At 4:00 a.m. Beijing time last week, the Fed, which had not seen any movement for more than a year, finally "wolfed", announced a 25 basis point rate hike, and the new federal funds target rate will be in the range of 0.5%-0.75%. According to the FOMC decision statement, the interest rate decision is unanimously passed, it is expected to raise interest rates three times in 2017, and there will be three interest rate hikes in 2018, and the future financial policy of the United States will enter the fast lane of interest rate hikes. As soon as the news came out, the price of gold futures fell again, the exchange rate of various currencies against the US dollar also fell to the ground, and China not only suffered against the US dollar, creating a high of 6.950 US dollars, and the Treasury bond index also fell sharply. Usually, interest rate hikes cause stock prices to fall, but this time both the Dow Jones and Nasdaq indexes hit new highs. Many analysts in the industry have written articles dissecting how to defend China's economy and defend the renminbi in the midst of a "strong dollar." More "patriotic commentators" said that the exchange target of $50,000 per person per year would be abolished. I generally take a dismissive approach to these sensational remarks, and this time will certainly not be an exception.

Before refuting these remarks, we must answer an unavoidable question, how many more rates will the Fed raise? Or how many more rates can the Fed raise? If these can be answered, the above sensational arguments will be self-defeating, and everyone's worries will be eliminated.

Or according to the author's style to first talk about the answer: based on the current us real economic situation, 6 interest rate hikes can not afford it, so we should treat the future interest rate hike expectations with a calm psychology.

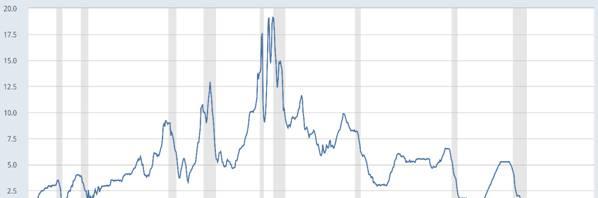

Let's first look at the direction of some of the major interest rate indicators in the United States. Figure 1 is a long-term chart of the US federal funds rate. Figure 2 shows the interest rates on US 5-year, 10-year and 30-year Treasuries after 2008. The federal funds rate has been in a downward spiral since the 1980s, and has been hovering slightly above the zero line since the 2008 financial crisis.

Figure 1 United States federal funds rate

Figure 2 U.S. Treasury rates for 5-, 10-, and 30-year government bonds

When considering the impact of interest rates, especially long-term interest rates, on the economy and capital prices, more important than the federal funds rate is the interest rate on treasury bonds, especially the interest rate on 10-year Treasuries (blue), which we have mentioned in the previous serial and represents the long-term interest rate. The trend of interest rates on U.S. Treasuries is closely positively correlated with the federal funds rate, which has been hovering at a historic low since the 2008 economic crisis. Due to Trump's proposal to issue a large number of long-term treasury bonds to invest in national utilities during the Trump campaign, after Trump was elected president, the interest rate of treasury bonds has soared sharply (the price of treasury bonds has fallen). Some analysts also said that the main reason for the rise in US interest rates this time is the change in supply and demand caused by the dumping of US Treasury bonds by China and Saudi Arabia.

Table 1 Interest rates on various types of US bonds

U.S. Treasury Bonds

U.S. corporate bonds

U.S. junk debt

5 years

2.10%

3 years ETF

2%

5-6 years ETF

5-6%

10-year period

2.60%

7 years ETF

2.70%

30 years

3.20%

15-25 years ETF

4-5%

Table 1 compares the interest rates on U.S. Treasuries, corporate bonds, and junk bonds (the corporate and junk rates are replaced by the rates of ETFs). The median interest rate for good U.S. corporate bonds is nearly the same as for 10-year Treasuries, while junk bonds have more than twice the interest rate on Treasuries of the same maturity. Now, if Trump's New Deal requires the issuance of a large number of 50-year Treasuries, the interest rate should be higher than the interest rate of the 30-year Treasury bond, and reasonably should be around 4-5%, which will inevitably push up the interest rate of long-term corporate bonds and junk bonds. The probability of the 50-year treasury bond being dumped should be much lower than that of the junk debt, in this case, the interest rate of the junk debt will rise by 2 percentage points, and if the interest rate is raised twice, the interest rate should enter the double digits when it is full. We have repeatedly stressed in previous serials that the main body of U.S. garbage debt is energy developers who are mainly shale gas development, many of them are on the verge of production, and this time because Trump threatened to ease the environmental protection restrictions of shale gas development, the interest rate of garbage debt did not rise sharply this time and escaped the disaster. Double-digit interest rates are undoubtedly a fatal blow to shale gas developers. We have repeatedly stressed in previous serials that the life and death of shale gas developers in the United States, like the price of real estate in China, is an insoluble hole in the US economy.

Another point is also quite important, interest rate hikes will directly lead to the appreciation of the dollar, a strong dollar and Trump's "economic patriotism" contrary to the opposite, not only is not conducive to the export of American enterprises, but also for the return of American enterprises will also become a great obstacle, this should be known to everyone, here will not be repeated. Similarly, rising interest rates will also create an economic burden on governments and households, and it is self-evident what an increase in interest rates will mean for a nation that likes to spend money in the future and with other people's money in advance. In the past two years, the US economy has driven consumption by durable consumer goods such as homes and automobiles, and the driving force behind it is also low interest rates and loose monetary policy. The long-term interest rate, or around 3% of the interest rate on 10-year Treasuries, could be a ceiling.

Combining the above points, as long as people with a little economic knowledge pat their heads, they will also know that the 6 interest rate hikes in the next two years are for the media and for those "leeks" who are willing to be the receivers of the United States. If Trump and Yellen are not big fools, the probability of one rate hike in 2017 may be higher than 50%, the probability of two rate hikes should be less than 20%, and there is no need to guess whether there will be a rate hike in the future. If I let the author gamble, I will definitely bet a small amount of money on the restart of 2018. Everyone may be staring at the United States ignoring Europe, 2017 is a general election year in Europe, and now Europe is already a "black swan lake", the white swan is far less than the black swan, and the farce similar to Brexit may be once a month. Seeing that if you still believe in the Fed's "flickering" here, the author suggests that there is no need to read my article in the future.

After the 2008 financial crisis, especially after the restart of interest rate hikes, the most important part of US financial policy is not the interest rate hike itself but the expectation of interest rate hikes, which guide the stock and bond markets and even the entire economy through interest rate hikes, which economics calls "expectation". For a simple example, it is easy to understand, when we buy stocks, the most important thing is whether the stock will rise rather than the stock price itself, and when the market maker ships high, it is also the use of the greedy psychology of retail investors to create expectations that they can eventually retreat, whether it is news or technical, the success or failure of a bookmaker ultimately depends on his "expected" creative skills. For the Fed to use "expectations" to easily manipulate the psychology of the receiver, and even kidnapped the financial policies of other countries, including China, in the case of almost no improvement in the real economy, a volume of leniency policy and a interest rate hike expectation can play with ease for eight years, the author's ability to the Fed is also five-body investment. I'm not a conspiracy theorist, but I've always felt the "invisible hand" of manipulating the market.

Zhao Tong

2016-12-20