supply:

In the first half of October, sugar production in south-central Brazil reached 1.146 million tons, compared with 2.621 million tons in the same period last year, a 56% year-on-year decrease. The cut exceeded market expectations, and Brazil's local crushing season will be harvested early. Brazil's current crushing season due to drought and frost to determine the reduction in production, the most direct embodiment of which is the sugarcane yield fell by about 14%, although the crushing speed before the mid-season is faster, the cumulative sugar production of the biweekly data is only 5-7% behind, but also gives investors certain doubts about whether the speculation of the reduction in production can be realized. Recently, near the end of the crushing season, Brazil's production cuts have begun to appear, because at the end of the crushing season, Brazil is facing a situation of no cane to squeeze, and sugarcane is really not enough.

demand:

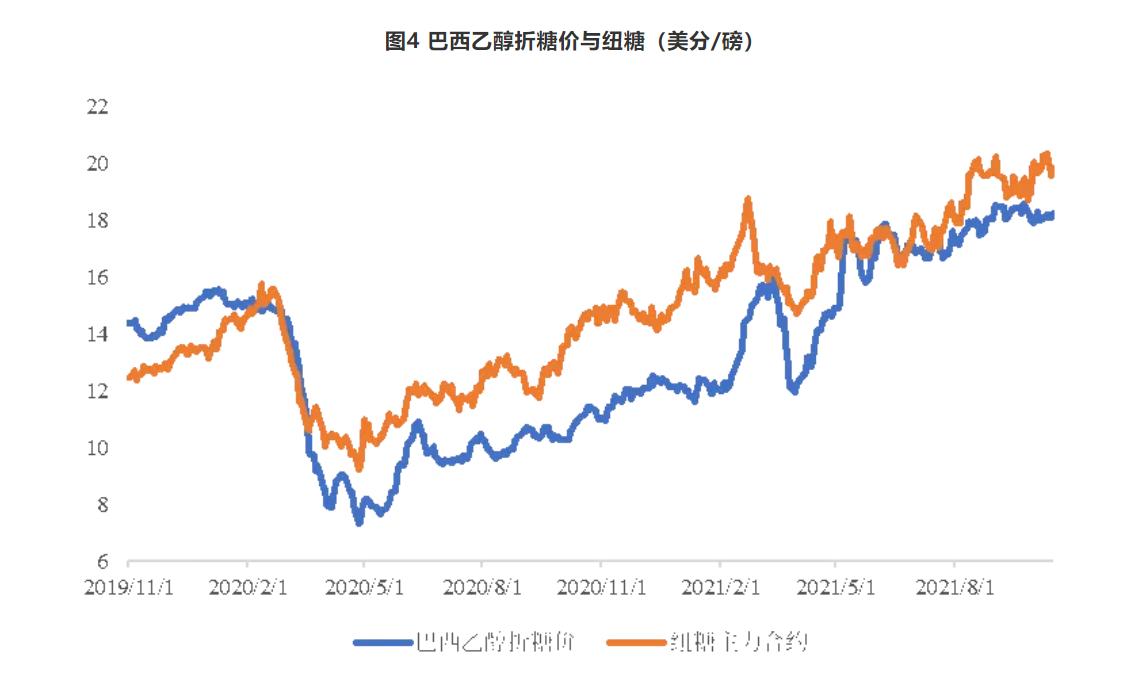

Brazilian ethanol has risen all the way and hit a local all-time high, and the current Brazilian ethanol discount sugar price has reached 19.86 cents/lb. Under the premise that crude oil continues to be bullish, ethanol may continue to climb higher, and Brazil is currently close to the end of the crushing season, and because sugarcane is not enough, it has to be harvested in advance, sugarcane is not enough, ethanol is not enough.

conclusion:

Then, in the next 4 months of empty window in South America, if the Asian market is affected by the La Niña climate and the supply supply cannot keep up, sugar prices will begin to accelerate.

!["People's Taste" Beitan cuisine is coming! White candy vs red candy, which one do you love?[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)