The important market of 5G is the vertical industry, and the 5G to B market is a new growth point to promote the sustainable development of enterprises. In the face of the market, users, competition and the future, how to better promote the high-quality development of 5G to B has become an important issue for operators at present and in the coming period, which requires a correct understanding of the current development characteristics and development laws of China's 5G to B market. This article will explore the six core issues of the current development of China's 5G to B market.

What are the driving forces behind the 5G to B market?

The author believes that there are four major driving forces for the development of 5G to B in China - policy drivers, technology drivers, competition drivers and demand drivers.

● Policy drivers

Since China officially issued 5G licenses on June 6, 2019, the state has intensively introduced relevant policies, such as the "5G + Industrial Internet" 512 Project Promotion Plan promulgated in November 2019, the "Notice on Promoting the Accelerated Development of 5G" and the "Notice on Accelerating the Development of the Industrial Internet" in March 2020, and the "5G Application "Sail" Action Plan (2021-2023) jointly issued by the Ministry of Industry and Information Technology and other ten departments in July 2021. In addition, in recent years, provinces, municipalities and districts have issued more than 570 relevant policies to support the development of 5G, which are all measures that the state actively supports and vigorously promotes the development of 5G in China. It can be said that policy support is the first driving force for today's achievements in the development of China's 5G integrated applications.

● Technology drive

Compared with 3G/4G, 5G has the characteristics of high bandwidth, low latency, high reliability and wide connectivity, which truly opens a new era of interconnection of all things and human-computer interaction, especially the integration of 5G with new technologies such as AI, big data, cloud computing, Internet of Things, edge computing, and blockchain, which can meet the communication needs of industrial manufacturing, automatic driving, drone control, telemedicine, smart cities and other fields, and truly become a new engine to promote the digital transformation of the industry. It can be said that 5G is born for the industry, and the development of 5G technology is an important force to promote the development of 5G to B.

● Competitive drivers

China's 5G network operators mainly include China Telecom, China Mobile, China Unicom and China Radio and Television. Nowadays, the four major operators are fully promoting 5G network construction, user development, integrated application innovation, industry application benchmarking, and ecosystem construction, and there is competition and cooperation.

Operators not only face competition in the same industry, but also face cross-border competition and challenges. Huawei, ZTE, Ericsson, Nokia Bell and other equipment manufacturers are strong competitors in the 5G to B market; Tencent, Ali and other Internet companies are actively involved in 5G private networks and other fields, and are also strong competitors in the future 5G to B market. In addition, with the implementation of the licensing system for the frequency of 5G private networks by the state, the self-built private networks of enterprises will also become a major trend in the development of 5G private networks, which will undoubtedly erode the 5G private network market of operators. In short, to a certain extent, competition is an important force driving the development of China's 5G to B market.

● Demand drivers

User demand is the fundamental driving force for the development of the 5G to B market. At present, the rapid development of China's 5G to B market is largely driven by policies, 5G is not the majority of vertical industry users just need, many companies believe that the current optical fiber, 4G and Wi-Fi can basically meet the information and communication needs of enterprises, coupled with the current real economy is facing difficulties, 5G huge cost investment inhibits the demand for 5G. At present, the development of the 5G to B market is in the stage where supply exceeds demand and supply creates demand, and the whole society also needs to work together to truly make demand-driven the first driving force for the development of the 5G to B market.

The above analysis shows that the current development of China's 5G to B market is mainly driven by policies, the author believes that only when demand-driven becomes the first driving force for development, China's 5G to B market can really achieve explosive growth, and the 5G industry can truly achieve sustained and healthy development. It is expected that after 2023, the demand for 5G to B market will show a gradual growth trend.

What stage is the development of China's 5G to B market?

China's 5G license has been issued for more than 2 years, 5G to B development continues to make breakthroughs, in such a situation, correctly grasp China's 5G to B market development in what stage, for operators to develop development strategies, promote 5G to B high-quality development is of great significance.

Judging from the current situation of the 5G to B market, one of the important reasons for the use of 5G technology by users in many industries is to obtain government subsidies. Although the application of China's 5G industry is showing a booming trend, the market acceptance is constantly improving, but the market penetration rate of the 5G industry is low, the 5G penetration rate of industrial enterprises above designated size is only about 5%, the 5G to B market has not really been stimulated, and the development of 5G to B is still in the introduction period.

China's 5G to B development is still in the stage of industry application benchmarking. According to the current development status of China's 5G empowerment and 5G integration applications, the author believes that China's 5G to B development is in the stage of industry application benchmarking. For example, the current users of the 5G to B market are mainly leading enterprises in the industry and large companies with strength, such as Baowu Group, Midea, Ningbo Zhoushan Port, Sany Heavy Industry, etc., with the purpose of achieving the purpose of scale replication through the leading role of large companies. A number of national policies and documents propose to build a number of industry-specific application clusters and carry out pilot demonstration actions for intelligent manufacturing. It can be seen that although China's 5G commercial development has made great achievements, the development of the 5G to B market is still in the stage of industry application benchmarking.

