How to solve the "world problem"?

From the elderly who have died to the 5-year-old children, about 2,000 villagers in the village have inexplicably "suffered a stroke".

This is not because stroke has become a new epidemic. Instead, some village doctors used false diagnosis and treatment records to defraud residents of the outpatient pooling fund for basic medical insurance.

According to the official disclosure of typical cases of insurance fraud over the years, hospitals are the "hardest hit areas" of violations.

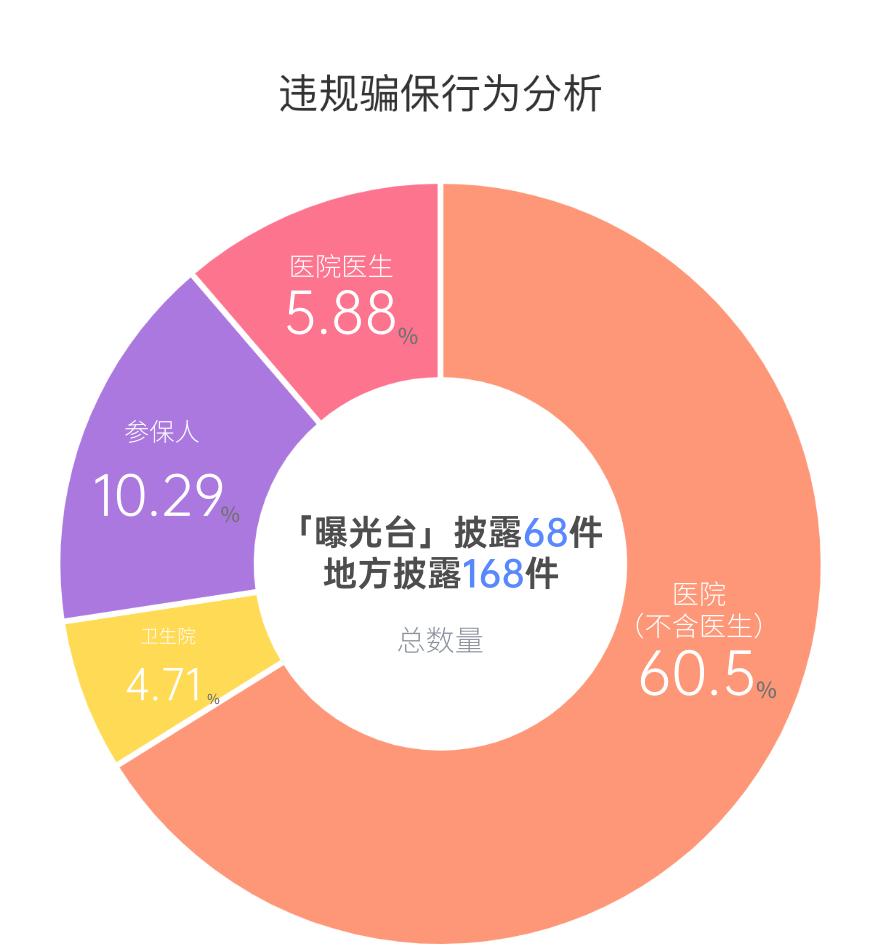

As of the end of June 2021, the "exposure desk" of the National Medical Insurance Bureau disclosed 68 typical cases and 168 local disclosures. Among them, hospital violations accounted for 66.18%, health centers 14.71%, and insured 10.29% - the data came from the research made by Wang Zhen, director of the Institute of Economics of the Chinese Academy of Social Sciences.

Hospitals and other medical institutions, as the main body of violations, have a high frequency of violations of laws and regulations, including excessive examination, excessive diagnosis, fabrication of hospitalization treatment materials, false charging, falsification of medical records, replacement and collusion of drugs, hanging beds for hospitalization, induction of hospitalization, and forged purchases.

The medical insurance fund is the "life-saving money" of the people. Since the establishment of the National Medical Insurance Bureau, it has been practicing "never letting the medical insurance fund become the new 'Tang monk meat'".

According to Jiang Chengjia, director of the Department of Fund Supervision of the National Medical Insurance Bureau, since the establishment of the National Medical Insurance Bureau, from 2018 to October 2021, a total of about 2.34 million designated medical institutions have been inspected, about 1 million have been handled, and about 50.6 billion yuan of medical insurance funds have been recovered.

In December 2021, the National Medical Insurance Bureau and the Ministry of Public Security jointly issued the "Notice on Strengthening the Investigation and Handling of Cases of Fraudulent Medical Insurance Fund Executions", a blockbuster document, which can be called "the most severe 'new policy for fraudulent insurance imprisonment'".

