summary

. Unity has developed a business model that allows them to generate revenue throughout the game's lifecycle, including after development and post-release.

. Unity has always put growth above profitability to gain significant market share, which can translate into significant profitability.

. Unity seeks to benefit from significant market growth as its technology finds significant applications outside of the video game space.

Today, Unity's business is dominated by the game space. Over the next decade, as other segments grow, video games may be only a fraction of the company's overall sales.

Unity ( NYSE: U ) is a software developer currently focused on the game space. However, as the technology continues to evolve, Unity is exploring alternative applications of its technology. These alternative applications can provide extraordinary growth opportunities for Unity, which is already growing rapidly. This article will explore the company's current and future business, as well as its financial position, to determine if it is worth investing in.

Operational Solutions

Before getting into Unity's game engine, I want to discuss operational solutions. It's a less exciting part of unity's business, but given that it accounted for 65 percent of the company's sales last quarter, it should be a major focus for a lot of investors. As the name suggests, the division focuses on assisting game developers and publishers with game operations. That is, Unity's Operational Solutions division assists in monetization through Unity ads and in-app purchases.

Since most mobile games are free, monetization is a key part of its success. There are more than 2.2 billion active mobile gamers worldwide, 56% of whom play more than 10 times a week. To put it another way, that's 0.61 times as many people using social media globally. This is a huge market for developers, and Unity aims to facilitate this market.

The company's advertising program offers integrations in all typical formats, such as banners, videos, and interstitial ads, that developers can integrate into their games. The company's advertising service also allows developers to introduce monetization across all app stores in the same process, which greatly simplifies the process for publishers. While there's not necessarily anything particularly noteworthy here, Unity just does all of this very well to create a complete service for its customers.

Unity isn't just for game developers, though. The company also offers services to companies looking to advertise on mobile games. Unity offers targeted advertising, which it claims to be able to make advertising more effective because it has a large number of games available and therefore an incredible amount of data.

Unity's Audio Pinpointer is the primary tool for advertisers aiming to maximize their revenue. Similarly, with Unity's data of over 22 billion ad impressions per month and more than 2 billion monthly active users, the world's most popular mobile game ad service has a huge data advantage in this professional space.

Unity provides advertisers with the expected return on their targeted ads, giving them peace of mind and clear expectations. With a real-time valuation of each player, Unity's service segments ad spend to individuals. Unity has a clear advantage over its peers in the mobile advertising space, with more available data and higher utilization than anyone else, making it one of the company's standout products.

It should be noted that Apple (AAPL) is now trying to severely limit the way companies collect user data through their apps. That would be a nice blow to the Unity product, which basically promises the best positioning in the mobile gaming space.

While the company's leadership in the mobile gaming space (discussed later) will help retain customers, it's something investors need to be aware of. It should also be noted, though, that 78% of mobile games are made on Android devices, which means that this doesn't affect the vast majority of Unity's data pools.

In the U.S., the average smartphone game spends $137, while the average revenue generated per user is $131.21. The global mobile gaming industry generated more than $163 billion in revenue last year, proving the efficacy of these "free- to-play" games that can monetize their gaming experiences. Unity as a major enabler of this market is a very exciting opportunity.

Currently, the company is working on Unity Economy, a system for developers to create a more efficient in-game economy. Among other things, the goal of the service is to create an effective monetization strategy from which publishers can profit. Creating an effective economy is an important part of the fun of gaming, whether it's monetized or not, which makes it possible for this operational solution to be heavily used when it's released. The service will also automatically track players' inventory, including currency and items, to reduce publisher overhead.

