In the previous article, we discussed Bitcoin's "natural consensus" origins and the same test of "secular consensus" choices. In order to further clarify and understand the nature of Bitcoin, it is necessary to first focus on the value law of Bitcoin, which is the core content of the analysis of the Bitcoin Economic Model.

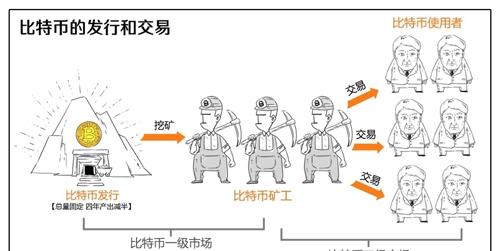

First of all, the issuance and trading of bitcoin has formed a primary and secondary market (the issuance of bitcoin, which started from the beginning of 2009, according to the rule of about four-year halving, a total of 33 times, after a cycle of more than 100 years, can not reach 1 satoshi, that is, one hundred millionth of a bitcoin, and terminate the issuance by the time of the halving around 2140. It should be noted that the role of miners, in the primary and secondary markets, the role has been reversed: in the primary market, because the rules determine the number and rhythm of issuance, the supply of bitcoin (in the cycle stage of every four years) is constant, and at this time the miner is the entire demand side, the more miners (hash power) to mine, the stronger the demand for the demand side, directly pushing up the cost of mining, that is, increasing the cost of obtaining a first-hand bitcoin; and in the secondary market, because miners only hold a first-hand bitcoin Therefore, miners have become the most important suppliers, and users who speculate and use Bitcoin have become the demand side of the secondary market, while the other type of supplier is the holder of second-hand bitcoin.

Bitcoin's self-mining and output mechanism forms a self-price increase. Assuming that in a longer period (more than four years), even if the overall hash power cost input of Bitcoin remains unchanged, since the output mechanism of Bitcoin is less and less output per unit of time (halving on average every four years), the output and acquisition costs per unit of Bitcoin will double in the same cycle. Assuming that even if only a few miners have maintained the overall hashrate cost input of Bitcoin (not declining), in the entire 100-year issuance cycle of Bitcoin, a total of 33 issuance halving (the last one was reduced to 0, so it is not included in the calculation) led to an increase in the cost of output hashrate is 2 to the 32nd power = 4,294,967,296, that is, nearly 4.3 billion times the hashing cost increase. This reminds us of the interesting story of the ancient Indian king and the chess king, on the 64-grid chessboard, the king starts with 1 grain of wheat, rewards the chess king with twice as much wheat every day, begins with an unknown king, and finally becomes a tragedy that does not understand mathematics (the story content is not repeated, please find it yourself). Similarly, the initial investment of Bitcoin miners can be equivalent to the 4.3 billion investment in the final period, which is a clever logic to be small and broad. Here, we refer to the increase in output costs every four years due to issuance rules only when the cost of hash power remains unchanged, which is called "the cost increase of the middle cost".

The above discussion is based on the "cost of hashing power" in order to simplify the calculation. Because if the computing power is used as the base, it is necessary to convert the hashing power into the current cost, and over time, the conversion rate between the future hashing power and the cost will change, which involves complex rules such as Moore's Law and Locke's Law, and whether these laws are accurate. Therefore, starting with the "input cost of computing power" and then discussing its "output cost" simplifies the calculation and simply and directly sees the essence of Bitcoin's issuance rules. At the same time, transaction fees will also be converted from initial insignificance to a larger and larger proportion of miners' income as Bitcoin is issued. As for the calculation relationship between the transaction fee level and the miner's hash rate, it is another set of calculation mechanisms that are completely independent of the above calculations. On the whole, the existence of transaction fees can have a certain effect of calming the "rising cost of the middle cost", because the transaction fee mechanism can be equivalent to the recovery and reissue of Bitcoin from a certain perspective. The curve of this fee cost model will have an intersection with the curve of "cost increase in the middle of the cost", so as to gradually transform from the issuance stage of the "cost increase of the middle cost" as the main cause in the early and medium term to the issuance stage of the middle and late stages with the fee cost model as the main cause. However, due to the soaring fees caused by the extremely low efficiency of Bitcoin, which has brought a lot of criticism, the rules of the fees have also been revised during the iteration of the version of Bitcoin, making the fee rules quite uncertain, so the calculation of this aspect is not introduced here.