Under the pressure of supervision and heavy blows, what should hospitals do?

Recently, China Medical Insurance magazine and social science literature publishing house jointly released the "Blue Book of Medical Insurance Fund Supervision: Report on the Supervision and Management and Development of China's Medical Security Fund (2021)" (hereinafter referred to as the "Blue Book"), which may bring new ideas for medical insurance fund management to hospitals.

Ying Yazhen, vice president of the China Medical Insurance Research Association and vice president of the National Medical Security Research Institute of Capital Medical University, believes that the Blue Book should "arouse the society's widespread attention to the safety of medical insurance funds, help all walks of life to fully understand the supervision of medical insurance funds, create a consensus on maintaining fund security, and timely recommend innovative concepts and practical experiences in medical insurance fund supervision."

What are the common insurance scams?

Medical insurance behavior involves many parties such as medical institutions, patients and medical insurance fund regulatory departments. In the view of Geng Tao, deputy director of the Supervision and Inspection Institute of the Shanghai Municipal Medical Insurance Bureau, who has long been engaged in the supervision and inspection of medical security funds, the medical insurance system has the characteristics of "four more and one long", which is embodied in the characteristics of "many stakeholders, many links, many risk points, many insurance fraud means, and a long chain of custody.

According to Geng Tao's research, the insurance fraud behavior of medical institutions mainly involves two kinds of -

First, "falsehood is true" is the main deception method, including fake patients, fake illnesses, and fake bills. Specific acts generally include false recording of drugs and medical treatment items, forged medical documents, false purchase invoices, fictitious diagnosis and treatment services, fabricated hospitalization materials, fraudulent use of insured persons' medical insurance cards, and false reimbursement invoices.

Second, medical institutions often take advantage of the asymmetric nature of medical service information to increase medical expenses by decomposing hospitalization, decomposing prescriptions, over-diagnosis and treatment, examination, over-prescribing, repeated prescriptions, repeated charges, over-standard charges, and decomposition project charges. Such cases are often joint cases of members of the institution, with a large number of occurrences and a large amount of money.

For example, the shocking "Taihe insurance fraud case", the media exposed the doctor's falsification of patient medical records, inducing the asymptomatic or mildly ill elderly to be hospitalized, thereby illegally arbitrage of the medical insurance fund, through the comprehensive investigation of all cases in 2020 in the 4 hospitals involved, it was found that the illegal and illegal involves the payment amount of the medical insurance fund as high as 7.5942 million yuan. In Fuyang City, where Taihe County is located, the amount of insurance fraud in 7 counties (districts) of the city is as high as 45.544 million yuan.

Why do insurance fraud still occur from time to time under the high-pressure crackdown? Wang Zhen believes that the motive for violations of laws and regulations is, in the final analysis, "interests".

On the one hand, the operation and profitability of primary medical institutions and pharmacies are limited, and they are more likely to tend to take risks and take fraudulent hedging to obtain improper profits in order to maintain survival and development.

On the other hand, some private hospitals are driven by interests and have weak legal awareness, and one-sidedly pursue improper profits; in addition, medical staff are either tempted by profits or in order to make up for the lack of labor value, subjectively began to seek "medicine to support doctors" and other ways, relying on violations to increase gray income.

How to check? How to punish?

It is not easy to combat fraud and insurance fraud in the new situation. The Blue Book points out that there are three main difficulties.

The first is the difficulty of discovery. Fraud and anti-fraud are shifting from explicit to implicit; the form of insurance fraud is also undergoing an evolution process from individuals to gangs, to doctor-patient collusion and joint insurance fraud, and presents cross-regional and electronic characteristics.

For example, the "Shenyang insurance fraud case" and "Taihe insurance fraud case" exposed by the media in recent years have exposed the "three false" insurance fraud problems such as fake patients, fake diseases, and fake bills in some bad hospitals, and it is difficult to find fraud and insurance fraud from individual conditions alone.

Second, it is difficult to identify. In the field of medical insurance fund supervision, it is more difficult to deal with when there is doubt about the rationality of fund expenditure, and the medical insurance department often lacks corresponding standards for the judgment of clinical diagnosis and treatment and drug use behavior compliance.

Finally, it is difficult to cure. Medical reform is a worldwide problem, especially in the current hospital compensation mechanism, charging price and performance management and other reforms have not yet been in place, coupled with the superimposed impact of "moral damage" caused by the third-party payment of medical insurance funds, some hospitals and doctors have repeatedly prohibited the behavior of inducing patients to seek medical treatment driven by interests, and even the fraudulent behavior of doctors and patients colluding.

