On the 21st, at the 2021 Financial Street Forum "Closed Door Seminar on China's REITs Market Construction from an International Perspective", Chen Qing, Managing Director of Singapore Exchange and Chairman of China, delivered a keynote speech. Chen Qing said that there is a lot of room for cooperation between China and Singapore's REITs market, which is mainly reflected in the following aspects:

First, in the successful REITs market, in addition to the qualifications of promoters, fund management capabilities are also important. In China, the general public fund serves as the main fund manager, while in the Singapore market, the subsidiaries of qualified promoters are also allowed to participate, cultivating many talents. Therefore, in terms of fund management capabilities, the two sides have a lot of room for reference and cooperation.

Second, exchange cooperation. Products are an important factor affecting liquidity and activity, and the co-construction of indexes between exchanges can be established through ETF interconnection to establish cross-border learning and cooperation, and the liquidity of REITs can be promoted through the construction of the product industry chain. Cooperation between exchanges, cooperation across markets is very important for REITs price discovery.

Third, professional teamwork. At present, investment banks, commercial banks and professional institutions have gradually begun to explore and develop in different markets. Some promoters will issue their REITs products in China and Singapore depending on their asset needs. It can be expected that there will be more and more cooperation among professional teams in the future.

The following is the full text of the speech:

Since the listing of the first REITs in Singapore 20 years ago, it has spanned several cycles, including the global financial crisis. The market activity of REITs in Singapore is very high, reflecting the recognition of the legal framework and maturity of the market by promoters and investors.

The first batch of Pilot Projects for Public ReiTs for Infrastructure in China were successfully listed, which injected great vitality into the international REITs market. Below I will delve into two aspects: first, the experience of the Singapore REITs market and the focus of international investors; second, the cooperation and competition between the Chinese market and the Singapore REITs market.

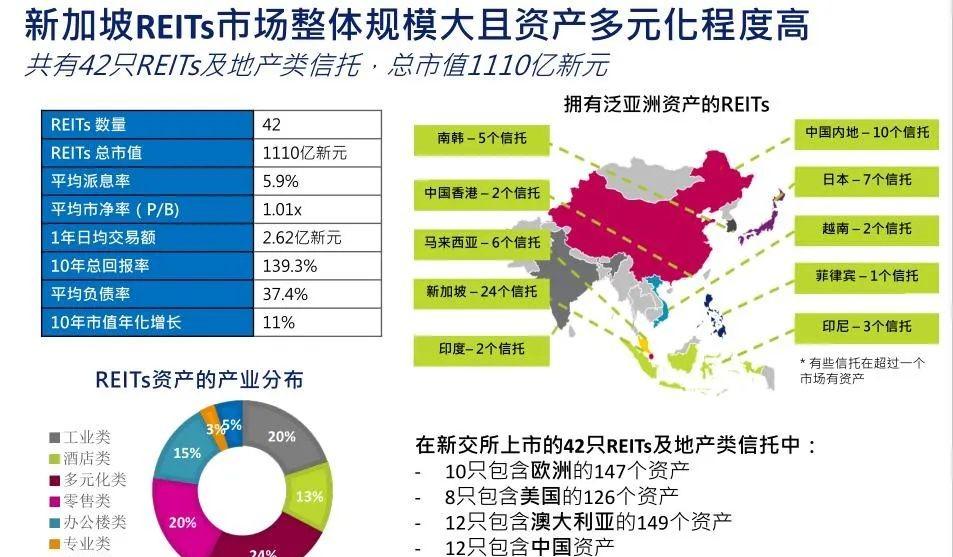

The first is the latest introduction to the ReiTs market in Singapore. In terms of scale, Singapore's REITs are second only to Japan in Asia, and the total market value of 42 REITs is currently more than 500 billion yuan, the market valuation is relatively reasonable, and the average price-to-book ratio is also within a reasonable range. In terms of geographical location, the international distribution of Singapore REITs is very high, and more than 80% of the underlying assets are distributed in the offshore market, including the United States, China, Europe, Southeast Asia and other places; there are 16 pure overseas asset package REITs and 12 REITs of Chinese assets.

Another feature of Singapore's REITs market is that the underlying assets are rich and evolving, including industrial, retail, infrastructure, etc., similar to mature markets. Singapore's REITs products can also be issued in 7 currencies according to the requirements of the issuer itself, the needs of investors and the characteristics of assets, including Singapore dollars, renminbi, dollars, euros, pounds sterling, etc.

The market recognizes Singapore REITs as having the following five characteristics:

Large number of investors and internationalization;

The regulatory framework is sound and mature and stable;

The tax system is relatively transparent and favourable;

Diversified assets, providing investors with rich investment opportunities;

High liquidity, active refinancing activities, and active asset acquisition transactions.

The REITs market is an important sector of Singapore's capital market, and has been pursuing depth and refinement for 20 years. The Singapore Exchange has also tried its best to continuously improve the entire ecosystem from the product side, and through 20 years of development, it has established a relatively complete industrial chain, including REITs with diversified assets as the underlying assets. REITs are actually a big concept, and different models such as business trusts, real estate investment trusts and joint stock trusts can be used to meet the different requirements for the listing of underlying assets. Because of the support of commercial trusts, the underlying assets can cover transportation infrastructure, environmental protection, telecommunications, ships, aircraft leasing, etc., as long as they can generate stable cash flow, they can meet the listing needs in different ways.