The application development of China's 5G industry is still in the development stage of scenario-based application. Through the analysis of various 5G industry application cases that have emerged in recent years, 5G mainly meets the needs of vertical industry users for remote control, information acquisition, high-definition images and video processing and other scenario-based applications. For example, the application scenarios of 5G in smart ports mainly include remote control of loading and unloading operations, unmanned transportation at ports, 5G intelligent tally, 5G smart yards, video surveillance and AI identification in the port area, etc. At present, these applications have been widely used in Shanghai Yangshan Port, Ningbo Zhoushan Port, Xiamen Yuanhai Terminal, Shenzhen Mawan Port, realizing the application of 5G full scenarios, and improving the level of port automation and intelligence.

In summary, at present, China's 5G industry application is still in the introduction period of development, 5G to B development is still in the stage of industry benchmarking application case creation, still in order to meet the vertical industry user scenario application needs, which requires operators to firmly grasp the opportunity of industrial digital development, adhere to the user-oriented, to help vertical industry users digital transformation, to achieve quality reduction and efficiency improvement as the goal, accelerate the large-scale promotion of benchmarking application cases, and continuously improve the penetration rate of 5G in vertical industries.

What is the essence of 5G development?

Products are the basis for the survival and development of enterprises, enterprises can only achieve sustainable operation if they continue to develop good products for users and realize product value. So what does China's 5G development ultimately rely on? As long as everything returns to its business roots, the answer is obvious, and that is the product.

To achieve better development of China's 5G industry, the key is to create value for users, deliver value and realize value. The word "value" here refers to the creation of good products and solutions for industry users, which can help industry users achieve quality improvement, cost reduction, efficiency and emission reduction. Therefore, for operators to have a good development of 5G, it must be product-driven, application-driven, platform-driven and solution-driven. Deepening the structural reform of the 5G supply side and creating good products and solutions is the foundation of 5G development.

The author believes that the good products provided by operators for vertical industry users refer to 5G solutions that meet the personalized needs of users, which objectively requires operators to adhere to user orientation, realize the transformation from "selling networks" to "selling services", and strive to provide users with "private network + terminal + platform + application" 5G overall solutions with 5G digital platform as the core.

Can 5G grow into the "second curve" of corporate growth?

The process of sustainable development of enterprises is essentially the process of constantly creating a "second curve". The so-called "second curve" is future-oriented growth, and it is the growth of the "first curve" that spans discontinuity before it reaches its peak. The reason why the company can continue to grow is because it can find the "second curve" again and again.

Over the past two years since the commercial use of 5G in China, 5G development has made great achievements. As of September 2021, China's 5G base stations have reached 1.159 million, 5G package users have reached 624 million households, the number of 5G terminal connections has reached 450 million, the number of 5G industry application innovation cases has exceeded 12,000, 5G + industrial Internet projects have reached 1,800, and 5G private networks have exceeded 2,300, and 5G has been widely used in industrial manufacturing, medical treatment, energy, transportation, logistics, steel, ports, agriculture and other industries.

With the rapid growth of 5G user scale and the continuous expansion of the depth and breadth of applications in the 5G industry, the contribution of 5G to operators' revenue growth has gradually emerged, mainly reflected in the following three aspects.

First, the penetration rate of 5G exceeds 20%, and operators have entered a new stage of user growth and increased commercial returns. In 2020, China's 5G penetration rate will reach 20.2%, marking that 5G has entered a stage of rapid development and will surely bring sustained revenue growth to operators.

Second, the growth of 5G users drives the growth of traffic and effectively improves the mobile ARPU. In the first three quarters of 2021, the ARPU of mobile users of China Mobile, China Telecom and China Unicom reached 50.1 yuan, 45.4 yuan and 44.3 yuan respectively, an increase of 2.45%, 2.25% and 6.49% respectively year-on-year.

Third, 5G is widely used in vertical industries, driving the rapid growth of operators' cloud computing, industrial Internet and other new business revenues. In the first three quarters of 2021, the digital revenue of China's telecom industry reached 74.09 billion yuan, an increase of 16.8% year-on-year, and the revenue scale and market share remained industry-leading; China Mobile's DICT business revenue for the industrial Internet was 48.9 billion yuan, accounting for 7.5% of the total revenue, and China Unicom's industrial Internet revenue was 40.925 billion yuan, an increase of 25.3% year-on-year. At the same time, operators' new services such as smart home, cloud computing, big data, and the Internet of Things maintained rapid growth. For example, China Telecom's smart home income in the first half of 2021 reached 7.2 billion yuan, an increase of 32.9% year-on-year; Tianyi Cloud's revenue reached 13.987 billion yuan, an increase of 109.3% year-on-year.