In practice, in a short period, more new hash power may be added to the market, and it may also lead to a phased or temporary large-scale withdrawal of hash rate due to any accidental factor, resulting in irregular fluctuations (up and down) of hash rate. However, under the "long cycle", the overall upward trend of the output cost of this daily output that can be maintained by relying only on a small number of computing power input costs (such as the beginning of the birth of Bitcoin) has created the basic trend of the eternal rise of the primary market price of Bitcoin. During its development and rise, for example, with the spread of the concept of Bitcoin, the overall hashing power investment of Bitcoin will also increase significantly, and it will be superimposed on the basis of "cost increase in the middle of the cost", resulting in a steeper price increase curve of Bitcoin. We define the increase in output costs due to the increase (or decrease) of the overall hashing power cost as "the increase (or decrease) of the cost of the computing source".

At present, the Bitcoin output halving cycle has only entered the third phase, and there have been two halvings, which is equivalent to the third chess grid when the Indian king rewards the king of chess with wheat, and the effect of this design rule is still not obvious enough, just as the indian king only needs to pay 4 grains of wheat on the third day, and cannot feel the effect of the "index" in the later stage.

Now let's take a closer look at the law of supply and demand value of Bitcoin in a short period (months to four years) when the cyclical output is constant.

Let's start with the primary market, the mining and output markets. An important feature of Bitcoin is that its output rate is fixed, and it does not expand because of the expansion of production scale, and the shrinking scale of production shrinks, which is precisely an important manifestation of Bitcoin's non-commodity. The market law of ordinary commodities is that because the production of a commodity is profitable and attracts more production, thereby expanding the supply, resulting in the oversupply of the commodity, the decline in market prices, and then the reduction or disappearance of profits, so that some producers withdraw from the market, and finally achieve a dynamic balance of supply and demand, which is the automatic adjustment mechanism of commodity prices in the market economic environment. The law that expanding production increases supply is even applicable to assets such as gold and oil and commodities. On the other hand, bitcoin, when the value of bitcoin is in an upward channel, will stimulate more production capacity into operation, but it can not increase the supply at all, but increase the demand. In the Bitcoin economy, more capacity is put into operation, but it directly pushes up the primary market price of Bitcoin, which in turn attracts more production capacity investment, guides the primary market price to rise even more, and forms a positive feedback that is repeatedly amplified until an accidental factor interrupts the process. When the value of Bitcoin is in a downward channel, it is a reverse process. This is the most important first important reason why the price of the Bitcoin market fluctuates extremely sharply in a short period of time.

Look at the secondary market, the ordinary buyer's and seller's market for Bitcoin, the market served by cryptocurrency "exchanges." The secondary market price of Bitcoin is the price formed between the instantaneous demand formed by the purchase of Bitcoin in the market and the instantaneous supply formed by the sale of stock + the sale of new output.

The buyer's demand in the secondary market is first derived from the demand for holding Bitcoin, such as speculation, investment, collection, etc., and the second is from the demand for use and circulation of Bitcoin. In the early history of Bitcoin's development, bitcoin's buyer demand first came from the demand for holding, and out of the demand for use and circulation, it was very scarce in the early days (such as using bitcoin to buy a pizza, or the flow of black gold and gray gold). The ico that appeared in 2013 began to appear for the first time, creating a new demand for the use of coins, which led to the first surge of bitcoin in 2014, and then due to the poor development of most ico projects, the price of bitcoin fell sharply. But in the first wave of ICOs, incubating and bring a rare success case - Ethereum. Ethereum proposed and implemented a smart contract mechanism, driving the blockchain into the era of "smart contracts", making token issuance extremely simple, which greatly reduced the threshold of icing, leading to the outbreak of icicos in mid-2017, and the financing behavior became a large-scale financing behavior, which led to a sudden surge in demand for the circulation and use of coins, which is the real reason why the recent bitcoin price has soared again and created a new high. With the inhibition of ICO behavior, the current price of Bitcoin has fallen to a certain extent, which is also a reflection of this market situation. The overall operation law of the secondary market conforms to the law of supply and demand in the general market, that is, the balance between supply and demand.

"Output value" (primary market) and "market value" (secondary market) do not coincide at all times. When the output value is higher than the market value, the mined coins cannot be sold or lost, some mining pools are stopped due to insufficient income, the production of coins is suppressed, and the primary market price is reduced. When the output value is lower than the market value, the mined coins must be profitable in principle, on the one hand, it will attract more mining pools to operate, resulting in an increase in the price of the primary market, under simple logic, in most cases, it will lead to an increase in the price of the secondary market; on the other hand, the holders of the chinese currency in the secondary market will be reluctant to sell, because the expected value of the currency will continue to rise, resulting in a reduction in the supply of coins in the market, which will further push up the secondary market value. This is the second important reason why the Bitcoin market is extremely volatile. When the market is in equilibrium, the cost of mining, just offsets the income from the sale of coins, which is equivalent to converting computing power + electricity into some kind of value that can be globally circulated. In actual observation, the market value of Bitcoin is higher than the output value and there is a price difference, and there has also been a stage of decline in overall computing power, and the specific reasons need to be seen in detail.

