The U.S. Competition Act of 2022, passed by the U.S. House of Representatives on Friday, is nearly 3,000 pages long, the highlight of which is to allocate a huge investment and subsidy of $52 billion to expand the construction of chip factories in the United States, so it is also known as the "Chip Act". The content of the bill is not new, in June 2021, the United States passed the "2021 American Innovation and Competition Act", the core content is to research and encourage support for the development and manufacture of local semiconductors, and the "Chip Act" is just its continuation, changing the soup does not change the drug, the essence is not new, from this point of view, the "Chip Act" or a performance project of the Biden administration.

1. Umbrella

If the Chip Act is likened to a cake, then the Biden administration, domestic U.S. multinationals, and non-U.S. multinationals with similar interests are cake-splitters with knives and forks in their hands.

The Biden administration is naturally the one who wants the biggest piece of the pie, and it desperately needs a big cake to prove its ability to govern.

At the beginning of Biden's presidency in early 2021, the US government faced five major economic problems, including saving the US economy, tackling income inequality, convincing the American people to tackle climate change, how to end the trade war, and dealing with the monopoly of technology giants.

A year later, the biden administration handed over the answer sheet, basically did not answer the above five major problems, involved, but only dragonflies a little water. Still, in his January 2022 speech, Biden gave an A+ to his year in office, praising himself for his performance "probably exceeding everyone's expectations," and then pie-up the American people: "The best days in this country are still ahead." ”

When Biden said this, the number of confirmed cases of new crown pneumonia in the United States on the same day was still as high as 850,000, inflation caused public dissatisfaction, and the confrontation between the two parties made unity a bubble. The latest poll released by the Associated Press that night showed that only 28 percent of Americans want Biden to be re-elected, and even within the Democratic Party, that percentage is less than half (48 percent), and that midterm elections will be held on November 8, 2022. That is to say, if Biden has not yet achieved his achievements in 2022, the Democratic Party's seats in the House and Senate will also be affected, and whether Biden can run for re-election will be dragged down after that.

Under the clouds, the Biden administration urgently needs to find an umbrella, and the "chip bill" is such an umbrella. If the bill is successfully implemented, the $52 billion subsidy will be in place without discount, and the investment and employment of the US semiconductor manufacturing industry will not be negligible. TSMC's fab using 5nm process technology built by TSMC in Arizona, USA, invested about $12 billion, created 1,900 full-time jobs, and upfront subsidies of $205 million, according to which it is estimated that the "Chip Act" can drive investment in the U.S. semiconductor manufacturing industry will be hundreds of billions of dollars, solving tens of thousands of jobs. For the Biden administration, this is a solid and self-congratulatory performance.

In addition, the "chip act" is plainly in response to the voice of the US big consortium. Since December 2021, executives from more than 50 companies, including Ford Motor Company, General Motors, Apple and Intel, have sent letters to the U.S. Congress urging the passage of the Chip Act. The major shareholders of these large multinational companies are all major us conglomerates, they are supporters of the Democratic Party, important contributors to campaign funds, and the passage of the "Chip Act" is equivalent to receiving a big gift, and the Democratic Party can get the bonus points of the consortiums in the next midterm elections or the next president.

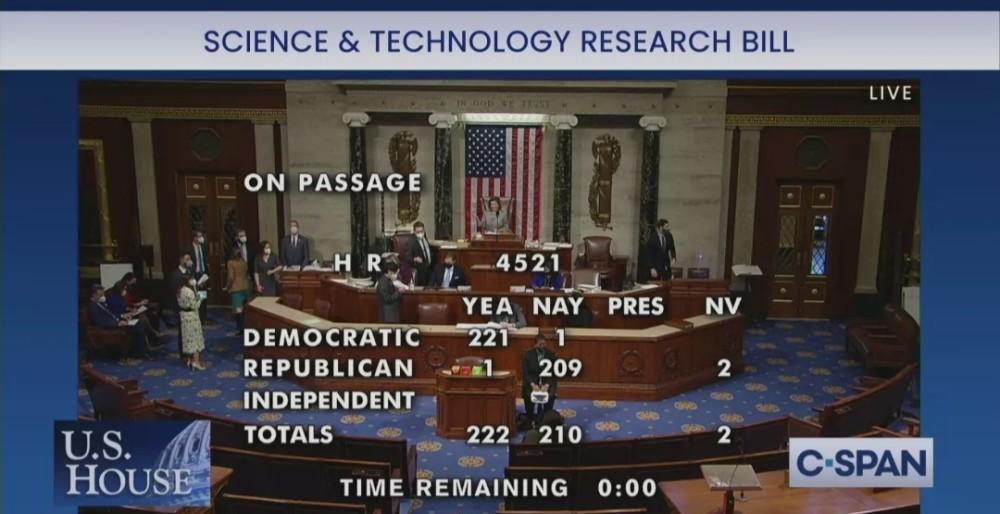

The "Chip Act" has strong performance engineering attributes, and it can also be peeked at from the passing situation tube. Judging by the number of votes cast, the Democratic majority of the House of Representatives voted 222 votes in favor and 210 votes against the bill, of which there was only one Republican who voted in favor and only one Democrat who voted against, in other words, the votes for and against were completely divided according to party. For Republican lawmakers, there is really no incentive to support the Democratic government's performance project.

