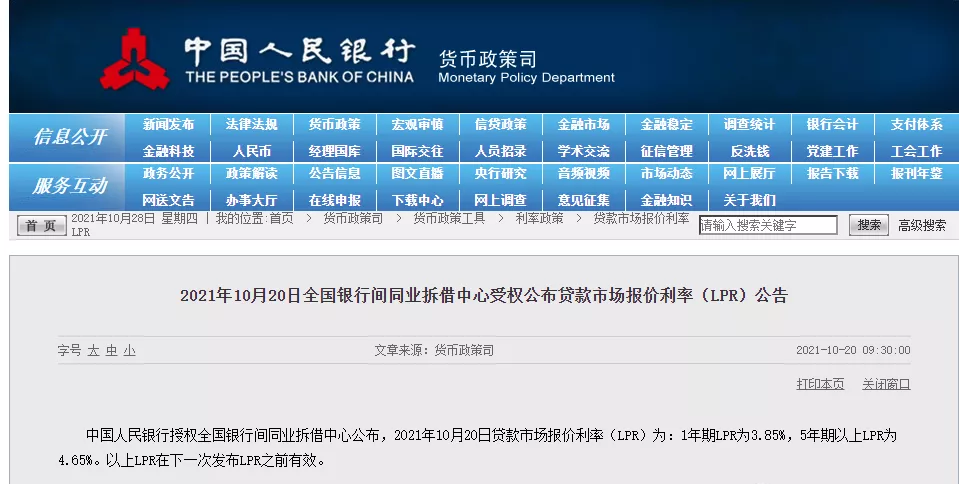

October 20, 2021. The National Interbank Lending Centre is authorized to publish the Loan Market Quotation Rate (LPR) Announcement.

Chinese Min min bank authorized the National Interbank Lending Center to announce that the loan market quotation rate (LPR) on October 20, 2021 is: 3.85% for 1-year LPR and 4.65% for 5-year LPR. The above LPR is valid until the next LPR is released.

The LPR for October 2021 has not changed since the previous month, and there has been no change since April 2020.

According to the voting results of the survey in the August article, many buyers in Wuhan have interest rates above 5.78%.

The interest rate of the first home in Wuhan generally rose from 5.68% to 5.73%-5.78%

Reference to loan interest rates of major banks in Wuhan:

Data source: Shell Research Institute Finally, please refer to the actual bank

In early June 2021, it rose from 5.68% to 5.73%-5.78% (5-year + 108 to 113 basis points), 5.98% for two-suite (5-year LPR + 128 to 133 basis points).

After a small survey, the interest rate of the first suite in Wuhan is generally 5.78%, the second suite is generally 5.98%, and the commercial office is generally 6.37%.

After a continuous decline in LPR to 4.65%.

It has not changed for more than 1 year

Chinese Min Bank authorized the National Interbank Lending Center to announce that the loan market quotation rate (LPR) on April 20, 2020 was: 3.85% for the 1-year LPR, down 20 basis points from the previous month; and 4.65% for the 5-year LPR, down 10 basis points (i.e. 0.1%) from March 2020.

Since then, the interest rate from May 2020 to September 2021 has been the same as in April 2020 and has not been further reduced.

On November 20, 2019, the central bank announced that the latest LPR (mortgage benchmark interest rate) with a maturity of more than 5 years will be reduced to 4.80%, on February 20, 2020, it was the second reduction in the LPR since the implementation of the LPR calculation method, and on April 20, 2020, it was the third reduction in the LPR since the implementation of the LPR calculation method (this reduction is larger than the previous two), and the total has been lowered three times.

The "Wuhan Asong" self-made LPR change table is as follows:

The cut until April 2020 is February 20, 2020, and the Loan Market Quoted Rate (LPR) is: 4.05% for the 1-year LPR, down 10 basis points from the previous month; and 4.75% for 5-year or more LPR, down 5 basis points from the previous month. Recently, however, LPR has been very stable and has not been adjusted.

The current LPR of 4.65% is also the lowest since China had an interest rate policy.

After adjusting to the LPR policy, it is more conducive to the targeted regulation of real estate. That is, when the LPR falls, by increasing the number of floating basis points, the actual execution rate of the mortgage remains relatively stable.

Mortgage interest rates in key cities across the country have also been raised:

Interest rate up 0.1% 1 million loan repayment 57 yuan more per month!

According to the loan of 1 million, 30 years, equal principal and interest calculation, if the interest rate is 5.68%, the monthly payment is 5791 yuan; if the interest rate rises to 5.78%, the monthly payment is 5854 yuan, which is equivalent to 57 yuan more per month.

What is LPR?

1. What is LPR?

The loan base rate, also known as the Loan Prime Rate (LPR), is the loan interest rate that commercial banks implement on their best customers, and other loan interest rates can be generated on this basis. The centralized quotation and release mechanism of the loan base interest rate is based on the quotation bank's independent quotation of the basic interest rate of the Bank's loan, and the publisher is designated to calculate the quotation arithmetically, form the average interest rate of the loan base interest rate of the quotation bank and announce it to the public.

2. After the implementation of the new regulations, the loan interest rate = the LPR at that time (which may change at any time every month) + the number of floating basis points (invariant after the loan is signed). Suppose, when you lend at 4.65% LPR and then rise by 103 basis points (i.e. 1.03%), then the interest rate at the time of your lending is 5.68%. After you lend a year later, you can calculate the interest rate for the next year based on the latest LPR. For example, when you sign the LPR 4.65% + up 100 basis points, if the LPR becomes 4.6% next year, your interest rate for the next year is LPR 4.6% + up 100 basis points, and the floating basis point will accompany your mortgage for decades without change.

3, but now the basis point of the new loan has changed, from 103 basis points to 108 basis points or 113 basis points, the interest rate of the buyer when signing the contract is increased, and the floating basis point will be accompanied by the entire decades of mortgage. If a recent lender rises by 108 basis points, the interest rate calculation formula for new loans will be as follows: interest rate = LPR4.65% + 108 basis points (i.e. 1.08%) = 5.73%.