The PMI has fallen, and it is time to start a "new" round of economic stimulus

Zeping macro

2024-05-31 21:39Posted in Beijing Finance and Economics Creator

Text: Ren Zeping's team

The manufacturing PMI in May was 49.5%, the previous value was 50.4%; The non-manufacturing PMI was 51.1%, compared with 51.2% in the previous month.

1 The PMI has fallen, and it is time to start a "new" round of economic stimulus

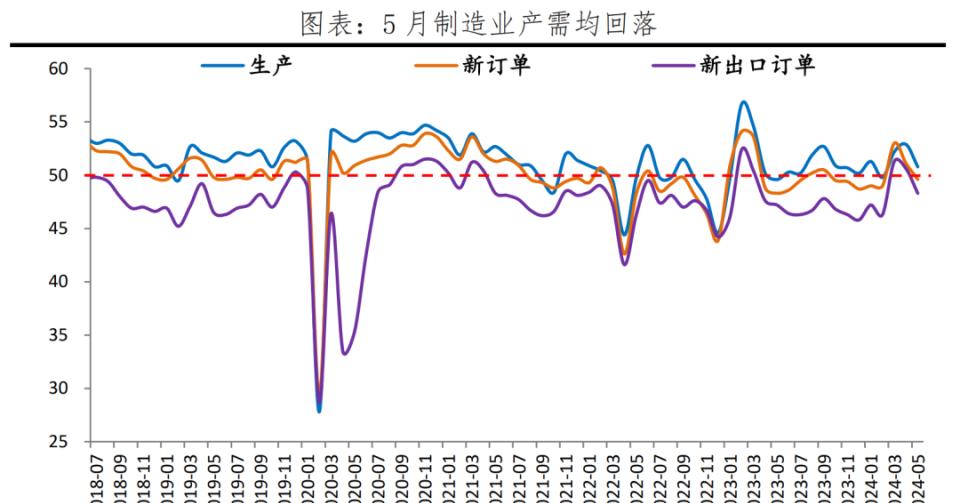

In May, the manufacturing PMI fell back to the boom and wither line, and domestic demand was insufficient. New orders in manufacturing declined, and property sales fell narrowly, but remained weak; The decline in production, high-tech manufacturing and construction is related to the lag in the effect of fiscal expenditure.

The 430 Central Political Bureau meeting emphasized "relying on the front" and "effective implementation", and the 517 epic real estate "combination punch" was implemented, and ultra-long-term treasury bonds were issued in May, but the policy effect lagged behind.

The progress of fiscal bond issuance is slower than in previous years, which is related to the decline in local government bonds and high-quality projects, which affects the pace of infrastructure investment in the early stage. From January to May, the issuance of special bonds was 28.2% of the year, and accelerated in May; According to the Ministry of Finance, the issuance of 1 trillion yuan of ultra-long-term special treasury bonds was completed in mid-November, and so far, a total of 80 billion yuan has been issued on May 17 and 24.

Real estate is still facing a more severe environment, the supply side is waiting to be cleared, and the demand side is subject to residents' employment and income; Policies have been introduced in an all-round way, including collection and storage, relaxation of purchase restrictions, and lowering interest rates and down payment ratios. The bottom of the policy appears, but the key to the bottom of the real estate market is the improvement of residents' purchasing power and expectations, boosting employment and income, and a "new" round of economic stimulus. (Refer to "Epic Positive, Is Real Estate Saved This Time?") 》)

Initiate "new" economic stimulus and "new infrastructure", that is, through fiscal expansion and monetary easing, expand demand, drive employment, and stimulate economic growth, while increasing support for the new economy and new quality of productivity, so as to enhance long-term competitiveness. Consideration can be given to: transformation and upgrading of traditional industries; new energy, artificial intelligence, digital economy and other emerging and future industries; the establishment of a housing security bank; Encouraging childbearing, for example, can boost short-term demand and increase total factor productivity without leading to surplus. (See "It's Time for a 'New' Round of Economic Stimulus.")

China's economic development potential is huge, as long as substantial and effective measures are taken to develop new quality productivity, new infrastructure and new energy, boost confidence in the stock market and property market, protect the vitality of the private economy, and liberalize and encourage childbirth, confidence will be greatly boosted, and confidence is more important than gold. In this way, there is great hope for our economy.

2 The PMI data for May showed the following characteristics:

1) The manufacturing PMI in May was 49.5%, down 0.9 percentage points from the previous month. Both production and demand have declined, and they are weaker than seasonal; The production index was 50.8 percent, down 2.1 percentage points from the previous month, and the new orders index was 49.6 percent, down 1.5 percentage points.

2) The new export orders index was 48.3%, down 2.3 percentage points from the previous month. South Korea's exports and Vietnam's exports increased by 1.5% and 12.9% year-on-year respectively in the first 20 days.

