Recently rarely come up to write articles, mainly to meet some customers of different ages, I found that for 20-year-old white-collar workers, working overtime all day and no time to exercise this thing is really concerned, many people are very worried about the future in case they are not physically good one day, how to solve the loss of income, many second- and third-line white-collar workers who come to the big city to work hard, parents can not provide them with anything, and their current income is OK, so when they take advantage of their own physical practice, the first thing that comes to mind is their own health protection - health insurance.

But for white-collar workers around 40 years old, many are still because of the pressure of work, family factors, did not find a partner suitable for themselves, and at this age is basically in the high, low age, do not want to make it up, and passed the best age of childbearing, coupled with the private sector, pressure, the future uncontrollable factors are high, especially parents can not bring their own children of female friends, for childbearing will affect their own hard work for many years of career will still be grumpy, so they have been configured with health insurance many years ago, At the age of 40, in addition to health insurance, another level is to plan for their own pension.

This customer and I said that there are many colleagues who work part-time in various insurance companies in the company, and there are many proposals sent to her, but considering the part-time people, it is likely to be unstable, and they will leave in the future, they still want to find a full-time, professional person to help themselves plan, and their friends have read some of my articles, very much agree with my point of view, although her friends have only had a relationship with me, and they have a good impression of me, so they have this recommendation.

And this customer because of their future pension replacement rate will be relatively low, so will consider that after their retirement, each month can have 10,000 income, of course, she now also has other financial aspects and real estate investment, the future is old, if they do not have children, when they can go, they must want to go sightseeing, but they can not go one day, or hope to have a better place to have a high standard of medical care for their later life. So now I want to get involved in insurance for pension planning, but too many products, each family says that each family is good, and it really needs professionals to conduct a comprehensive combing.

First, pure pension annuity

This annuity is actually a fool's type of operation, that is, when you start to receive pensions at the age of 55 (female) and 60 (male), you can choose to pay monthly, annual, and payment periods, 3 years, 5 years, 10 years, and even some products can be paid for 15 years and 20 years. There are also some products that are delivered in 6 years, 7 years, and 25 years in order to treat them differently.

1. How do I choose the payment period?

It must be to see the pressure of payment that you can bear. For example, my customer, if you choose 3 years to pay, a year to pay about 400,000; 5 years to pay, a year to pay about 240,000; this is certainly unrealistic, choose 10 years to pay, a year also to 120,000; or choose 15 years to pay, a year 80,000; 20 years to pay, 60,000 feel less pressure to pay. However, the relative choice of products in 15 years and 20 years will be small, and the money received in the same period is certainly not as good as that in 10 years, more than 120,000.

2. Whether to choose life or start with the collection, after 20 years to receive the maturity payment is more cost-effective?

In fact, it depends on how much the maturity payment you receive? This will be different for each product, in my current example.

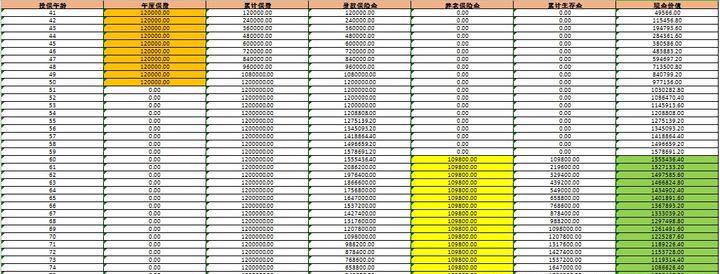

40 years old, female, 120,000 a year, pay for 10 years, 60 years old to start to receive, receive 109800 per year, after 19 years of collection, to 80 years old, receive a sum of 1098000 (10 times the maturity fee), then many friends say, 10,000 a month, 120,000 a year, this 109800 is not at all to 120,000 ah, can not meet the needs of customers.

But what everyone ignores is that the green row on the right, the cash value statement, from the beginning of collection, 20 years is the current price, until the 80th year of age to receive the maturity payment, there is no cash value. Therefore, the total value of the policy is actually 109800 received in the previous year + the cash value of the current year (155436.40), adding up to 260,000. But the peak actually occurred in the 80th year, except for 109800 * 19 + 1098000 (10 maturity deposit) = 3.18 million, compared with the investment of 1.2 million, the actual increase was more than 2 times.

3. What is the situation if you choose lifelong?

Similarly, we can see that the annual receipt of 114360, more than before 4560, 19 years is equal to 86640, but the 20th year of maturity is 1098000, equal to 80 years old, more than 897 000 for life, at the current rate, at least nearly 8 years to catch up, that is, to almost 88 years old, then can not live so long, whether the family has longevity genes, and for many elderly people at this age, if they are sick and hospitalized, it is really difficult to say How much will it cost, and people without children, if they don't go to the pension community, they also need to hire a caregiver, these are the places that need to spend money, so in fact, 80 years old to receive the maturity payment, for my current customer should be more suitable for her than the lifelong continuous withdrawal of money.

In addition, for female friends who may want Dink for a lifetime, it is best to choose insurance that can bring a pension community, because income is one aspect, and there is a relatively good environment after old age, there are good medical conditions, which can save a lot of worries and let the elderly spend their old age with peace of mind.

Some products belong to the lifetime collection, although the annual collection may not be so much, but the cash value of the collection is very high, the total value of the insurance policy exceeds the product I am talking about now, but it is not necessarily the total value of the policy that is the highest must be the first choice, the functional attributes are many times, but also an important factor that customers value, a product, the number of years to choose, the choice of collection methods, the pension received, and the functional attributes, then this product will definitely be audienceed to most of the customers.

4 How good is it to receive, or is it necessary to receive it well, but the account continues to have cash value, all the way to life?

That's actually a pretty good question? Let's take a look at the following two products.

We can see that assuming the same situation, 60 years old to start to receive, each year to receive 107520, is the least to receive, but look at the right of the yellow line, you will find that this product has a lifetime cash value, that is, you can choose to surrender at any point in time, receive your current price, and although it seems that every year will be less than 10,000, but after 19 years, the account will still have a cash value of 880080, so in fact, the total value of the policy is the highest of all the products at present. This kind of is actually very suitable for friends who have longevity genes at home and have inheritance requirements, although this inheritance can only be guaranteed to receive 20 years, and then there is no death, but you can surrender the current price when you are not in good health, leave it to your children, obviously for women, the probability of living older is much greater than that of men, so this is actually more suitable for married women with children, do not need some other functional attributes, completely want their own interests.

Look at the following chart, the annual premium is close to 120,000, pay for 10 years, from the age of 60 to receive, the annual collection is about 116820, the premium paid is less, the collection is also the most recommended products above, but look at the cash value of the rightmost green line, from the beginning of the second year after the beginning of the collection there is no current price, that is, how long to live to get, can not surrender, is completely their own fate in their own hands, but from the total interest of the total policy, it should be the lowest, This is also a lot of salesmen to customers to say that we get a high amount of money every year, this high is actually a high with the loss of cash value to win the high, not the real sense of high. So everyone must have polished their eyes to see clearly, not a verbal promise, but a real cash value statement.

Today I will introduce so much to you, the next topic is still pension annuity, but the structure of the insurance policy will be different. See you next time, see you next time.