Written by | Xu Weijia

On September 17, 2021, the results of the review meeting of the Listing Committee of the Science and Technology Innovation Board showed that the initial offering of Shanghai Haihe Pharmaceutical Research and Development Co., Ltd. (hereinafter referred to as "Haihe Pharmaceutical") did not meet the issuance conditions, listing conditions and information disclosure requirements. Haihe Pharmaceutical's suspension of the sci-tech board seems to imply that the capital market is no longer easy to pay for the authorized introduction model of China biotech companies.

Soon, the secondary market had a ripple effect on this regulatory-oriented audit result. R&D customers observed that affected by the news, from September 10 to September 30, a number of Biotech companies listed in Hong Kong, including WuXi Juno, Zai Ding Pharmaceutical, Fuhong Henlin and CStone Pharmaceutical, suffered a heavy share price. Among them, WuXi Junuo fell by 36%, the market value evaporated by 3.42 billion Hong Kong dollars, and The decline of Deqi Pharmaceutical was nearly 25%, and the market value shrank by 2.3 billion Hong Kong dollars.

Be wary of the liensing-in of capital bundles

It is generally believed that the rejection of the listing of Haihe Drugs stems from the fact that most of the company's research projects are from cooperative research and development or licensing-in, and the Listing Committee of the Science and Technology Innovation Board has questioned its independent innovation ability.

But this is probably not a phenomenon unique to sea and medicine. It's no exaggeration to say that without license-in, China probably wouldn't have spawned a large number of innovative drug companies in just a few years. After the establishment of the 18A new rules of the Hong Kong Stock Exchange and the establishment of the A-share science and technology innovation board, this model has become the path dependence of many companies.

In this process, capital has undoubtedly played a role in fueling the waves. So, the sharp decline in the stock prices of many biomedical companies caused by the rejection of the Haihe Pharmaceutical Science and Technology Innovation Board is an overreaction of the capital market or a rational return to value?

In this regard, there are two very different voices in the capital circle. One voice thinks investors voting with their feet are panicking too much. "We believe that compared with the longer and more uncertain early development of new drugs, the adoption of the license-in model can make the valuation of unprofitable companies more certain."

However, fund managers of pharmaceutical thematic funds believe that the motivation of listed companies needs to be more vigilant than valuation certainty. "Many innovative drug research and development companies that are deeply bound by capital have adopted the license-in model to increase the listing weight in order to seek to cash out the early investment institutions as soon as possible, and achieve short-term rapid listing, while ignoring the long-term value."

In fact, because the chain of new drug research and development is too lengthy, it is difficult for a company to achieve full coverage. As Xu Ning, executive vice president of Zaiding Pharmaceutical, said in an earlier interview with R&D customers, two-thirds of the products of large foreign companies are obtained through open innovation, and only one-third or less comes out of the laboratory. In recent years, many multinational pharmaceutical companies have also "ridden the city" on the road of "buying, buying and buying", and in this way, they have put more emphasis into the clinical transformation part they are good at.

On the contrary, for Chinese biotech companies that have grown up through "buying, buying and buying", the vision of choosing differentiated products, clinical research design, etc. are all tests of the overall level of the team. What needs to be avoided is not actually the license-in itself. What really needs vigilance is to blindly introduce products in order to accelerate the pace of listing under the coercion of capital, and even fall into the quagmire of homogeneous competition. As a result, in the future commercialization process, it is difficult to bring a good valuation to the enterprise.

Innovation is incremental

In fact, the industry has a long history of discussion about whether liensing-in is pseudo-innovative.

In this regard, a founder of a new drug research and development enterprise who did not want to be named told the developer that the current understanding of the Chinese people on the license-in has a misunderstanding, thinking that this is imitation, cooperative research and development has no independent research and development or just dependence on other people's technology, in fact, it is not. Licensing-in is not the original of Chinese biotechnology companies, but a very practical means and channel for complementary product pipelines, R&D technology concepts and sales network cooperation in the world. "China's independent innovation needs a process, just like from imitation to innovation, from licensing to source development, it is gradual."

At present, the leaders of local innovative drugs who are rapidly rising with the license-in model have also begun to pay more and more attention to open innovation, translational medicine and independent research and development.

Recently, Tektronix and LegoChem Biosciences entered into a collaborative development and licensing option agreement for novel antibody-conjugated drugs (ADCs). The two parties will jointly develop and evaluate new ADC drugs using D&Pharma's premium antibody assets and LBC's next-generation ADC technology platform. Teckey Pharma reserves the right to select the global development and commercialization interests of the ADC candidate drugs resulting from the introduction. When this option is exercised, LCB will receive a down payment and potential milestone payments, as well as tiered royalties. In addition, LCB will also be eligible for a certain percentage share of the income from the authorized transfer of Deqi Pharmaceutical. This transaction is different from the traditional authorization introduction, and can also strengthen the existing independent research and development and global drug clinical development experience of Deqi Pharmaceutical.

