Figureworm Creative /Courtesy photo Peng Chunxia/Cartography

Securities Times reporter Liu Canbang

With the end of the disclosure of the third quarterly report, the pattern of upstream and downstream differentiation of the photovoltaic industry has gradually emerged.

At the beginning of the year, the industry's view of "silicon is king" has been further verified, due to changes in supply and demand and price factors, silicon is the best link in the main photovoltaic industry chain this year; the ability of silicon wafers to conduct downward cost pressure is strong, but even if the two major silicon wafer leaders, the operating rate in the third quarter has been lowered; the concentration of battery links is relatively low, facing the squeeze of upstream and downstream, which is the hardest hit area of performance losses in the third quarter; module manufacturers are seriously differentiated due to different industrial structures and capital structures.

It is still difficult for the industry to judge when this round of industrial chain price increases will come to an end, but the interviewees pay special attention to the upcoming changes in the industrial pattern. This change is mainly concentrated in the silicon wafer link, due to the influx of new entrants, the expansion of wafer production capacity next year will be very significant, in the words of one interviewee, the silicon wafer rookie has invested so much money to build a production line, it is impossible not to grab silicon materials, do not start, otherwise, the depreciation scale of the new production line will be very large. At that time, the relationship between the silicon wafer and the upstream and downstream may be reinterpreted.

For the recent situation, in interviews with people in different industry links, they all mentioned the view that the fourth quarter is the peak season for photovoltaic installations. A component manufacturer reported to the Securities Times reporter that the component inventory of the head manufacturer is currently at a high level, mainly to prepare for the shipment in the fourth quarter, because it is difficult to meet the shipment requirements by relying on the production capacity in the fourth quarter alone. Since October, the price of components has exceeded 2 yuan / W, and the industry is paying attention to whether the terminal demand can be accepted, but also paying great attention to whether the new energy electricity price can follow the floating.

Silicon supply is tight

It will continue until next year

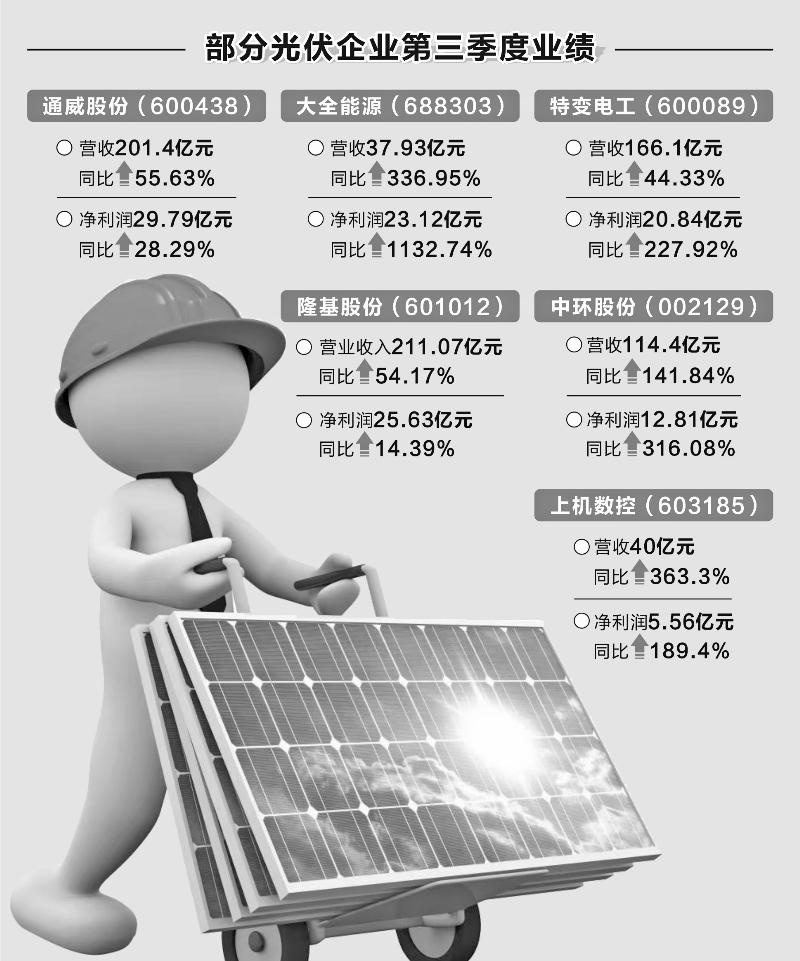

As far as this year's situation is concerned, silicon materials are the most profitable link in the main photovoltaic industry chain, and silicon manufacturers are the biggest beneficiaries. Tongwei Co., Ltd. (600438) achieved revenue of 20.14 billion yuan and net profit of 2.979 billion yuan in the third quarter, with a year-on-year growth rate of 55.63% and 28.29%, respectively, and achieved revenue of 46.7 billion yuan and net profit of 5.945 billion yuan in the first three quarters, with a year-on-year growth rate of 47.42% and 78.38%, respectively.