In terms of products, SGX-listed REITs are tracked by two funds, FTSE and iEdge, and a number of REITs stocks have been selected to be included in the Straits Times Index, an index of Singapore's main trading market, which has greatly increased the trading activity and attention of REITs.

In addition, ETFs with REITs as underlying assets have also set off a global pursuit boom. The three REITs listed on the SGX have stood firm during the pandemic, with total assets up 40% during the pandemic. Currently, the three ETFs have about $500 million in assets under management.

The Singapore Exchange is also a multi-asset platform. In August last year, SGX took the lead in launching Asia's first batch of REITs futures, tracking various REITs indexes listed in Singapore, Malaysia, Thailand and Hong Kong. This batch of futures contracts also provides a hedging tool for investors with risk management needs, so the industrial chain is relatively perfect, not only REITs stocks.

The Singapore REITs market has attracted internationally renowned investors and retail investors, and in recent years the following trends have emerged: high net worth individuals and family offices have begun to actively invest in singapore's REITs market. International investors recognize the market for the following main reasons:

First, the relevant policy framework is stable, and various government departments cooperate to formulate taxation and other supporting policies to improve the investment system;

Second, Singapore has brought together the world's high-profile and high-quality REITs promoters to ensure asset quality and asset management capabilities, such as China's Hualian and Sand Ship;

Third, under the cultivation of the ecological environment, the Singapore REITs market has accumulated a large number of experienced trust management talents and asset management talents;

Fourth, the geographical distribution of the underlying assets is internationalized, which is convenient for investors to find familiar geographical areas or assets of interest, enter the market through REITs, and diversify investment for asset allocation;

Fifth, the overall level of return is stable, with an average yield of about 6%. In the long run, there is a steady compound interest growth, with an average ten-year return of more than 130%.

During the pandemic, institutional investors had a net outflow of funds before July this year, while retail investors had a net inflow, because ultra-high-net-worth individuals focused on asset value and investment income rather than promoter size. In addition, individual investors believe that assets may be undervalued during the epidemic and thus get excess returns, so they are more willing to boldly enter the market at this point in time. Institutional investors pay attention to the size, scale and long-term stable income of the fund, such as insurance funds and pension funds, which focus on long-term stable income. But since July, both types of investors have seen net inflows of funds; since the beginning of the year, retail investors have seen net purchases of more than S$900 million.

In the first nine months of this year, SGX announced a number of REITs asset acquisition transactions with a consideration of more than S$9 billion, including data centers, logistics, student apartments, most of which took place outside singapore, further enhancing the internationalization of Singapore's REITs market.

Overall, the purpose of the ReiTs market development in Singapore is to improve its ability to withstand pressure and actively seek healthy new development opportunities. The asset operation reflects that the underlying assets, share prices and dividend payout ratios of REITs have gradually recovered. Listed REITs are also actively working together to strengthen their position and financing capabilities in the capital market.

In addition, ESG is highly sought after in the capital market. Just this week, Singapore Exchange and UOB Asset Management jointly launched the Green REITs Index, which covers 50 high-yield REITs that meet liquidity requirements and excel in real estate valuations. The quality index helps to form relevant ETF products in the future, and ESG is also reflected in the development of REITs products.

On the ground floor, the Singapore government and the Singapore Authority have proposed an extension of interest payments during the pandemic. In September, the government introduced policies on market activity, which included subsidies for government investment funds and issuers. The pandemic has not affected the development of REITs in Singapore, and some mature promoters have also taken full advantage of this opportunity to absorb and better recycle their assets.

The basic logic of equity investment is similar, but at this stage there are different concerns. For now, regulatory priorities are different. Because Singapore pays more attention to ecological construction because the market is mature, and the compliance of assets, the purity of ownership and the protection of investors' rights are still the core issues, Singapore has always maintained a rigorous and prudent attitude to achieve more stable development of the market, improve the ability to resist pressure and risk resistance.

The space for cooperation between Singapore and China is huge, mainly reflected in the following aspects:

First, in terms of successful REITs, both sponsor qualifications and fund management skills are important. At present, in China, public funds are the main fund managers. The Singapore market allows qualified sponsor subsidiaries to be managed and has cultivated a lot of talent. Therefore, in terms of fund management capabilities, the two countries have many references and cooperation.

Second, the cooperation of exchanges. Products are an important factor in promoting liquidity and activity. Index co-construction can be achieved between exchanges, and the market can establish cross-border learning and cooperation opportunities through ETF interconnection, and promote the liquidity of REITs through the construction of product industry chains. Product indices, ETFs and futures are important tools in the process of price discovery, so cross-market cooperation between exchanges is very important for the discovery of REITs prices.

Third, the cooperation of professional teams. Nowadays, investment banks, commercial banks, professional institutions, etc. are expanding in different markets. Many promoters issue REITs in China and Singapore according to different asset needs, and the professional team can expect to cooperate more and more actively.

All in all, the asset management industry is in a very important stage of development in the world, especially in China; and REITs, as a subdivision of asset management, can serve the real economy well and inject very important fresh blood into the asset management industry.