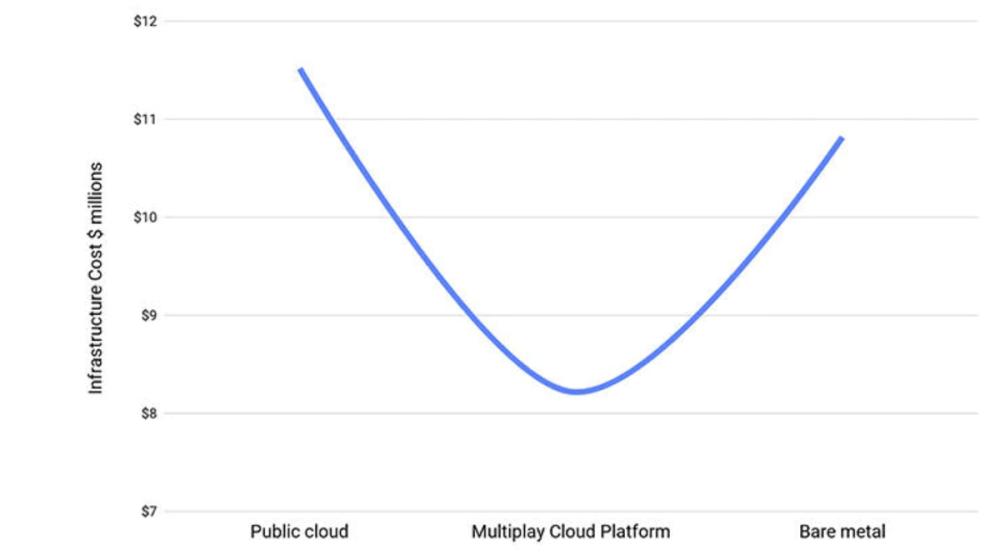

However, Unity doesn't just monetize its customers. Once the game is through the development phase, more needs to be done to get the game running smoothly, and unity's services can help make that happen. Multiplay is one of Unity's core products, and as the name suggests, it supports multiplayer experiences.

Multiplayer, especially when watching console or PC games, is one of the most common ways people enjoy gaming. This is especially true for more casual players, who may only enjoy the game for the company of friends rather than the actual content. Multiplay claims to be a cheaper alternative to the public cloud, with the performance needed for truly global gaming.

The company cites Electronic Arts (EA)'s wildly popular Apex Legends, a game that grew from 0 to 50 million users in 24 days as a prime example of the service's capabilities. Multiplay's servers are located around the globe and are designed to provide a premium experience for all game users, no matter where they are.

Unity

To enhance its multiplayer experience, Unity also offers Vivox, an in-game voice and text communication service. The service is used by many of the world's premier multiplayer games, such as Valorant, League of Legends, and PUBG. In terms of context, League of Legends has an average of 117 million unique users per month.

Unity is also currently beta testing its Robey service, which will enable players to join multiplayer servers in smaller groups. These can be invitation-only or open-ended. Lobbies are a major component of most multiplayer shooters, such as Apex Legends, and Unity's services are designed to reduce the development overhead and cost associated with enabling them.

More back-end capabilities build on the ability of economic services to maintain accurate records of player inventory. For example, Unity's Cloud Save allows game publishers to uninstall storage of players' game progress and status.

While emphasizing each of Unity's different services is a bit redundant, my goal is to be clear at this point. Unity's operational solutions span a wide range of products designed to improve or reduce the necessary operational overhead for game publishers. The company also doesn't limit the customer base of any of its services to those who use the Unity game engine to develop games.

Game engine

Although the company doesn't limit its users to those who have only used its gaming platform, it can still have some success if it does. 61% of mobile games were developed using Unity's game engine, making it the most popular mobile game engine in the world. There is a big gap. More than half of the world's games, including mobile devices, PCs, consoles, and VR, also use Unity's engine.

A game engine is essentially a framework for games that developers can piece together to create the final product. In a game engine, there are detailed physics simulations, animation systems, shading and shading details, sound systems, rendering—basically anything you need to get your game "running."

Although it was up to the game developers to take these multiple systems and emulate them and turn them into games. The engine is also responsible for communicating with the platforms that are playing it, whether it's iOS, Windows, or PlayStation. Without a generic engine like Unity, game developers will need to make new engines for different platforms and new games.

As you might imagine, creating an engine takes a lot of work, especially for small developers, and there's no real resource to do it, and that's where Unity comes in.

However, Triple-A or AAA studios don't always use pre-made engines like Unity. AAA Studios has the resources to develop their own engines, although they sometimes opt for hybrid systems. Let's say you're looking to develop a racing game. You may be happy with the shading and shading appearance of a given engine, but you need a more tuned physics engine and a more immersive sound.

In this case, it is not uncommon to develop various hybrid systems, where studios use certain aspects of the standard game engine, while also developing certain aspects that meet their needs.

However, in the game engine market, there are actually only two products to be aware of. Unity is certainly one of them. The other is Epic Games' (OTCPK:TCEHY) Unreal Engine. Between the two of them, responsible for the vast majority of games on the market. However, when it comes to AAA games that use pre-built game engines, Unreal Engine is usually the engine of choice.

Regardless, it's clear that Unity has a stronghold in the game engine space with its closest competitor, Unreal Engine, surpassing it only in console and PC gaming.