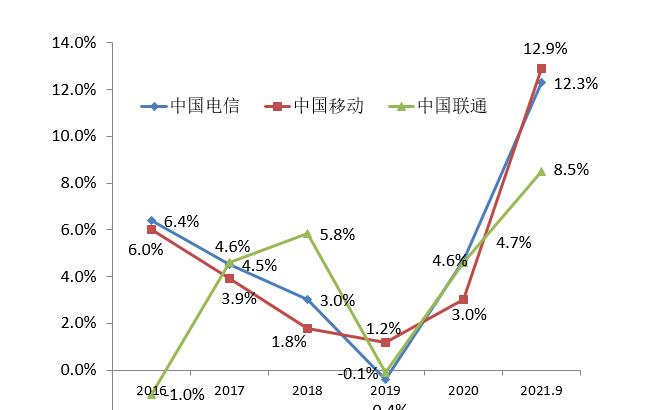

It is the rapid development of 5G that has enabled operators to grow revenue out of the trough and achieve a "V" reversal. As can be seen from Figure 1, the operating income growth rate of the three major operators fell into a trough in 2019 and showed a negative value. After 2019, the revenue growth rate of the three major operators has gradually increased, achieving a bottoming rebound. In the first three quarters of 2021, the revenue growth rates of China Telecom, China Mobile and China Unicom reached 12.3%, 12.9% and 8.5% respectively. It can be said that the development of 5G has enabled operators to hand over a bright report card. Today, 5G is becoming a new engine to drive operator performance growth.

Figure 1 Changes in revenue growth rate of the three major operators from 2016 to 2021

From the perspective of market opportunities, enterprise development strategies, and 5G development practices, 5G is expected to become the "second curve" of operators, but there is a point that needs to be particularly explained that the current contribution of 5G to operators' revenue growth mainly comes from the rapid growth of 5G to C user scale, which in turn drives the rapid growth of traffic and the steady increase of mobile ARPU, and the contribution of the 5G to B market to revenue growth is not outstanding enough. Since the revenue growth dividend brought about by the expansion of individual users has a "ceiling" effect, the most critical thing about whether 5G can become the "second curve" of operators in the future is to see how the 5G to B market develops. It can be said that 5G to B determines the success or failure of operators' future transformation. All parties in the industry should summarize the development status of the 5G to B market, systematically promote from the aspects of strategy, industry insight, technological innovation, application innovation, model innovation, management innovation, mechanism and system innovation, and continuously improve the cohesion, innovation, control, execution and competitiveness of the 5G to B market.

How to innovate and break through the 5G business model?

The immature 5G business model is a prominent problem restricting the development of 5G at present. The unclear 5G business model is mainly manifested in: for the 5G to B market, operators' products and services are still at the level of providing network connectivity, and the development, construction and operation of the 5G digital platform still have a long way to go; the 5G to B market demand has not really exploded, and the 5G to B market is still in the introduction period; the 5G industry terminal and module prices are high, and the industry terminal ecology has not yet formed; there is still a threshold for 5G cross-border integration, and the diversified profit model has not yet been formed; the 5G industry has developed in semiconductor chips, There is still a "card neck" problem in key electronic components, and the security of the 5G industry chain supply chain still faces the risk of changes in the global market environment; the 5G development investment is large and the effect is slow, and the effect has not changed.

In order to solve the problem of 5G business model, we must first correctly understand what is a 5G business model. At present, people generally believe that the 5G business model is a profit model, which is a misunderstanding of the 5G business model. The 5G business model refers to the overall business model of 5G operators forming an ecological community through the integration of internal and external elements according to a clear strategic positioning, and in the process of meeting the needs of users' 5G applications, they can achieve win-win cooperation and sustained profitability among all parties in the ecosystem.

According to the above definition, the success of the 5G business model should be judged by a comprehensive assessment of the innovation of 5G products and solutions, the influence of the digital platform, the health of the ecosystem, and the sustainability of profitability. Looking at the development of China's 5G to B in recent years and many typical industry application cases, the 5G to B market business model is evolving in accordance with the overall architecture of the 5G business model, and the future development is worth looking forward to. In order to better promote the innovation of 5G business models, the industry should focus on the following points.

First of all, operators should change from "selling networks" to providing 5G overall solutions for vertical industry users. Operators should stand in the user's position, consider from the perspective of the overall digital transformation of the enterprise, embed the whole process of production and operation such as enterprise research and development, production, manufacturing, sales, etc., and provide users with a 5G closed-loop overall solution of "private network + platform + terminal + application" to help vertical industry users improve quality and efficiency.

Second, create an open and win-win 5G industry ecosystem based on core capabilities. Operators should exert efforts in the following three aspects.

