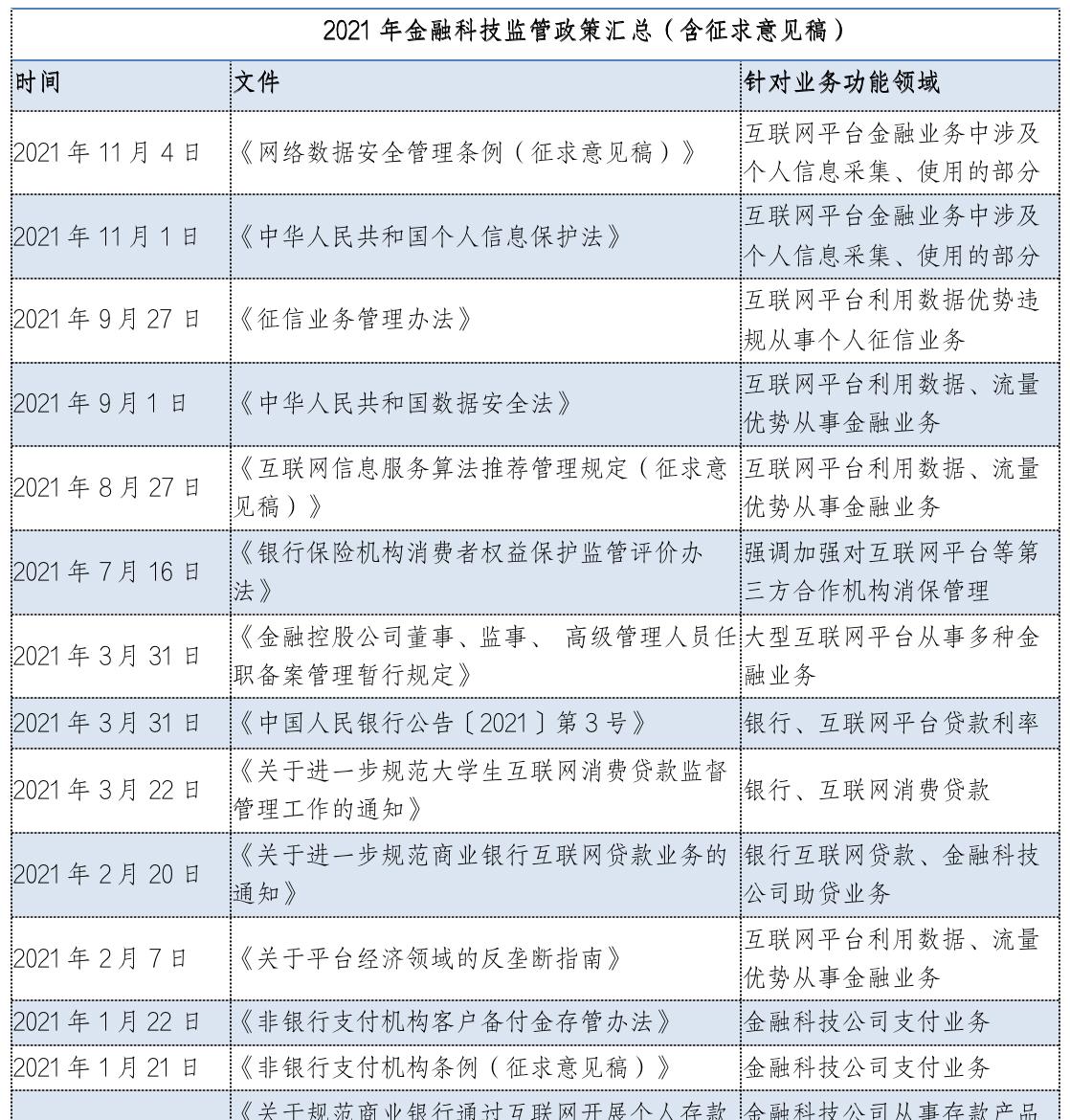

At the end of the central bank's "FinTech) Development Plan (2019-2021)", how to steadily develop financial technology and accelerate the digital transformation of financial institutions is a mandatory question in the digital finance industry in the past year. At the beginning of the year, the tone of strong supervision, the entire 2021 digital finance field compliance rectification has become the main theme, ushering in the adjustment of a number of business areas, at the end of the year, on the last day of 2021, we take you to review the many changes in the field of digital finance in the past year.

