What happened when gold suddenly soared?

The start of the week was off to a good start for the gold market.

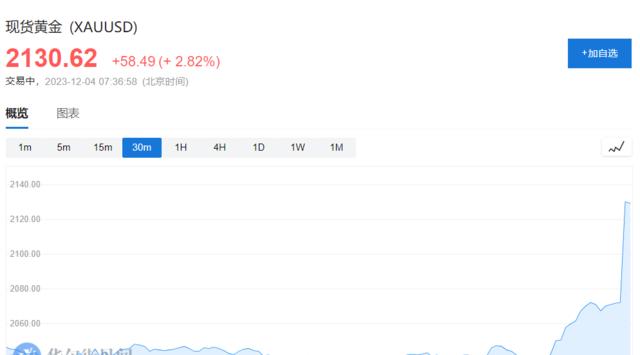

On Monday, December 4, in early Asian trading, spot gold soared by $70 intraday, approaching the $2,150 per ounce mark, up more than 3% during the day, refreshing the all-time high.

The time was a little longer, and gold consolidated for three years, and this was the third attempt in three years to break through $2,100 per ounce, and finally broke through. It has now retreated slightly to $2,090 an ounce.

Wall Street institutions such as UBS expect that the Fed's interest rate cut and the sharp fall in real interest rates will make gold possible to hit new highs in 2024 and 2025.

Strong buying of financial products related to bullish gold, whether futures or gold-backed ETFs. Over the past week, open interest has continued to increase between $2,000 and $2,500, driven by bullish sentiment.

Zerohedge, a financial blog, commented: This means that the Fed faces a new "old" problem: a mass exodus from fiat currencies and a shift to safe hard currencies, such as gold.

If the Fed does cut interest rates as soon as March next year and then proceed with more quantitative easing, which will inevitably monetize the soaring US budget deficit and explosive interest payments, then all assets will hit record highs, including gold, stocks, oil.

In addition, geopolitical concerns have recently boosted investors' safe-haven appetite for gold, with uncertainty continuing to support gold prices despite the risk of a conflict in the Middle East seemingly being contained.

Is the market betting on interest rate cuts and ignoring Powell?

A series of recent economic data releases have been weaker than analysts expected, and inflationary pressures continue to ease, cementing market expectations that the Federal Reserve has ended its rate hike cycle and will start cutting interest rates next year.

Senior Fed officials have repeatedly poured cold water on this expectation. Recently, Fed Chairman Jerome Powell's hawkish speech continued this rhetoric, trying to suppress interest rate cut expectations again.

However, the market doesn't seem to be buying it – the two-year Treasury yield plunged more than 10 basis points to a five-month low after Powell's speech, and the 10-year Treasury yield plunged to 4.21%, a three-month low.

In fact, after the bond market reached a peak of selling on October 19, Wall Street's view of interest rates changed dramatically. Over the past five weeks, Wall Street has been "working against the Fed", buying Treasury bonds in defiance of warnings from Fed executives such as Powell, leading to a sharp drop in yields.

Ben Emons, head of fixed income at wealth manager NewEdge Wealth, sees economic conditions and geopolitical backdrop as additional positive catalysts for the gold market.

"There is uncertainty about next year. There are general elections. We don't know what to expect. [The U.S. economy] may or may not fall into a recession," Emons said, "and at the same time, gold rises when there is this risk-on sentiment in the market, which is when real interest rates and interest rates fall." This provides a very good impetus for gold's rally. ”

"[This happens] tends to happen when the market is pricing in a major easing cycle," Emons said, "and at the moment, it's going on in a modest way, making the seasonality of gold a spotlight." ”

Emons expects gold's rally to continue into next year.

UBS expects the Fed to cut rates in the first quarter of 2024, and if there is a pause in December, this will continue to confirm that the Fed is inclined to cut rates around six months after the last increase.

Looking at gold's performance after the Fed's previous rate hike cycles, UBS found that gold tends to fall by 2% or so in the last three months or so after the end of previous rate hike cycles, but rises 7% over the next six months.

Hong Hao, chief economist of Sirui Group, is also optimistic about gold recently, believing that it will continue to hit new highs in the next year or two. He said:

Despite the strength of the dollar and high real interest rates, gold remains at a high level of $2,000.

The reason behind it is also very simple, behind the sharp rise in US bond yields is actually the downward trend of US government credit, which is essentially a credit premium.

At this time, gold will remain strong as a proxy or antithetical indicator of the US dollar, and we believe that gold will continue to hit new highs in the next year or two.

Real interest rates remain the main driver of gold prices

UBS has a slightly different view of the impact of real interest rates on gold prices than investors, who believe that real interest rates remain the main driver of gold prices.

Although the extent of this relationship has changed over time, one key aspect of it remains – it is asymmetrical. When interest rates fall, gold rebounds more than when interest rates rise.

Gold's sensitivity to real yields has declined this year relative to historical levels, but this asymmetry remains, making gold an attractive alternative outside of the bond space that could prepare for lower interest rates in the future.

UBS found that for every 100 basis point decline in the 10-year Treasury real rate, gold rises by 11%, but falls by only 4.2% when the monthly increase is the same.

Therefore, if real interest rates fall in the coming year, gold is expected to benefit. In addition, UBS found that when real interest rates fell below 1.25% and continued to fall, gold prices rose even more, reaching 14%.

In addition, UBS expects gold to continue to strengthen in the first half of 2025 as real interest rates may fall below this threshold. According to the agency's estimates, the real yield on the 10-year Treasury note will fall by 160 basis points over the next two years from its 2023 high.

Central bank gold purchases are expected to continue

According to data released by the World Gold Council, global central banks bought 337t of gold in the third quarter of 2023, the third highest quarterly net purchase on record, and in the first three quarters of this year, global central bank demand increased by 14% year-on-year to a record 800t.

UBS said that while the unusually strong buying momentum of recent years is unlikely to continue, purchases have historically remained high.

While these gold flows are unlikely to drive price increases on their own, they will continue to play a key role in holding the market up and supporting the overall upward trend.

UBS noted that gold's resilience to rising real yields over the past few years is largely due to a historically large increase in official gold reserves, which largely absorbed the gold sold by investors.

"Central banks are snapping up gold again amid reduced supply, which could push gold above $2,100..."

This article does not constitute personal investment advice, does not represent the views of the platform, the market is risky, investment needs to be cautious, please make independent judgment and decision-making.