

Meta's new earnings structure consists of two parts, one is the "app family" that includes Facebook, Instagram, Messenger, WhatsApp and other services, and the second is FRL (Reality Labs), which includes hardware, software and content related to AR (augmented reality) and VR (virtual reality).

This is the first time Meta has disclosed financial data for the FRL division, which includes the Metacostem Strategy, and the company expects the investment in Metacosm to reduce operating profit by about $10 billion in 2021, and FRL will not be profitable in the short term. In CEO Zuckerberg's vision of the metacosmology last July, he hoped to turn Facebook into a metacosmite company in about five years, and billions of dollars of multi-year investment would eat into profits.

According to the financial report, FRL's revenue in the fourth quarter of last year was $877 million, up 57% sequentially and 22% year-on-year. The segment generated revenue of $2.274 billion for the full year 2021, double its 2020 revenue of $1.139 billion and $500 million in 2019.

At the same time, the segment's operating loss in the fourth quarter of last year was $3.3 billion, and the net loss for each quarter of the year gradually widened, with a net loss of $10.19 billion for the full year of 2021, a net loss of $6.62 billion in 2020, and a net loss of $4.5 billion in 2019.

In contrast, the app family's fourth-quarter revenue was nearly $32.8 billion, up 15% sequentially and nearly 20% year-over-year. Revenue exceeded $115.6 billion for the full year 2021, more than $84.8 billion in 2020 and nearly $70.2 billion in 2019, with no operating loss recorded during the period.

In addition, advertising revenue was $32.639 billion in the fourth quarter, in line with market expectations, up 15.4% sequentially and 20% year-on-year, accounting for nearly 97% of revenue. Other non-advertising revenue was $155 million in the quarter, down 12% sequentially and nearly 8% year-over-year.

The company warned in the third quarter of the financial report that non-advertising revenue is expected to decline year-on-year in the fourth quarter, because the all-in-one VR headset sales launched at the end of 2020 are too strong, making it difficult to surpass the same comparison at the end of 2021.

Meta has never disclosed sales figures for the Oculus Quest 2 headset, and last July's notice of recall of facial foam paddings involved about 4 million devices in the United States. The Oculus app, which became the number one app for the Apple App Store in the U.S. on Christmas day last year, could also be seen as the latest sign of strong sales of the device, a topic of focus on Wall Street.

Wall Street remains focused on the core of social media advertising, and a clear path to the initial monetization of the metacosmity is key

The analysis generally pointed out that although Meta said it would invest billions of dollars to build a meta-universe virtual world, for now, its Facebook and Instagram apps and core advertising revenue, which accounts for the absolute majority of revenue, are still the focus of investors' attention.

Meta has the second largest digital advertising platform in the world after Google. Last year's third quarter, the company warned that it faced a continuous crackdown on Apple's operating system privacy changes, the macro economy and the epidemic in the fourth quarter, and "major uncertainties."

Daniel Newman, principal analyst at Digital Technology-focused Futurum Research, points out that it is important to pay attention to how sensitive the advertising business is to price increases, and how robust is Facebook in a high inflation environment? If the economic slowdown can continue to raise prices, Evercore ISI analyst Mark Mahaney also believes that Apple's privacy change obviously had a negative impact on Facebook in the third quarter, and the key question is whether the latter can further reduce this risk, or whether the negative impact has expanded.

Judging from today's Meta assessment of "high inflation and supply chain bottlenecks reduce advertiser budgets", it can be said that the most feared phenomenon in the market is happening.

Investors also want to see indicators of profitability in the FRL sector. Bank of America analyst Justin Post said last week that Wall Street wondered "how much profit loss will be caused to Meta in the coming years" by investing in metacosm. Brad Erickson, an analyst at RBC Capital Markets, said a key question investors want to see resolved is whether there is a clear path to the initial monetization of the metacosmity.

Since Meta released the Metacosmum Manifesto, there have been 224 earnings calls from U.S. companies in 2021 that mention "metacosmity" once, compared to just seven in 2020, showing the popularity of metaversity as the next mainstream concept after the mobile Internet. But Kim Forrest, chief investment officer at Bokeh Capital, warned that Meta is expected to invest heavily in the meta-universe and that the first movers cannot guarantee success.

Global X research analyst Pedro Palandrani also called the metacosmity a "long-term story," with investors paying more attention in the short term to how Meta navigates Apple's privacy changes, e-commerce business breakthroughs, and ways to monetize Messenger or the short video Reels feature.