Standing in front of the new course of digital finance development, we can see that with the normalization of "strong supervision" and the deepening of cross-border integration of "technology + finance", a new and standardized future financial picture is being reshaped. In 2022, digital finance will achieve high-quality development in the direction of innovation and development in a steady manner and effectively serving the real economy.

NO.1 Compliance rectification into the main theme, strong supervision and stable development of the two prongs

Interviews, rectification, compliance operations, fintech giants have ushered in unprecedented regulatory attention in the past year. Fourteen platform giants were asked to rectify thousands of issues related to business areas such as payment, loan assistance, and data protection. Regulators have repeatedly spoken out, pointing out the compliance issues such as lax protection of personal information, illegal advertisements, high interest rates, and student loans on various platforms, and continue to safeguard the legitimate rights and interests of consumers.

The central bank's 2021 work summary mentioned that for the financial business of large Internet platforms, the two key points of this year are "strengthening supervision" and "supporting development". In the past year, the regulatory level has repeatedly emphasized that it is necessary to resolutely promote anti-monopoly and prevent the disorderly expansion of capital, insist that financial business must be operated with a license, incorporate all financial activities into prudential supervision, and guide and urge 14 leading online financial platforms to conduct in-depth self-examination and rectification of violations. To this end, the regulatory level has also issued a series of relevant policies in 2021.

NO.2 emphasizes "no license and no finance", and leads to the replenishment and expansion of gold companies

While digital technology is changing traditional financial services, there are also problems such as lack of supervision and regulatory arbitrage. Some large technology companies have the phenomenon of disguised financial services such as lending, asset management, credit investigation, and loan assistance without a license.

It can be seen that it is more obvious that the compliance development signal of consumer finance business has gradually emerged during the year. 2021 has become a year of frequent capital increases for consumer finance companies and small loan companies, and more new entrants have emerged, and consumer finance licenses have been expanded. In the view of industry insiders, on the one hand, the capital increase is to meet the corresponding regulatory requirements, on the other hand, it is still optimistic about the future market in the field of consumer finance.

According to the incomplete statistics of Nandu reporters, since 2021, a number of consumer finance companies, including Hangzhou Bank Consumer Finance, Suyin Kgi Consumer Finance, Zhonglian Consumer Finance, Beiyin Consumer Finance and Ant Consumer Finance, have increased capital to "replenish blood". In order to meet the regulatory requirements for microfinance companies operating online microfinance business across provincial-level administrative regions with a registered capital of not less than 5 billion yuan, a number of small loan companies have also increased their capital. According to incomplete statistics, Meituan Small Loan, Tencent's Tenpay Small Loan, JD.com Small Loan, AndteDance's Zhongrong Small Loan, etc. have all completed the requirements of capital increase to 5 billion yuan during the year.

At the same time, there are many new entrants. Since 2021, Suyin KGI Consumer Finance, Ant Consumer Finance and Vipshop Fubon Consumer Finance have been approved to open, and the industry's licensed army has also expanded to 30. Didi and Bank of Ningbo also invested in Hangzhou Bank Consumer Finance and Huarong Consumer Finance in March and December respectively, thus obtaining consumer finance licenses.

NO.3 Strengthen antitrust and prevent "winner-take-all" of large technology companies

2021 is the first year of the "14th Five-Year Plan" and the "big year" of anti-monopoly work, and the anti-monopoly work in the field of digital finance is also frequent, starting with the "Regulations on Non-bank Payment Institutions (Draft for Comment)" issued by the central bank in January and the rectification of Ant Group.

According to the rectification requirements of the competent financial departments, the first is to return to the origin of payment and strictly prohibit unfair competition; the second is to operate personal credit reporting business in accordance with the law and in accordance with the law and in accordance with the law, and protect the privacy of personal data; the third is to establish a financial holding company in accordance with the law, strictly implement the regulatory requirements, and ensure the adequacy of capital and the compliance of related party transactions; the fourth is to improve corporate governance, strictly rectify financial activities such as credit, insurance, and financial management in accordance with the requirements of prudent supervision; fifth, carry out securities fund business in accordance with the law and in accordance with the law, and strengthen the governance of securities institutions. Carry out asset securitization business in compliance.

Subsequently, the 14 companies interviewed began to steadily rectify their credit products. Among them, Ant's "Huabei" and "Borrowing" successively launched brand isolation in November, gradually handed over the two businesses to the newly established Ant Consumer Finance Company to undertake in an orderly manner, and guided the original two small loan companies to achieve a stable and orderly market exit.