The first is to reshape core competitiveness. On the basis of consolidating the advantages of its own brand, users, networks and channels, we will reshape our core competitiveness and focus on improving our scientific and technological innovation capabilities, cross-border integrated operation capabilities and 5G end-to-end industry solution capabilities.

The second is to build an influential 5G digital platform to bring together industry chain partners with a platform. Platform and ecology are twin brothers. To build a 5G industry ecology, the focus is on building an influential industry digital platform.

The third is to do a good job in value distribution. In order to achieve the long-term and effectiveness of ecological cooperation, operators should adopt an active value distribution policy, and can explore a joint investment and construction, revenue sharing-oriented development model, so that partners can gather around.

Third, actively explore diversified profit models. Diversified profit model is based on a rich product system, operators should break through the "connection thinking", to provide users with the overall solution to build a digital platform as the core, only to create a rich product system and solutions for users, in order to fundamentally broaden the 5G diversified profit model.

Finally, achieve innovation leadership and promote pilot demonstrations of 5G applications. All parties in the 5G industry chain should work together to focus on key industries such as the industrial Internet, telemedicine, transportation and logistics, and energy, strive to create 5G vertical industry application demonstration projects and benchmarking application cases, realize product upgrades, capability upgrades, ecological upgrades, and service upgrades of industry benchmarking cases, and accelerate the large-scale replication and promotion of 5G benchmarking cases.

How does the organizational operation management model support the rapid development of 5G?

The innovation of 5G operating model should follow the law of enterprise development, so as to better support the development of 5G scale. To sum up, the law of organizational model change mainly has the following points.

First, small headquarters and large markets. This requires streamlining and optimizing the headquarters of enterprises, strengthening the planning, command, coordination and service functions of headquarters, highlighting the market operation main position of provincial and municipal companies, specialized companies, research and development institutions and various strategic units, and making the market bigger and stronger industries.

The second is flexibility and flattening. The core of flexibility and flattening is to make adaptive adjustments to the organizational model of enterprises in the face of complex and changeable market environments, and improve the rapid response ability of enterprises to meet user needs. Flexible organizational structure requires flexible leadership, decentralized decision-making, full authorization, flexible establishment of various types of market operators, and the use of digital technology to achieve organizational flattening and information flow and sharing.

The third is specialization and coordination. To continuously meet the needs of users, enterprises need to build a professional organizational model, establish a well-trained 5G professional team, strengthen the coordination of various organizational units, form a horizontally integrated organizational system, and further enhance the ability to quickly meet user needs.

Building an efficient organizational management model, Huawei's experience is worth learning. In 2021, Huawei established five legion organizations: coal mines, customs and ports, smart roads, data center energy, and smart photovoltaics. The legion model is to bring together scientists, technical experts, product experts, engineering experts, sales experts, delivery and service experts engaged in basic research in one department, shorten the cycle of product updates, and quickly adapt to industry needs. Using a clan model can break down existing organizational boundaries and quickly assemble resources. Although the legionnaire model is not much staffed, it is extremely effective.

The development of 5G can be said to be a comprehensive test of operator transformation and upgrading. In the post-epidemic era, in the face of the development of digital technology and the increasingly uncertain VUCA environment, it is urgent to accelerate the construction of an enterprise organization model that adapts to the development of 5G. To this end, the author suggests that the operator group headquarters should take the "small headquarters" reform as the goal, strengthen the group's strategic guidance and overall command functions; promote professional operation in accordance with the requirements of "small", establish various 5G independent operating bodies, and fully authorize; for coal, ports, steel and other industries with large market potential and relatively mature applications, we can learn from Huawei's legion model and establish institutions such as "coal legion", "port corps" and "steel corps" at the group company level to serve coal, ports, steel and other enterprises across the country In order to improve the rapid response ability to meet user needs as the goal, under the overall planning of the group company, strengthen the leading role of R & D institutions and specialized companies in product innovation, strengthen the efficient collaboration between market-oriented research and development, technology, sales and other 5G business entities, never let the front line fight alone; cultivate and build a team of 5G technical experts, industry experts, product experts, sales experts and solution experts who can fight a hard battle, and better enhance the ability to meet the overall 5G solution needs of vertical industry users It is necessary to adhere to the correct assessment orientation, increase incentives, continuously stimulate the innovation vitality of various 5G independent management bodies, and jointly create organizational value in the 5G era.

Overall, China's 5G development potential is huge, and all parties in the industry need to work together to exert the agglomeration effect and promote the vigorous development of the 5G to B market. At the same time, we should also soberly realize that China's 5G development is still facing huge challenges, and the external environment is still severe and complex. It is believed that with the support of national policies and the joint efforts of all parties in the industrial chain, China's 5G industry will certainly develop better, faster, stronger and more prosperous.

![When the hardware drive gradually slows down, can the phone be faster?[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)