3) The U.S. manufacturing boom continued to expand, and the euro area manufacturing PMI rebounded. The Markit manufacturing PMI in the United States was 50.9%, up 0.9 percentage points from the previous month, while the manufacturing PMI in the euro area and Germany were 47.4% and 45.4% respectively, up 1.7 and 2.9 percentage points from the previous month.

4) Bottom of the inventory cycle. The inventory index of raw materials and finished products was 47.8 percent and 46.5 percent respectively, down 0.3 and 0.8 percentage points from the previous month; the inventory of finished products in April was 3.1 percent year-on-year, a slight rebound for five consecutive months, and the bottom fluctuated. In terms of prices, driven by rising commodity prices, the purchase price index of major raw materials was 56.9%, up 2.9 percentage points from the previous month.

5) Real estate sales are weak, and the epic real estate "combination punch" has landed. In May, the number and area of commercial housing transactions in 30 large and medium-sized cities were -38.5% and -38.3% year-on-year, and -38.6% and -38.9% respectively in April, narrowing the decline for three consecutive months. The key to the bottom of the real estate market is the improvement of residents' employment and income.

6) The expansion of the construction sector has slowed down, and the service sector has rebounded, but weaker than seasonal. The business activity index of the construction industry was 54.4 percent, down 1.9 percentage points from the previous month, and the business activity index of the service industry was 50.5 percent, up 0.2 percentage points from the previous month, boosted by the May Day holiday.

7) The employment index of manufacturing and non-manufacturing enterprises was 48.1% and 46.2% respectively, with a change of 0.1 and -1.0 percentage points from the previous month, respectively, and the PMI of large, medium and small enterprises was 50.7%, 49.4% and 46.7% respectively, with a change of 0.4, -1.3 and -3.6 percentage points from the previous month.

3 Both production and demand in the manufacturing industry fell

The manufacturing PMI in May was 49.5%, down 0.9 percentage points from the previous month, and the prosperity fell into the contraction range, with orders being the main drag. At present, the foundation for the recovery of production and demand is not solid, and the lack of aggregate demand is the main problem.

1) The production index and new orders index in May were 50.8% and 49.6% respectively, down 2.1 and 1.5 percentage points from the previous month. New export orders were 48.3%, a sharp drop of 2.3 percentage points. On the production side, the production of general equipment, railways, ships, aerospace equipment, computers, communications, electronic equipment and other industries continued to expand; The production of textile, chemical fiber, rubber and plastic products and other industries has slowed down significantly. On the demand side, the demand for food, wine and beverages, refined tea, metal products, railways, ships, aerospace equipment, electrical machinery and equipment continued to expand; Demand from papermaking, printing, cultural, educational, sports, aesthetic and entertainment products, petroleum, coal and other fuel processing industries weakened.

2) The U.S. manufacturing boom continued to expand, and the euro area manufacturing PMI rose. The US Markit manufacturing PMI was 50.9% in May, and the April PMI was revised upward to 50.0%; The manufacturing PMI of the euro area and Germany were 47.4% and 45.4% respectively, up 1.7 and 2.9 percentage points respectively from the previous month. South Korea's exports in the first 20 days of May were 1.5% year-on-year; Vietnam's exports were 12.9% year-on-year.

3) The inventory cycle is still oscillating at the bottom. The inventory of raw materials, finished products and purchases were 47.8%, 46.5% and 49.3% respectively, down 0.3, 0.8 and 1.2 percentage points from the previous month. The economic momentum index was 3.1%, 0.7 percentage points lower than the previous month.

4) Continued improvement in business expectations. The expected index of production and business activities was 54.3%, down 0.9 percentage points from the previous month, still in the expansion range. From the perspective of industries, the expected index of production and business activities in industries such as agricultural and sideline food processing, food and wine and beverage, refined tea, special equipment, and electrical machinery and equipment continues to be in a relatively high boom range.

5) The high-tech manufacturing industry and the equipment manufacturing industry maintained prosperity expansion, both of which were 50.7%, down 2.3 and 0.6 percentage points respectively from the previous month.

4 Prices are rising, and global bulk prices are rising

In May, the purchase price index and ex-factory price index of major raw materials were 56.9% and 50.4% respectively, up 2.9 and 1.3 percentage points respectively from the previous month.

Commodity prices rose across the board. Crude oil prices fell, non-ferrous metals continued to rise, and black prices rebounded. As of May 30, the South China Industrial Products Index rose by 2.6% month-on-month, down 0.9 percentage points from the previous month.

Crude oil prices fell. As of May 31, the prices of Brent Dtd and OPEC basket crude oil in the United Kingdom fell by 8.9% and 6.1% month-on-month, down 14.5 and 11.9 percentage points from the previous month.

