On 23 September, PwC released its 2021 Semi-Annual Review and Outlook for China's Banking Industry. Looking back at the first half of the year, the overall performance of listed banks has improved and the asset quality has shown a stable and good trend, but the core Tier 1 capital adequacy ratio has declined and the difficulty of capital replenishment has increased. For hot issues such as real estate financial loans, which have attracted much attention in recent days, PwC China's financial industry partners also made an analysis and interpretation in an interview with Aoyi News reporter.

How big is the impact of the decline in the growth rate of real estate loans and the rise in non-performing loans?

Recently, regulators have frequently spoken out, proposing to adhere to the prudent regulatory standards for real estate development loans and personal mortgage loans, and clearly indicating that they will curb the illegal flow of "operating loans" into the real estate field and severely punish violations of laws and regulations. Affected by policies such as real estate loan concentration management, the growth rate of real estate enterprise loans has decreased significantly, from 11% in the first half of 2020 to 5% in the first half of 2021.

Regarding the slowdown in real estate loans in the banking industry, Xie Ying, a partner in PwC's China financial industry, believes that this actually reflects a "deleveraging" purpose. Under the current macroeconomic regulation and control, the existence of the "three red lines" itself will have an impact on the growth rate of real estate loans, showing a trend of compressing real estate loans, and at the same time making the real estate industry itself also have the impetus to achieve economic growth and structural transformation. ”

At the end of June 2021, the rapid growth momentum of non-performing balances of listed banks was suppressed, with the overall non-performing ratio of 57 banks falling from 1.51% at the end of 2020 to 1.44%, the overdue rate from 1.49% to 1.45%, and the concern loan ratio from 2.07% to 1.88%.

However, it can be seen that with the tightening of real estate regulation and control of macro policy, the overall non-performing rate of real estate loans of listed bank companies has risen significantly. In terms of market performance, on the first trading day after the holiday yesterday, the bank stock sector fell collectively, according to the Choice platform Shenwan Bank Index, the overall decline of the A-share bank index in the past 5 trading days reached 6.47%. Today's close, the bank stock sector picked up. Will real estate loans have a big impact on the banking industry?

Wang Wei, a partner in PwC China's financial industry, pointed out that in the first half of this year, the non-performing loan ratio of real estate loans continued to rise. The regulatory level and the national macro level have successively introduced some policies, and for listed banks, there is a lot of room for operation on how to do a good job in consolidating the quality of real estate customers.

Xie Ying said in an interview, "The regulator has done the relevant risk assessment, has enough confidence and experience to properly deal with the problems of the real estate industry, avoid the problems of individual housing enterprises from conveying risks to the entire industry or upstream and downstream enterprises, try to restore market confidence, and reduce the negative impact of the real estate industry on the financial market." At the same time, Chinese regulators are also guiding the market reasonably to avoid triggering sharp fluctuations in the bond market. ”

Asset quality is good Wealth management promotes revenue

According to PwC's analysis of 57 A-share and/or H-share listed banks, the performance of listed banks improved in the first half of the year, on the one hand, due to the stabilization of asset quality, the provision for loan impairment losses decreased; on the other hand, banks actively promoted business transformation and focused on intermediate businesses such as wealth management, and the growth rate of non-interest income was higher than that of net interest income.

In the first half of 2021, the overall net profit of 57 listed banks increased by 12.21% year-on-year to 1.02 trillion yuan, and the net profit of 52 banks increased year-on-year. The impairment loss on credit assets of listed banks decreased by 5.95%, resulting in a net profit increase of more than pre-provision profit.

At the same time, the average return on total assets (ROA) of large commercial banks and joint-stock commercial banks increased slightly, while urban and rural commercial banks were basically flat. The net interest margin and net interest margin of large commercial banks, joint-stock commercial banks and urban and rural commercial banks generally show a narrowing trend. The steady decline in the yield of loans of listed banks is mainly due to further responding to the call to support the real economy and reduce the financing costs of enterprises; at the same time, the loan market quotation rate (LPR) continues to deepen the reform potential and guide interest rates to decline.

Xie Ying, PwC China Financial Industry Partner, said: "In the first half of 2021, China's economy continued to recover steadily, the performance of listed banks showed significant improvements, and the ability of operation management and risk resilience continued to improve. Fee and commission income grew faster than net interest income. At the same time, listed banks have increased their support for key areas such as inclusive finance, green finance, strategic emerging industries, high-end manufacturing, and rural revitalization, and loans and total assets have grown rapidly. ”

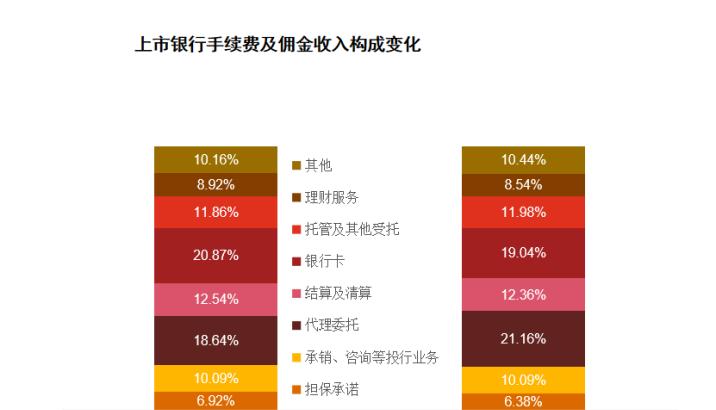

It is worth noting that with the transformation of business, the wealth management business of listed banks has increased its contribution to intermediate business, and the proportion of agency entrustment fee income (agency insurance, agency fund, agency asset management trust, etc.) has increased, surpassing bank cards as the most important source of income.

The downward trend of the core Tier 1 capital adequacy ratio is obviously needed to accelerate the transformation

In the first half of the year, listed banks continued to increase the disposal of non-performing assets, at the same time, as of the end of June 2021, the core Tier 1 capital adequacy ratio of listed banks generally declined, and the core Tier 1 capital adequacy ratio of individual joint-stock commercial banks and urban and rural commercial banks has approached regulatory requirements and needs to be supplemented accordingly.

PwC pointed out in the report that the main reason is that the growth rate of risk-weighted assets exceeds the growth rate of core Tier 1 capital, causing losses to capital, resulting in a decline in core Tier 1 capital.

In the first half of 2021, listed banks raised a total of RMB490.38 billion through perpetual bonds, non-public issuances, convertible bonds and secondary capital bonds, a decrease of RMB496.3 billion or 50% from the first half of 2020, making it more difficult for the capital market to finance.

With the implementation of the new Basel III Standards Law from January 1, 2023, and a series of new capital regulations issued by the Banking and Insurance Regulatory Commission, the capital of China's commercial banks will continue to bear greater pressure in the medium and long term, so commercial banks need to accelerate business transformation and use capital more efficiently and economically.

Aoyi news reporter Mai Miaodian