N0.4 Loan interest rate "clearly marked price", welcome the 24% interest rate "new red line"

While emphasizing strict supervision, strengthening consumer protection is also the focus of work in 2021, and the supervision has strictly controlled excessive marketing such as encouraging advanced consumption and illegal financial advertising on Internet platforms. Among them, the central bank issued an announcement in March, requiring all institutions engaged in loan business to display the annualized interest rate to the borrower in an obvious way when marketing through websites, mobile applications, posters and other channels, and specify it when signing the loan contract, and can also display daily interest rates, monthly interest rates and other information as needed, but should not be more obvious than the annualized interest rate. The "clear price marking" of credit products is interpreted by the market as further maintaining the order of market competition and protecting the legitimate rights and interests of financial consumers.

At the same time, this year's supervision further reduced the loan interest rate, and many local regulatory departments provided window guidance to consumer finance companies under their jurisdiction, requiring the annual interest rate of credit products to be reduced to less than 24%, and the annual interest rate of consumer finance companies and small loan company products was mostly close to 36%. Under the requirements of supervision, the credit products launched by a number of consumer finance companies have controlled the interest rate within 24%, which has also triggered a 24% "new red line" pressure drop in the credit products operated by various types of capital providers, but the sharp compression of profits has led to some small loan companies withdrawing from the credit market this year. It is worth noting that in judicial practice, courts also make judgments at a maximum annual interest rate of 24%.

N0.5 Financial data governance difficulties to be solved

In 2021, new laws related to financial data security have been introduced, and the most important asset in the current development of digital finance is data, and the digital transformation of financial institutions also needs to tap the value of data, and how to achieve innovative and steady development within the scale of security and compliance has become a new topic of the times. In the future, financial institutions urgently need to think about how to improve the data governance mechanism, strengthen data privacy protection, release the value of data safely and compliantly, and strive to seek new opportunities in the new situation.

In the view of industry experts, the current financial data governance rules are still not perfect. First, the use of financial data is not standardized, and privacy protection is insufficient. Some large technology companies over-collect user data, mix data on various product lines, and do not clearly define the scope of data use, infringing on user data privacy. Second, there are deficiencies in the openness and fairness of data. Some large technology companies hinder the migration of user data to competitors, because the data is not open, some small and micro enterprises and individual industrial and commercial households are difficult to provide their own platform data to commercial banks to obtain direct credit and lending, and can only rely on the joint lending or loan of large technology companies. Third, the ownership of data still cannot be effectively defined, and what responsibilities and constraints should be borne by various types of participating entities still need to be improved in terms of laws and systems.

NO.6 The curtain of personal credit reporting marketization has opened

In the field of consumer finance business, problems such as data islands and long-term lending caused by imperfect credit reporting systems and intensified competition gaps are not uncommon. This year, the "Measures for the Administration of Credit Reporting Business" was officially promulgated, which will further enhance the level of marketization, rule of law, and science and technology of the credit reporting industry, and promote the healthy and orderly development of the credit reporting market.

It is worth noting that this year, under the background of the country's gradual promotion of the steady development of the credit reporting market, the curtain of the marketization of personal credit reporting has gradually opened. In February, the second market-oriented personal credit reporting agency Park Dao Credit Was officially opened, and at the end of the year, the third personal credit reporting agency, Qiantang Credit, also began to prepare, and the central bank has accepted the company's personal credit business application. This makes up for the lack of marketization of personal credit information, internet lending information on credit information and other personal alternative data are not covered.

NO.7 Regulatory sandbox breaks the ice, and the first batch of pilot projects in many places are "out of the box"

Since September 2021, Beijing, Shenzhen, Chongqing and other places have successively announced that the first batch of projects of the financial technology innovation supervision pilot project have officially "come out of the box", which marks that the Chinese version of the "regulatory sandbox" has completed the "last kilometer" in the construction of the mechanism, forming a complete work closed loop, and is a milestone event in the development and maturity of China's financial technology regulatory mechanism. This is an important step in China's financial technology innovation supervision pilot, indicating that the financial technology innovation supervision work has entered the normalization stage from the pilot stage.

Up to now, 9 regions across the country, including Beijing, Shanghai, Shenzhen, Guangzhou, Hangzhou, Xiong'an, Chengdu, Chongqing and Suzhou, are carrying out pilot projects for financial technology innovation supervision.