As of the end of 2020, games made on Unity have 2 billion monthly active users and are powered by 1.5 million monthly active creators. The company's game engine business model follows a subscription model, with developers paying per seat.

While the company's Operate Solutions aren't unique to games developed on Unity, the game engine certainly provides a good ingredient for Operate Solutions. About 65% of Unity's Operate Solutions customers also use the company's Create Solutions, demonstrating the high potency of this ingredient. As a result, Unity is able to monetize the creation and operation of the games it helps create.

In addition to its game engine, Unity maintains tens of thousands of assets for developers to use, which is an important asset for the engine.

Even AAA studios use some third-party assets in their games, rather than making them all themselves, because it would be more efficient to focus on creating proprietary assets that players will constantly interact with, rather than small things like fences.

On the Unity Asset Store, assets can be listed for free, but if not, the creator can set a minimum price of $4.99 for those assets. However, of the 75,372 assets listed on the Unity Store, only 7,343 or 9.74% are listed for free.

There is also often a significant difference in quality between free and paid assets, which means that developers often choose paid assets. Some of these assets were created by Unity, but most are not.

However, Unity charges a 30% revenue share on the assets listed in its store, some of which are priced in the hundreds of dollar range, and it provides a fairly reliable source of revenue. The exact number is unknown, and Unity didn't reveal much, except that when it was disclosed in 2014, top creators earned $30,000 a month.

Weta acquisition

For some who call themselves movie fans, Weta is a name that should have weight. Founded in 1993 by Peter Jackson, Richard Taylor, and Jamie Selkirk, VFX Studios is responsible for producing visual effects ("VFX") in Creatures of Paradise, and has been heavily involved in major blockbuster hits, including most Of the Marvel games, Avatar, and Demon King Rings.

The studio promotes motion capture using Golem characters and is now the technology's preferred home, garnering critical acclaim in the Planet of the Apes series, though its involvement in Avatar was probably the most influential. Responsible for the top two visual effects of the most successful films of all time, it's clear that the studio is one of the best films in the world. But what interest does Unity have in it?

Looking at Unity's press release announcing its intention to acquire Weta, the company said: "Ultimately, this acquisition aims to bring Weta's incredibly exclusive and sophisticated visual effects ("VFX") tools to millions of creators and artists around the world, and once integrated into the Unity platform, it can realize the next generation of RT3D [real-time 3D] creativity and shape the future of the virtual world." So, I would say the intent is clear. While the company's VFX business is quite strong, Unity's primary interest is in acquiring IP and talent.

Further potential

This is where things start to get exciting. Unity describes itself as "the world's leading platform for creating and manipulating interactive, real-time 3D content." I think the wording, especially without anything to do with the game, shows where Unity sees itself making progress. Now, mobile games don't translate well into metaverse-like apps, consoles or the engine behind PC games are more relevant.

Unreal's huge lead in the space may be a bit of a concern for investors, but Unity has been building a leading position in the XR space. In fact, according to Unity CEO John Riccitiello, the company's lead in XR even outpaces its lead in mobile gaming. Since the company holds more than 60 to 70 percent of the XR development market, I think it's safe to say that Unity currently dominates the space.

XR, or extended reality, is an umbrella term that encompasses both virtual reality ("VR") and augmented reality ("AR"), which is the space that many people expect virtual reality to occupy. For those who don't know, VR is a computer-generated experience designed to create a "virtual reality" by allowing the user to fully immerse themselves in another environment.

AR allows users to fully understand their real-world environment and often enhances the user's perception of their environment by providing supplemental information. Head-up displays, which are increasingly popular in high-end vehicles, are a good example, as is Apple's Animojis.

So it's clear that XR is well beyond the scope of video games, and Unity is taking full advantage of that. The company partnered with Audi (OTCPK:AUDVF) to develop the first VR car configurator and packaging training course case study detailing one of many potential applications.

Virtual training sessions allow companies to allocate more time to training employees on the right technology without having to invest more money. The company also partnered with PiXYZ in 2018 to develop a platform that leverages CAD files in real time. These are among others the measures the company has taken over the past few years to develop its XR capabilities beyond those offered by its peers. The lead unity has established is clear and looks long-lasting.

A recent report by Research and Markets estimates that the XR market value will reach $397.81 billion by 2026, up from $25.84 billion in 2020. While much of that value will go to companies that are developing a variety of spatial applications, Unity does stand up to the fact that it has benefited greatly from this growth by positioning itself as the leading platform for developing these applications. Based on industry multiples, 60% of the global XR engine market (the low end of the company's current market share estimate) could be worth $6.7 billion by 2026.

