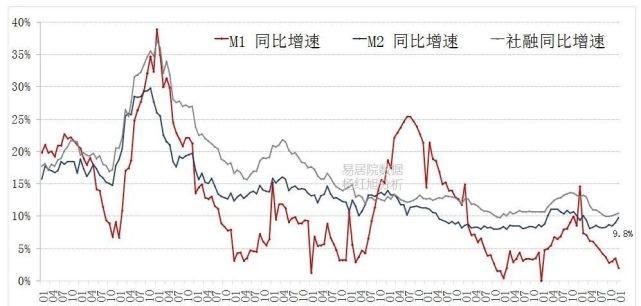

In January, the credit release opened well! The scale of new loans is the highest in history! M2 and social finance growth rebounded, M2 increased by 9.8% year-on-year, significantly better than expected, mainly due to the central bank's RRR cut, interest rate cut policy effect, off-balance sheet financing convergence, fiscal continued strength, obviously promoted credit creation, promote M2 year-on-year rise. The balance of M1 decreased by 1.9% year-on-year, excluding the impact of the spring festival timing factor, M1 increased by about 2% year-on-year. Lao Yang expects to recover to around 3.7 percent in March. Overall, under the guidance of stability, steady progress, and economic policy, the financial environment continues to improve, which is good for cyclical stocks and the property market!

Next, look at the transaction volume of second-hand houses in seven typical cities in January. In Shanghai, the transaction volume of second-hand residential buildings in January was 15,000 units, compared with 18,000 units in the previous month, a significant decline. However, January is affected by the Spring Festival factor, which is normal compared to December. Overall, although the current Shanghai property market is significantly stronger than 99% of the country's cities, the volume and energy are still below the boom-bust line and are still in the adjustment period. Neither joy nor worry.

In Beijing, the transaction volume of second-hand houses in January was nearly 12,000 units, which was significantly lower than that in December, but higher than that in January 2019 and 2020. Basically stable. The key is to see where you can stand in March. It is no problem to re-enter the boom-bust line. The probability of house prices tending to rise slightly in a stable manner is large.

Shenzhen, the transaction volume of second-hand residential buildings in January was 1557 units, a new low in nearly a decade! From the perspective of volume and energy, the current Shenzhen property market is in an extremely cold state! Such a downturn, rare in history, is the inevitable result of the retreat of investors. The market is elastic, easy to go crazy when it rises, and easy to be miserable when it falls. March small Yang Spring, should not expect too much...

Chengdu, second-hand housing transaction volume, December and January, two consecutive months of explosive volume. Among them, there are the reasons for the centralized application for the previous backlog of mortgages, but what about other reasons? As far as the price of second-hand houses is concerned, the current formation is the initial pattern of decline. As a result, there is a divergence of volume and price, preferring to believe in the authenticity of price fluctuations.

Qingdao, the transaction volume of second-hand houses in January, still has no improvement, lying steadily on the floor, has lasted for 5 months bear-like. I have to admit a cruel and abnormal fact: in the whole of Shandong, the strongest city is Qingdao, and the weakest property market is also Qingdao! Quite strange, I don't know how Qingdao people and Shandong people see this matter?

Wuxi, the transaction volume of second-hand houses in January continued to hover at a low level. House prices are still falling. In the coming year, the risks remain large... Housing enterprises and individuals should be cautious.

In Foshan, the transaction volume of second-hand houses in January was slightly weaker, but it was significantly stronger than that of Dongguan. In October and November last year, the transaction volume of second-hand houses in Foshan cooled sharply, rebounding in December and January, but still below the boom-bust line. According to this amount of energy, Foshan's second-hand house prices should currently be a small decline. According to our 50-city monitoring system, overall, the current national property market continues to cool down, and the bottom of the market has not yet been established! But a few cities have largely bottomed out. This set of 50 cities real estate opportunity and risk monitoring system, research and development is very difficult, is still in the process of research, is expected to have preliminary results in March...