The continuous rise in non-ferrous metal prices is related to the increase in demand for new energy vehicles, the shortage of supply and speculative sentiment. As of May 31, LME copper and LME aluminum prices rose by 6.9% and 2.5% month-on-month respectively, down 2.4 and 9.9 percentage points from the previous month.

The operating rate of petroleum asphalt and cement prices have risen, and the prices of coal and steel have rebounded. As of May 30, the cement price index rose by 2.6% month-on-month, up 2.3 percentage points from the previous month, the operating rate of petroleum asphalt was 1.1% month-on-month, an increase of 11.1 percentage points from the previous month, the prices of coking coal, coke and the closing price of thermal coal in Huanghua Port increased by 4.6%, 5.7% and 5.9% month-on-month respectively, up 3.7, 6.6 and 12.2 percentage points from the previous month, and the average monthly increase of rebar was 3.3%, up 4.3 percentage points from the previous month.

Gold and silver prices continue to rise. As of May 29, COMEX gold and silver prices rose by 1.0% and 7.2% month-on-month, respectively, down 6.9 and 4.4 percentage points from the previous month.

5. The foundation for the recovery of production and demand of small and medium-sized enterprises is not solid

In May, the PMI of large, medium and small enterprises was 50.7%, 49.4% and 46.7% respectively, a change of 0.4, -1.3 and -3.6 percentage points from the previous month. Large enterprises maintained an expansion trend, but many indicators of small and medium-sized enterprises have fallen, and they still need to be vigilant against problems such as insufficient demand to stabilize the recovery momentum of small and medium-sized enterprises.

1) The production and demand of large enterprises continue to expand. The production index was 52.7 percent, down 0.1 percentage points from the previous month, and the new orders index was 51.6 percent, up 1.0 percentage points from the previous month. New export orders were 48.1%, down 1.9 percentage points.

2) The production of medium-sized enterprises continued to expand, and the prosperity of export orders was better than that of overall orders. The production index was 50.8 percent, down 2.6 percentage points from the previous month, and the new orders index fell 2.3 percentage points to 49.6 percent. The new export orders index was 50.2%, down 2.0 percentage points from the previous month.

3) The indicators of small enterprises have fallen sharply, and policy stabilization is still needed. The production index was 56.4 percent, down 6.0 percentage points from the previous month, and the new orders index fell 6.4 percentage points to 44.8 percent. The index of new export orders fell by 4.4 percentage points to 45.2%. The foundation for recovery is not solid, and policy support is still needed.

6 Construction activity slowed and orders retreated

The non-manufacturing business activity index was 51.1% in May, down 0.1 percentage points from the previous month. The index of new orders in the non-manufacturing industry was 46.9 percent, up 0.6 percentage points from the previous month, and the index of business activity expectations was 56.9 percent, indicating a relatively high level of prosperity.

The business activity index of the construction industry was 54.4%, down 1.9 percentage points from the previous month. The business expectation index was 56.2%, still in the relatively high prosperity range. From the perspective of market demand and labor demand, the new orders index and employment index of the construction industry were 44.1% and 43.3% respectively, down 1.2 and 2.8 percentage points from the previous month. In terms of prices, the input price index and sales price index of the construction industry were 53.6% and 49.7% respectively, up 1.4 and 1.0 percentage points from the previous month.

The issuance of new special bonds has accelerated, with 28.2% of the full year completed, but the issuance progress is lower than expected. From January to April, the scale of new special bonds issued nationwide was 56.78 billion yuan, 346.59 billion yuan, 230.75 billion yuan, and 88.32 billion yuan respectively, with an average monthly issuance of 180.61 billion yuan, and 438.35 billion yuan of new special bonds were issued in May.

The business activity index of the service sector was 50.5 percent, up 0.2 percentage points from the previous month. In terms of different industries, the business activity index of postal, telecommunications, radio and television and satellite transmission services, Internet software and information technology services, culture, sports and entertainment and other industries was above 55.0%, while the business activity index of capital market services, real estate and other industries was running at a low level. New orders and business activities are expected to be 47.4% and 57.0% respectively, a change of 0.9 and -0.4 percentage points from the previous month.

View original image 223K

-

The PMI has fallen, and it is time to start a "new" round of economic stimulus -

The PMI has fallen, and it is time to start a "new" round of economic stimulus -

The PMI has fallen, and it is time to start a "new" round of economic stimulus -

The PMI has fallen, and it is time to start a "new" round of economic stimulus -

The PMI has fallen, and it is time to start a "new" round of economic stimulus -

The PMI has fallen, and it is time to start a "new" round of economic stimulus -

The PMI has fallen, and it is time to start a "new" round of economic stimulus