Last year, I read "Value" by Zhang Lei of Hillhouse Capital, which introduced in detail the origins and investment philosophy of Hillhouse Capital. Some of the contents of this book were recently interpreted at an internal learning seminar, which is very meaningful. Here, three investment masters of the three eras are selected to make a simple sorting out of the changes in value investment thinking.

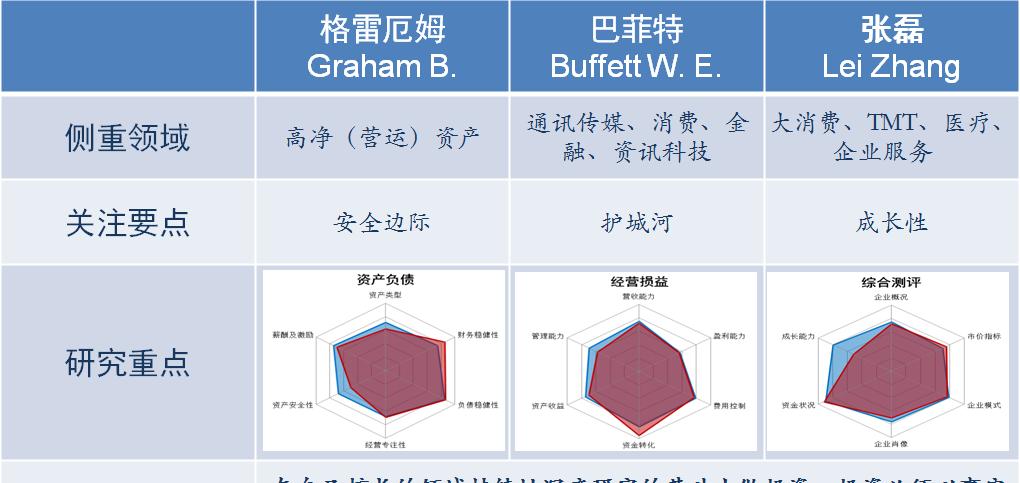

When it comes to value investing, the first thing that comes to mind must be Warren Buffett Buffer W.E., a household name. The representative figure before Buffett was Benjamin Graham B., the father of securities analysis, who was Buffett's teacher. To pick a representative figure in China, the most suitable one is Zhang Lei, who in recent years has bought shares that Hillhouse Capital has led often become sought after by the capital market.

The three of them are in three eras and share the same philosophy of value investing. However, the market environment in different periods is very different, and the investment philosophy of the three masters is constantly changing with the development of the times. To go into detail about their value investing ideas, everyone can write a thick book. Here, in a small space and in plain language, I will briefly talk about the differences and changes in their investment philosophy. Today, the main introduction is Graham.

Graham: Early-stage value investing with the margin of safety at its core

As the originator of value investing, Graham created the theoretical framework of modern securities analysis and achieved great success in practice. After the stock market crash in the 1930s, he participated in the formulation of many securities laws and regulations in the United States, and made great contributions to the formulation of securities market trading rules and financial regulatory systems.

Before Graham, capital market investment mainly referred to bond investment, while stock investment was often regarded as speculation, and stock prices were often divorced from the operating conditions of the enterprise. In such a market environment, many stocks are priced much higher than the true value of the company, and many stock prices are significantly lower than the true value of the company.

Graham found that by analyzing the company's financial information, it was possible to calculate the net (operating) assets of the company represented by each stock, which is the value of the stock. By calculating one by one, looking for companies whose stock prices are below the value, buying and holding, waiting for some time in the future when the market finds the value of the company, the stock price will gradually rise to a reasonable level.

Graham's investment strategy has been called the earliest value investing and was a resounding success after the crash in the 1930s. Affected by the stock market crash, the market sentiment is very low, and many stock prices have fallen significantly below the value of the company, and it is like picking up money to get into the bottom. The bottom can not be fried, otherwise there is usually a situation where the bottom is copied in the middle of the mountainside. This requires a detailed fundamental analysis of whether it is worth buying the company's stock at the market price and whether it has investment value.

In fact, before the economic depression and stock market crash in the 1930s, Graham had gradually explored the formation of a value investment system, and there were some investment success stories. However, after the stock market crash in the 1930s, this strategy worked more effectively and gradually gained market recognition, making the market realize that stocks are not speculative, but have logical and rigorous investment value. Under the influence of Graham, the modern securities analysis industry gradually developed, which is what today's narrow brokerage research institute does.

In Graham's value investment analysis system, the two most important concepts are net operating assets and margin of safety. To calculate the value of a company, you cannot simply use the assets on the balance sheet, nor can you directly use the owner's equity, but to calculate the assets in the net assets that are more liquid and easy to realize. For assets that are not easy to realize, such as decades of dusty broken machinery and equipment, old office furniture, etc., their book value should be excluded. The value per share is obtained by dividing the net operating assets derived from this calculation by the number of shares in the company. When the stock price is below the value per share, there is a margin of safety and investment value. The greater the margin of safety, the greater the expected return on the investment and the smaller the risk.

In the Graham era, there were many investment opportunities with a margin of safety, and it was only necessary to calculate and search for them in detail on a company-by-company basis. There is no need to pick an industry, and companies in any industry can look for investment opportunities through this system. Doing this kind of financial analysis and calculation is a manual task, similar to looking for a cigarette butt that can still be smoked in a pile of smoked butts, which is commonly known as "cigarette butt investment". This investment method is similar to the asset-liability part of Xuezhi's "three six" analysis system.

Later, with the development of the capital market and the gradual rise of stock prices, there were fewer and fewer investment targets with a margin of safety. By the 1970s, it was essentially difficult to find stocks below the net operating asset price, resulting in a smaller and smaller Graham-style value investing.

In order to adapt to market changes, value investing thinking began to change, and corrections were made to Graham's investment system. There are two main directions: one is to expand the core scope of value investment from the margin of safety to the moat represented by Buffett; the other is walter Schloss, strictly following the Graham investment system, and the correction is to gradually reduce the margin of safety standard.

In the early days, the margin of safety was set at a stock price less than 2/3 of the company's value, and such stocks were bought and sold after the stock price rose above the company's value. Later, Schloss gradually lowered the margin of safety standard, and stocks that were higher than 2/3 of the company's value were also included in the candidate. After the 1970s, companies with stock prices higher than the value of net operating assets were selected. Since then, the standard has been further lowered, and in the 1990s, companies with stock prices within 2 times the value of net operating assets have been selected. Later, companies that were less than 2 times the value of net operating assets were hard to find, so the Schloss father and son closed their partnership in 2002, marking the purest Graham-style investment in history.

Even so, today's margin of safety analysis methods and ideas are still applicable and remain an indispensable and important part of the value investment system.

Image source: Learning Wisdom Economy

(The views and judgments presented in this article are only those issued on the date of analysis, and the authors seek but do not guarantee the accuracy and completeness of the conclusions, and may issue reports at different times that are inconsistent with the views expressed herein.) The information and opinions expressed herein do not constitute investment advice to any person and are not responsible for any investment profit or loss of any person. )

![O'Neal forwarded the Lakers' three-era lineup photo: Nothing more than three Can the third time work?[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)