By 2026, I don't think Metaverse will be a widely used platform yet. Instead, I expect much of the company's XR business to come from a combination of gaming and niche commercial applications. However, transitioning to the metaverse, Unity has more room for explosive growth. Since XR is a platform for building virtual worlds, Unity's foothold as a leading vendor of XR development solutions provides excellent growth opportunities in the medium to long term.

Unity Simulation Pro and Unity SystemGraph are probably the most important steps Unity has taken in developing mass-market applications developed based on its 3D content. Simulation Pro is a high-performance simulation platform that generates "faster than real-time simulations, enabling developers to do more iterations and tests, accelerating their time to insight at a fraction of current operating costs." According to tests at Carnegie Mellon University, the platform's simulation processing speed is 2,400% faster than the standard process. This increased processing efficiency allows universities to shorten training programs from weeks to days.

These simulations can be used in a variety of applications, including robotic automation and autonomous vehicle training. The speed and accuracy with which Simulation Pro can generate a variety of environments may also have some fidelity for creating virtual environments, such as those that virtual environments try to occupy.

In its XR and real-time 3D capabilities, Unity is now also trying to bridge the gap for live sports. Unity uses volumetric capture technology to partner with UFC to provide viewers with an unparalleled experience. By creating a live-action digital twin, Unity aims to give viewers the ability to see action from any angle they choose, even the warrior's own perspective.

UFC provides a solid testing ground for Unity because the limited environment and limited players reduce the number of variables that companies must consider. It's unclear how long it will take for this technology to become commercial, but it's these goals that are starting to provide context for the types of impact Unity could have outside of video games. Morgan Stanley analyst Matthew Cost estimates that TAM for non-gaming applications could bring $25 billion worth to Unity in five years.

Financial metrics

The chart below shows the company's cash flow since 2018 and shows that there is no outstanding consistency. However, this is mainly due to some unusual events that have occurred since Unity went public. This includes the Company's initial public offering, which netted $1.418 billion for the Company, the acquisition of Weta, which resulted in a loss of $1.58 billion for the Company, and the issuance of convertible notes, which resulted in a net profit of $1.725 billion.

Long Term Tips

Regardless of the anomalous events, a company cannot be expected to maintain any form of cash flow if it cannot generate stable profits. The following diagram depicts Unity's EBITDA since 2018. You may notice that, unlike a company's cash flow, there does seem to be a recognizable pattern here. The trend here is clearly negative, as Unity's operating expenses continue to balloon despite the increase in revenue.

Long Term Tips

However, despite this, the company's current assets remained at $2,151 million at the end of 2021. Investors may be concerned about interest payments from taking on $1.725 billion in debt, but convertible notes in 2026 will not pay interest. At a conversion price of $308.72 per share, the notes also assume a considerable appreciation in Unity's current share price.

Issued the day before Unity hit an all-time high, I would say management was quite opportunistic in issuing these convertible notes, which provided the company with ample liquidity without resulting in significant dilution or burdening it with high interest. Down more than 50% from an all-time high, the original 57.5% premium on convertible note pricing is now close to 250%.

As a result, with $2.151 billion in liquid assets and a cash burn rate of several hundred million dollars per year, Unity is currently in a strong financing position. Honestly, the company's market debt ratio is only 0.06, which also means it has a lot of room to raise more money with more debt if needed, and to make up for it through equity if the difficulties persist.

Although if Unity continues on a positive path, it won't worry about it in the short or even medium term. However, just because a company isn't on the brink of financial bankruptcy doesn't mean profitability isn't important. To be a valuable growth company, there must be evidence that this growth can be translated into profitability at some point.

Valuation discussion

Nine years ago, Quora posted about Unity's business model and how it makes money, to which founder David Helgason responded: "I have to admit, it's a bit outdated. We make money primarily by selling Unity software to our large and small customers (in that order) and getting a small percentage of our 30% commission from the Asset Store. After that, it's just tiny bits and pieces. We don't publish our revenue figures, but we've made a lot of profits from it all, and the growth has been very strong. That's the last point I want to focus on.

Unity was profitable in its early stages. However, now generating hundreds of millions of dollars in sales, the company is unable to make a profit. What went wrong? The simple answer is: No. In today's dynamic market, we've always seen unprofitable companies win over companies that are only generating static profits at an astonishing rate of growth. Whether this is true or not is a completely different question, and the question this article focuses on is the extent to which investors should value this growth.