In addition, the innovative drug companies represented by Nuocheng Jianhua and led by scientific research institutions have more independent research and development capabilities, and may replace the license-in model in the future and open the era of China's new drug research and development 2.0.

Sci-Tech Board attaches importance to "hard technology"

Zhao Hongchun, senior manager of the Shanghai Stock Exchange Issuance and Listing Service Center, reminded some biotechnology companies with listing aspirations to pay attention to information disclosure at the recent Zhangjiang Biomedical Summit Forum. Although this is a flexible requirement, under this flexibility there are very large requirements for business executives and intermediaries. To translate the prophecy of the industry into a capital market, investors can understand and recognize the language.

The founder of the aforementioned innovative drug company also talked to the developers about the importance of information disclosure. He believes that the blocking of Haihe from the IPO also reminds the increasingly strict and rational capital supervision, and startups need to learn how to communicate with the capital regulatory authorities and explain their advantages and characteristics from a scientific level.

In addition, Zhao Hongchun stressed that the mission of the science and technology innovation board is to promote the formation of a virtuous circle between science and technology, industry and capital through this market-oriented sector, and to promote the overall scientific and technological strength of the country through capital and market forces. Just because some companies have not been successfully listed, it cannot be generalized that the science and technology innovation board does not support the entire industry in which the enterprise is located. The Science and Technology Innovation Board pays great attention to whether the key core technologies and scientific and technological innovation capabilities of enterprises are prominent, and whether they have a high degree of market recognition. This is the obvious difference between the Sci-Tech Board and other sectors.

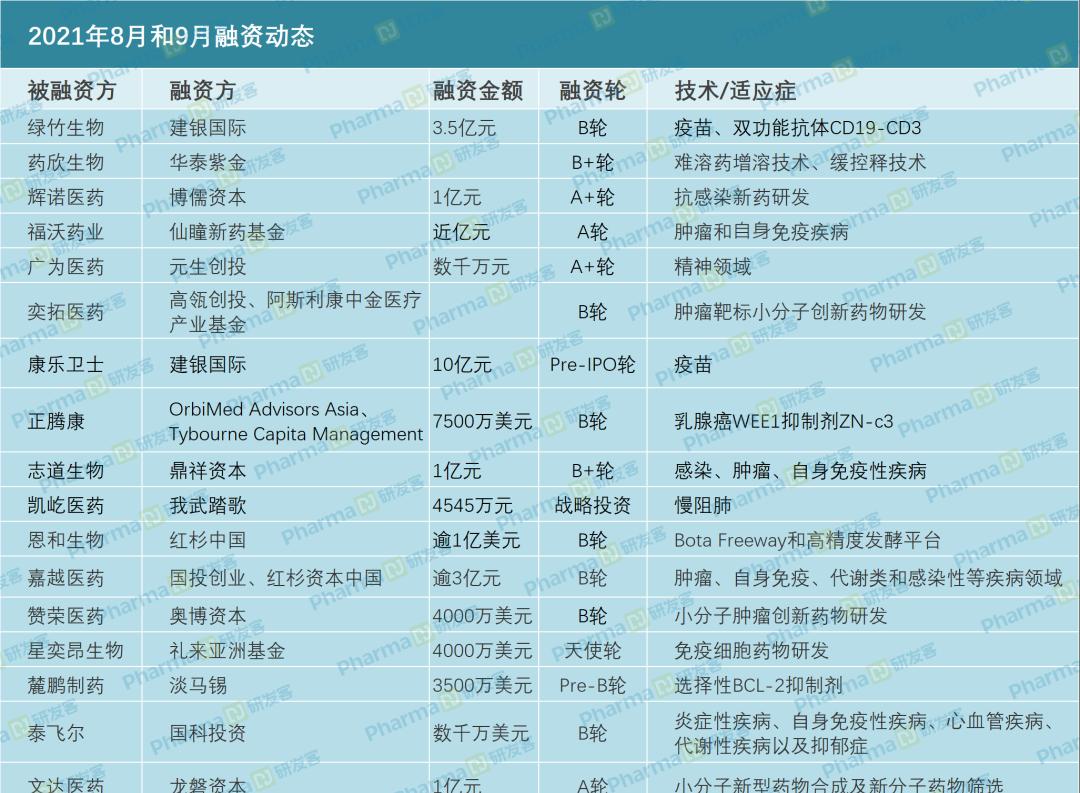

Financing dynamics in August and September

The market capitalization of A-share pharmaceutical listed companies is ranked

Editor| Yao Jia layout | Zhang Yue

Issue 1441