Tongwei shares mentioned that the increase in the company's operating income is mainly due to the expansion of the scale of operation and the increase in product prices. According to the reporter's understanding, Tongwei shares' existing annual silicon production capacity of 80,000 tons, and there is a certain degree of overproduction, capacity utilization rate to maintain a high level; at the end of this year, the company will have 100,000 tons of new production capacity put into production, respectively, Sichuan Leshan Phase II 50,000 tons and Yunnan Baoshan Phase I 50,000 tons.

Daqo Energy (688303) landed on the Science and Technology Innovation Board in July this year, is also one of the mainstream silicon suppliers, the company achieved revenue of 3.793 billion yuan and net profit of 2.312 billion yuan in the third quarter, with a year-on-year growth rate of 336.95% and 1132.74% respectively; the first three quarters of revenue of 8.3 billion yuan, net profit of 4.473 billion yuan, the year-on-year growth rate of 177.16% and 799.73% respectively.

Daqo Energy said that in the first three quarters of this year, the overall photovoltaic market continued to grow, the downstream demand was strong, the polycrystalline silicon material market was tight, the unit price of polysilicon sales rose sharply, and the sales volume increased, among them, the tight supply and demand of silicon materials in the third quarter continued to exist, and the price increased compared with the previous quarter. In the context of the rising volume and price of polysilicon, the company's gross profit on polysilicon sales has also increased significantly.

Data show that in the first three quarters, Daqo Energy achieved polysilicon production of 63,000 tons and sales of 63,700 tons, an increase of 11.89% and 23.42% respectively compared with the same period last year. On the whole, the company's single-quarter output in the first three quarters has steadily increased, and single-quarter sales have remained at about 21,000 tons, basically achieving full production and full sales. In addition, the average selling price in the first three quarters was 129,700 yuan / ton, an increase of 125.05% year-on-year, but the unit cost of silicon materials remained basically unchanged, with an average of 42,600 yuan / ton in the first three quarters.

Like Tongwei shares, Daqo Energy also had overproduction in the first three quarters, and will invest in new production capacity at the end of the year. According to Daqo Energy's statement, the company will maintain full production, the annual output is expected to be 83,000 to 85,000 tons; the company's phase III B annual output of 35,000 tons of polysilicon expansion project is under construction, is expected to be completed and put into operation by the end of the year, and reach production before the end of March 2022.

In the third quarter, TBEA (600089) achieved revenue of 16.61 billion yuan and net profit of 2.084 billion yuan, with a year-on-year growth rate of 44.33% and 227.92%, respectively; in the first three quarters, revenue was 39.168 billion yuan and net profit was 5.191 billion yuan, with a year-on-year growth rate of 32.65% and 233.67%, respectively. The company said that one of the reasons for the increase in performance is the increase in polysilicon prices and sales.

"Silicon material is very good to trade, gross profit is also very high, and it is cash delivery, one hand in full and one hand in stock, no worry about sales at all." A person from a silicon factory said to reporters that once again verified the conclusion that the silicon material link has the best income. According to PV InfoLink data, the high point of silicon prices this week is 270,000 yuan / ton, and even the average price is as high as 267,000 yuan / ton.

For the next stage of the trend of silicon prices, the industry believes that it is difficult to judge, "the price fluctuations are very large, half a year ago no one would have thought that the price of silicon materials could rise to more than 250,000 yuan / ton, even in September, we also feel that 210,000 yuan / ton has reached the top, but now to 270,000 yuan / ton, still relatively strong." ”

So, is it possible for the price of silicon to plunge sharply? A person from a head silicon factory believes that this situation cannot be seen in the short term. As far as the fourth quarter is concerned, photovoltaics may appear rush to install, in the case of silicon shortage and no new release capacity at the end of the year, silicon prices are supported; next year, although silicon materials also expand, but silicon wafer capacity expansion is faster, the supply and demand pattern between the two links will change, "according to the silicon wafer production capacity calculation of silicon material is still in short supply, supply and demand relationship will become the support of silicon prices." ”

Silicon wafers and batteries

Squeezed to varying degrees

Strictly speaking, silicon wafers are in the upstream position of the main photovoltaic industry chain, in the face of silicon price increases, silicon wafer manufacturers have a very strong ability to conduct costs downstream, but from the reporter's observation, in the first three quarters, several major silicon wafer suppliers were also squeezed to varying degrees.