Since its establishment, the National Medical Insurance Bureau has deployed special governance work of medical insurance funds for three consecutive years, and has made certain achievements in the supervision of medical insurance funds by establishing a flight inspection work mechanism, implementing reward measures for reporting, increasing the exposure of insurance fraud cases, promoting the construction of the rule of law in fund supervision, deploying and promoting the "two pilots and one demonstration" work, and promoting joint supervision by departments.

The "Blue Book" shows that from 2019 to 2020, the proportion of inspections of designated medical institutions in the national medical insurance was stable at more than 99%, and the cumulative recovery of funds was as high as 33.867 billion yuan.

Among them, a total of 22.311 billion yuan was recovered in 2020, which is nearly twice that of the funds recovered in 2019.

In terms of flight inspection, in 2019, 66 flight inspection teams were dispatched successively, covering 30 provinces (autonomous regions and municipalities directly under the central government) across the country, and 1.125 billion yuan of suspected illegal funds were found. In 2020, the National Medical Security Bureau organized a total of 2 batches of 61 flight inspection teams, and a total of 540 million yuan of suspected illegal funds were found.

In addition, since the National Medical Insurance Bureau opened reporting channels for the whole society in November 2018, by the end of 2019, 11,411 fraudulent insurance reports had been received nationwide, with a completion rate of 95.40%. In 2020, a total of 2,141,600 yuan of whistleblowing rewards were issued nationwide. In the same year, the official website of the National Medical Insurance Bureau exposed a total of 5 major cases, and the local medical insurance departments took the initiative to expose a total of 42,108 cases of fraud and insurance fraud.

According to Wang Zhen's statistics, common penalties for insurance fraud include fines, cancellation of agreements, and revocation of licenses. In addition, there are relevant punishment measures related to the suspension of the medical insurance reimbursement system, the suspension of medical insurance services, the revocation of the "Medical Institution Practice License", the rectification within a time limit, the dismissal of duty, the transfer to relevant departments or judicial organs for handling, criminal detention, serious warning punishment within the party, or administrative demerit handling.

In addition, starting in 2021, some regions have seen penalties for sentences of fixed-term imprisonment.

How does the hospital check itself?

In the context of the reform of medical insurance payment methods, hospitals should pay special attention to the rational and compliant use of medical insurance funds, which is not only a regulatory need, but also an inevitable path for the high-quality development of public hospitals.

Leng Jiahua, director of the Medical Insurance Service Division of Peking University Cancer Hospital, believes that medical insurance management is entering a stage of high-quality development, value medical care will become the pursuit of goals, and medical institutions should actively participate in the formulation of medical insurance policies in the future, while paying attention to the integration and development of medical insurance performance and performance appraisal, and uniting different departments such as information, medical administration, and pharmacy to work together.

In the clinical aspect, hospital management should change the way of passive supervision in the past, take the initiative, and do a good job in medical indicators. Under the background of drg/DIP medical insurance payment method reform, hospital medical indicators can get more money from the medical insurance fund if they do well, which certainly encourages medical institutions to pay attention to medical insurance reform with motivation and initiative. But at the same time, we must also avoid the dual tendency of over-medical treatment and under-medical treatment.

The existing medical insurance supervision has entered the stage of legalization and social governance. As a clinician, Leng Jiahua also sees some urgent problems to be solved, such as the natural problem of repeated treatment for tumor patients.

"How to define whether this behavior is a breakdown of hospitalization?" It remains to be explored." Leng Jiahua suggested that we should emphasize social governance, set up an expert database and a multi-dimensional assessment model, negotiate through consultation, and arbitrate contradictions.

In terms of specific practices, the Blue Book selects six medical institutions, including designated public and non-public, comprehensive and specialized, from the perspective of hospital medical insurance management, and discusses their internal medical insurance management practices and experiences.

Zhu Jiaying, director of the Medical Insurance Price Office of Zhejiang Provincial People's Hospital, believes that it is necessary to establish a rational drug use review system, a real-time intelligent supervision system for the whole process and a SPD standardized management model, so as to strengthen drug supervision, help the supervision of medical service projects, and standardize the use and supervision of consumables.

Zhu Jiaying specifically proposed that hospitals should take "irregular medical behavior" as a breakthrough point in fund supervision. Through intelligent supervision, we focus on irregular medical behaviors such as violations of medical insurance drug indications, drug over-dosage, repeated charges, over-frequency charges, and mismatch between materials and diagnosis and treatment items.

Note: The expert views and data in this article are mainly from the "Blue Book of Medical Insurance Fund Supervision: Report on the Supervision and Management and Development of China's Medical Security Fund (2021)" and the report conference, and the views in the article only represent the views of the author (or research group) of the report.

Sources | the health community

The author | Jiansheng