Second, what are the advantages of american semiconductors

The "Chip Act" claims to strengthen U.S. control over chips and maintain a competitive advantage over China's high-tech industry, which is actually the political foundation that the Biden administration has put on its face for its political achievements, because in the semiconductor field, the United States is in a dominant position, and no one can shake this position at present.

From the perspective of specialized division of labor, the global semiconductor supply chain includes basic research, EDA/IP, chip design (subdivided into logic devices, DAOs and memory), semiconductor manufacturing equipment and materials, wafer fabrication, back-end packaging and testing.

Let's look at the 2018 data comparison to see how competitive the United States is in the semiconductor industry.

In terms of semiconductor basic research (mainly including the research of basic materials and chemical processes), the industry's more common view is that basic research accounts for 15 to 20% of total semiconductor R&D investment, and the United States has maintained a level of 16 to 19% for many years, while China's investment in this area is only 5 to 6% (OECD data in 2018), about one-third of that in the United States.

In terms of EDA/IP, according to the SIA report, the United States accounts for 74% of the share, while China has only 3%, the former is nearly 25 times the latter. A visual example of the gap is that cadence, Mentor and Synopsys, the three giants of EDA, are all American companies.

Chip design is subdivided into logic chip design, DAO (discrete devices, analog devices and other categories of devices) design, memory chip design, three tracks, the United States occupies an absolute advantage: logic chip design market, the United States share of 67%, China is close to zero; memory chip design market, the united States share of 29%, China is 7%, the former is more than 4 times the latter; DAO design, the United States share of 37%, China accounted for 7%, the former is more than 5 times the latter.

In terms of manufacturing equipment, the United States accounts for 41%, representing companies such as LAM (Lam Semiconductor), AMAT (Applied Materials) and KLA (Ketian Semiconductor), all of which are industry giants, while China accounts for 5%.

In the field of semiconductor manufacturing materials, the United States accounted for 11%, and China's data was 13%.

In the field of semiconductor packaging and testing, the United States accounted for 2% and China accounted for 38%.

Analysis of the above data can be seen that the United States occupies the vast majority of the entire industrial chain, in the highest value-added design and front-end manufacturing also occupies the advantage, the competitive advantage in the global semiconductor industry chain is in a hegemonic position, and in the basic research of high-intensity investment, coupled with semiconductor is a technology, capital and talent-intensive industry, once a company or country / region establishes a competitive advantage, it is difficult to be surpassed in the short term.

Three, two hands

The United States maintains an absolute competitive advantage in the semiconductor industry, while controlling the industry with an invisible hand, the visible hand has never been idle, before there was a "entity list" of Chinese high-tech enterprises such as Huawei, and then there was a "data blackmail" incident.

In particular, in the name of solving the chip shortage, the U.S. Department of Commerce asked more than 20 global chip companies, including TSMC and Samsung, to provide chip supply chain data to them in September 2021. After a series of struggles, silence, or verbal resistance, the companies concerned finally submitted their data before the deadline set by the United States. Even large foreign companies such as TSMC and Samsung have to obediently obey orders, which shows the strength of the United States' administrative control of the global semiconductor industry chain, and there is no second in Bluestar.

The United States, with the hand of the market and the hand of the administration, has maintained absolute control over the global semiconductor industry, in this case, talking about maintaining a competitive advantage over China, it is obviously to find reasons and find reasons, so that the "chip bill" can be smoothly landed and the performance project will blossom.

The question now is, if the "Chip Act" allows TSMC and Samsung to land smoothly in the United States, what impact will it have on the industry?

As we all know, the high labor cost in the United States, coupled with the fact that the American union is not a fuel-saving lamp, in order to continuously increase the labor cost as a mission, the main reason why GM has closed its local factories in succession is that the labor cost driven by the union has soared, and it is eventually overwhelmed. Will the semiconductor manufacturing giants repeat the mistakes of the past? The answer is unlikely, because TSMC, Samsung and General Motors, unlike each other, are monopoly giants, and they can use their dominant position in the market to digest the rise in labor costs caused by the construction of factories in the United States, in other words, the global market will pay for the rise in the cost of chips made in the United States.

Another foreseeable trend is that due to the return of developed countries to wafer manufacturing, the global division of labor network of the semiconductor industry will be split, and the prosperous era of designing semiconductors in Europe and the United States and manufacturing and testing in Asia will enter the twilight.

——END——