Taking LONGi (601012) as an example, the company achieved operating income of 21.107 billion yuan and net profit of 2.563 billion yuan in the third quarter, with a year-on-year growth rate of 54.17% and 14.39% respectively; in terms of single-quarter data in the first three quarters, the company's net profit was 2.502 billion yuan, 2.491 billion yuan and 2.563 billion yuan, respectively, which remained stable quarter-on-quarter, but the growth rate change in each quarter and the same period of the previous year was significantly weakened.

The reporter learned from LONGi shares that due to the increase in the price of various raw materials such as silicon materials, the company's profits have been eroded to a certain extent, and the operating rate of some production lines has also been affected by the rise in raw materials. The reporter learned that LONGi shares reduced the operating rate of silicon wafers in the third quarter, and in the first three quarters, the cumulative shipments of silicon wafers were also less than the same period last year.

Another silicon wafer leader, Zhonghuan Co., Ltd. (002129), achieved revenue of 11.44 billion yuan and net profit of 1.281 billion yuan in the third quarter, with a year-on-year growth rate of 141.84% and 316.08% respectively; in the first three quarters, revenue was 29.09 billion yuan and net profit was 2.76 billion yuan, with a year-on-year growth rate of 117.46% and 226.29%, respectively. As one of the silicon bipoly, Zhonghuan shares have not escaped the decline in operating rate, the reporter learned from the company, in the third quarter, the company's silicon wafer operating rate was about 70%, and now it has gradually risen to 85% to 90%.

Silicon wafer rookie computer numerical control (603185) achieved revenue of 4 billion yuan and net profit of 556 million yuan in the third quarter, with a year-on-year growth rate of 363.3% and 189.4%, respectively; the first three quarters of revenue of 7.586 billion yuan and net profit of 1.405 billion yuan, a year-on-year growth rate of 289.71% and 310.28%, respectively. From the performance growth rate is still very eye-catching, the company mentioned that the expansion of the monocrystalline silicon business has increased revenue.

However, looking further, the sharp increase in the price of silicon materials has adversely affected the gross profit margin of CNC on the machine. The gross profit margin of the company in the first three quarters was 24.7%, down 6.25 percentage points from the gross profit margin of 30.95% in the first half of the year; of which the gross profit margin in the third quarter was only 19.1%, a sharp decline from the previous quarter.

Because the battery is in the position of the main photovoltaic industry chain, the squeeze is more obvious. As a silicon material, battery double leader Ofway shares is an example, although the company's silicon business volume and price rise together, but from the overall net profit growth rate, significantly weaker than the single business of Daquan Energy. Tongwei shares told the Securities Times reporter that one of the reasons for the difference between the company's net profit growth rate and peers is that the base is different, but the person also pointed out that the entire battery link this year is more difficult, and the cost transmission is not as good as the upstream.

Another situation that the person talked about is that the battery link belongs to the pattern of squeezing at both ends, and the battery production capacity is not only relatively larger, but also the capacity distribution is more dispersed, not as high as the concentration of silicon materials and silicon wafers, which leads to the current conditions, the premium ability of the battery link is relatively weak. The reporter learned that the industry-wide battery operating rate reached a low point in the second quarter and improved in the third quarter.

Aixu shares (600732) is also an example, in the third quarter, the company's operating income of 4.33 billion yuan, an increase of 69.05% year-on-year, but the net profit was a loss of 22.07 million yuan; in the first three quarters, the company's operating income was 11.2 billion yuan, an increase of 78.99% year-on-year, and the net profit loss was 45.825 million yuan. The company said that the increase in production and the expansion of sales scale increased sales revenue, but the price of major raw materials rose more than the increase in sales prices, resulting in a decline in profits.

As for the component link, the difference in performance in the first three quarters is even greater. LONGi shares, which are the double leaders of silicon wafers and components, the expansion of revenue in the first three quarters was due to the growth of module sales, but the profitability of the module business was suppressed by high costs. Among the other component leaders, in the first three quarters, trina solar (688599) net profit of 1.16 billion yuan, an increase of 39.05% year-on-year; JA Technology (002459) net profit of 1.31 billion yuan, an increase of 1.62% year-on-year; Oriental Risheng (300118) net profit of 354 million yuan, but after deducting non-profit loss of 230 million yuan.

"This year's component links are not very ideal, but compared with the first half of the year, the efficiency of components in the third quarter is improving, especially in October, the price of components jumped from 1.8 yuan / W to more than 2 yuan / W, the increase is relatively large." A component manufacturer told reporters.

Another component manufacturer also said that from the perspective of module operating rate, the differentiation between first-line manufacturers and second- and third-tier manufacturers is very serious; and the component inventory of the company is at a high level, mainly to complete the fourth quarter of shipment preparations, because the single-quarter production capacity can not meet the shipment requirements.

![What lolitas are in the game? Seemingly weak but actually output explosion, popularity strength double full[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)