NO.8 Blockchain + privacy computing has become a hot spot in the development of the industry

In 2021, financial technology will gradually return to the origin of science and technology to serve finance and help the rapid development of the real economy. The core technical elements represented by artificial intelligence, blockchain, cloud computing, and big data ("ABCD") are an important foundation for the development of fintech infrastructure, providing a driving force for breaking the difficulties of "information asymmetry" and "high transaction costs" in traditional finance.

KPMG China recently released the "2021 China Leading Fintech Enterprises 50" report, pointed out that in the past year, the development of blockchain technology has shown an explosive growth trend, its decentralized, immutable and trustless attributes have provided a trust foundation for the development of financial technology, and the landing in the financial field has a certain scale and application scenarios. The combination of blockchain and privacy computing is one of the hot spots in the development of the industry, and the combination of the two can achieve the effect of "1+1>2". The report points out that at present, private computing is still facing the challenges brought about by the "interconnection" problem caused by data security, algorithm acceleration, large-scale application and algorithm differences, and there is still room for development in the future in the direction of industry standard construction and technological breakthroughs.

NO.9 Sound the clarion call for rural digital inclusive finance

This year, digital inclusive finance was written into the No. 1 document of the central government for the first time, setting off a nationwide upsurge in the development of rural digital inclusive finance and sounding the clarion call for the development of rural digital inclusive finance. More and more counties are exploring the introduction of new technologies for the financial industry and helping rural revitalization with the help of digital finance. Recently, the Institute of Rural Development of the Chinese Academy of Social Sciences released the "China County Digital Inclusive Finance Development Index Report 2021", which pointed out that digital credit has become a key area of digital inclusive finance at the county level after the continuous popularization of digital payment in counties and rural areas.

It is worth mentioning that through the use of cloud computing, satellite remote sensing, IOT and other digital technologies, farmers' agricultural insurance, planting conditions and other data have become the basis for reflecting their credit and business conditions, and the rural customers that were originally the most difficult to identify have more accurate digital portraits, digital credit ratings and digital credit, expanding the user base for rural use of digital credit.

NO.10 Digital Yuan Multi-point Blossom into the Winter Olympics "Science and Technology" Business Card

Since the beginning of this year, Beijing, Shanghai, Guangzhou and other places have successively written the development of the digital yuan into the government work report. At present, the digital yuan has been piloted in Beijing, Shenzhen, Suzhou, Shanghai, Xiong'an, Chengdu, Hainan, Changsha, Xi'an, Qingdao, Dalian 11 places and the 2022 Beijing Winter Olympics scene, digital yuan red envelopes, the cumulative amount of more than 340 million yuan, some cities have also launched digital yuan green travel, low-carbon red envelopes and other use scenarios. As of October this year, there were more than 3.5 million digital yuan pilot scenarios, with a total of 123 million personal wallets opened and a transaction amount of about 56 billion yuan. At the same time, the digital yuan has moved towards a cross-border payment function.

Some research institutions believe that the digital yuan will be the "technology" business card of the Winter Olympics, and the digital yuan is also expected to drive China's digital currency to usher in new development opportunities in the Beijing Winter Olympics scene. According to the work conference arrangement of the Chinese Minmin Bank in 2022, the steady and orderly promotion of the digital yuan research and development pilot is also one of the key tasks.

【Conclusion】

Looking back at the development of digital finance in this year, under the background of strong supervision, compliance rectification has become the main theme, bidding farewell to the era of barbaric growth of mixed fish and dragons, and entering a new stage of standardized, healthy and sustainable development.

During the year, the introduction of regulatory policies in various subdivisions improved the construction of the institutional system from the top-level design. The rectification of the head enterprises has set up a sample for the industry to develop compliance, and has also brought a fairer competitive environment to the market. In addition, focusing on the development of digital inclusive finance, improving financial data governance, financial consumer rights protection, the landing and application of cutting-edge technology finance, regulatory technology and digital yuan research and development pilots and other important directions, encouraging and supporting innovative development is still the same direction.

Looking forward to 2022, the development of digital finance will take the word "stability" as the first word, innovate and develop in a steady manner, and implement the "real" place to continue to serve the real economy with the power of science and technology.

Written by: Nandu reporter Xiong Runmiao

![The advantages of renting a house in Hangzhou to choose a brand single apartment are: 1. good privacy, single-family households do not disturb each other, 2. complete facilities, cooking, laundry and washing do not disturb each other, 3. The location is superior,[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)