Bitcoin will still have one day to be mined, when the value of Bitcoin will lose a so-called output cost support, leaving only a "historical output cost" support. Of course, miners will still receive transaction fees, and, according to calculations, long before Bitcoin is fully mined, the transaction fee income of miners will exceed the bitcoin income rewarded by the system at some point, so that miners can receive continuous incentives and continue to serve as the cornerstone of the Bitcoin ecosystem. Of course, I don't know how future humans (calculated to be 2140) will view the "historical cost of output." For example, it is said that when the refrigerator was first invented, you could change a car, but if you saved an old refrigerator at that time, it may be worthless now, but if the car becomes a classic car, it is still worth a lot. At the same time, when the bitcoin issuance ends, the incentive and motivation to maintain the overall computing power (mining machine) of the entire Bitcoin system to continue to operate has become the transaction fee of the Bitcoin system, at this time, if the total computing power is still very high, it means that the operating cost of the entire Bitcoin system is very large, and the total transaction fee is still very high, which is a negative element for a trading system, and its competitiveness will be greatly challenged, because the Bitcoin system at this time, There is no difference from a system that distributes all the coins at the beginning. If this problem is not solved, the value trading system may be eliminated by competition from other cryptocurrency systems with lower operating costs. Of course, perhaps Bitcoin has experienced a sharp decline in overall computing power long before it is mined, and when the final coin issuance is completed, the overall operating costs are already relatively low, but this also means that the system has become unpopular.

Of course, the so-called mining work, a situation worth mentioning, in the early days, of course, has always existed, by some online machine vacancy time hashing power to complete, and even, there are many "private work" behavior. Sometimes the owner of the miner is the technical manager of some computer room, and they use the idle machine and network resources of the machine room for mining behavior. They have no corresponding output cost at all, because this kind of "private work" is often carried out privately behind the back of the owner of the computer room. From this point of view, in fact, the input cost of some bitcoin output hashrate is equivalent to zero. In the later period, mining machines and mining pools specifically for mining appeared.

As a second summary, bitcoin founders defined the "cost of output" that rises eternally under the "long cycle." What we have repeatedly emphasized is that only the "cost of output" is mentioned here, and the "value" will be further discussed later. An initial hash rate investment is equivalent to the 4.3 billion hash rate investment at the end of the period. In the "short cycle" of the Bitcoin economy, because the output rate is fixed, more production capacity inputs, but push up the primary market price of Bitcoin, thereby attracting more production capacity input, guiding the primary market price to rise more sharply, forming a positive feedback effect. The source of buyer demand in the secondary market is first from the demand for holding Bitcoin, and the second is from the demand for circulation using Bitcoin. The emergence and outbreak of ICOs led to a sudden and sharp surge in demand for the circulation and use of the coin, causing two spikes in the price in Bitcoin's history.

Writing this, you may want to ask whether there should be a positive or negative view of Bitcoin and other cryptocurrencies. Looking back at the development of the Internet and the mobile Internet, how similar the process is, there is no simple white and black, nor can it be summarized by the simple word scam. In the current market, there is no shortage of people who are mysterious and exaggerated, and there are also a large number of cases of using the lack of rules of ico and fishing in muddy waters, and more melon-eating masses are in the clouds and blindly following the trend, but under the muddy waters, there is an unexplored future. Next articleWe will do some slightly subjective analysis of Bitcoin's properties in order to provide some predictable predictions for the future of cryptocurrencies.

About the Author

Zhang Xiangning, China's first generation of Internet entrepreneurs, founded www.net.cn in 1995 and was acquired by the then Hong Kong-listed Alibaba Group in 2009, becoming the predecessor of Alibaba Cloud. He is currently the founding partner of Qingyi Investment, a member of the 10th and 11th All-China Youth Federation, a director of the Internet Society of China, the vice president of the Alumni Entrepreneur Association of Beijing Normal University, and the vice president of the Beijing Alumni Association of Huazhong University of Science and Technology (formerly Huazhong University of Technology).

【Related Articles】