However, Unity is now a very different company than it was nine years ago. In terms of its profitability today or years to come, its profitability doesn't really mean squatting. For now, one of the company's biggest expenses seems to be stock-based compensation.

The company's total stock-based compensation for the most recent quarter was $97.8 million, representing 30.9% of the company's total revenue. As the company continues to add more employees rapidly, with a 31 percent increase in headcount last year, employee-related expenses, such as stock pay, will only continue to grow. However, Unity's revenue is growing faster.

With a 43.77% increase last year, the company's revenue exceeded the increase in new hires, which was its biggest expense. In addition, according to widespread expectations, the company's revenue is expected to grow by another 34.8% next year. As sales grow, profitability increases as expenses begin to become less important relative to earnings. Analysts currently expect Unity to eventually turn a profit in the second quarter of 2023 as Unity continues to grow.

The key question now shifts from whether Unity is profitable to how much growth Unity can really sustain. This has been briefly discussed in the discussion of the impact of stock-based compensation, but I'll explore it in more depth here. As of the fourth quarter of 2020, when Unity last offered an update, 94 of the top 100 game development studios ranked by revenue were Unity customers.

In addition, 71% of the first 1,000 mobile games were developed using Unity. The second metric is up significantly from 2019, when the software company was responsible for developing 53% of the top 1,000 mobile games. In 2019, the company also maintained 93 of the top 100 game development studios for customers. While no specifics were provided this time, Unity claims its market share continues to rise in its recent filing.

However, top game developers aren't the only ones making money for Unity. The company focuses on customers generating more than $100,000 in revenue as one of its key growth metrics. In 2021, the customer base grew from 739 in 2020 to 973 in 2021, an increase of 31.7%.

In addition, Unity's spending has also grown dramatically within its existing customer base. The company's U.S. dollar-based net expansion rate was 133% in 2019, 138% in 2020 and 140% in 2021. This sustained and extreme growth proves that Unity is not only maintaining existing customers, but also doing well. The game engine market is expected to grow at a CAGR of 13.63% from 2020 to 2027, providing strong growth for Unity's core business.

But let's go beyond the business units that the company has established. While this growth is quite remarkable, I'm more interested in revenue from non-gaming apps. Still in the early stages of adoption, the company currently comes only 25% of its sales from non-gaming apps. However, last year's $1.1 billion in sales increased by 70% compared to 2020. The $1.1 billion is also well below the $6.7 billion that Unity is likely to generate by 2026.

While Unity may have started by building an accessible and high-quality game engine, it has evolved into more than just a game company. I'm not sure how many outsiders are already aware of this. Just as GPUs are no longer considered primarily gaming products, so will these engines. As for what this means for companies like Unity, consider NVIDIA (NVDA). The King of GPU, originally a niche product, looks set to be the first semiconductor company to reach a market capitalization of $1 trillion.

Currently, Unity's average price target is $150.38, and only one of the 18 analysts covering the company has a rating below "Hold."

risk

Whenever there is an investment theme that relies heavily on significant growth, there are significant risks. Some or many of these opportunities may not materialize at all as expected. If this is indeed the case, Unity will most likely continue to struggle with profitability, and the company will need to make significant changes to its business and operations. As existing employees flee toxic and uncertain environments, mass layoffs often become the end point of a company's growth.

In addition, as with any high-growth sector, Unity may face some competition. Now, Unity does have a strong product and talent moat, which makes the barrier to entry fairly high, but it can still be broken.

Microsoft (MSFT) and Meta (FB) could be huge customers, and given their desire to develop virtual environments, they could also become competitors. Both companies have a large number of resources, including talent, that they can use to simply exclude Unity.

However, I believe Unity's services will deliver higher quality at a lower cost. Years of leadership can't really be bought, unless, of course, it becomes an acquisition target. As Microsoft seeks to strengthen its gaming business, Unity is sure to be a target of interest to them.

Investor advice

I love Unity, but it's expensive. In a way, I can't help but think of the original dot-com bubble.

That being said, I think it's too early for Unity. The company already has a very strong presence in the gaming industry and is making the right investments to develop the applications of its industry-leading products. Returning to the comparison of GPUs, industry insiders foresee that the industry will expand dramatically as new technology advances require products. For me, Unity offers investors the same opportunity to participate in major industry developments.