Interpreting Minimum Viable Issuance (MVI): Balancing ETH safety with inflation

Written by Anders Elowsson

Compiled: DeepTide TechFlow

introduce

I think it's important to achieve Minimum Viable Issuance (MVI), which is an important commitment to the average Ethereum user. Staking should keep Ethereum safe, not become an inflation tax, while reducing utility and liquidity, creating oligopolistic risk.

Ethereum is constantly evolving and may drive the global financial system in the future. We must assume that "ordinary users" will know about the inner workings of Ethereum as much as ordinary people know about the current financial system.

Of course, we can't assume that the average user will be driven by some ideology, just as Ethereum was created in the first place. Our job is to make sure the right incentives are in place so that Ethereum can grow unhindered.

An important design principle that existed since the birth of Ethereum is "minimum viable issuance" (MVI), which means that the number of ETH issued by the protocol should not exceed the amount required for strict security. This principle is reasonable both under Proof of Work (PoW) and Proof of Stake (PoS).

Under PoW, MVI works to prevent miners from charging excessive inflation taxes to regular users. As a result, the block reward is reduced from 5 ETH to 3 ETH and finally to 2 ETH.

Under PoS, the MVI principle should also be upheld and not excessive inflation taxes are charged to ordinary users. Ordinary users should not need to worry about the details of staking to avoid their savings being eroded, or supporting validator sets that may be censored, etc.

Therefore, MVI is essentially being able to maintain the collateralization ratio (the proportion of all ETH used for staking) at a sufficiently high level, but not higher. In this article, I will try to illustrate why issuing more than the "minimum feasible amount" reduces the utility of Ethereum.

The benefits of MVI for user empowerment

There are various opportunity costs for individuals to participate in staking. It requires resources, focus, and technical knowledge, or trusting a third party, while also reducing liquidity. Liquidity Staking Tokens (LST) are not as reliable as native tokens and are not as suitable as currencies or collateral as native tokens.

Therefore, individuals hope to be able to earn rewards by staking. Define their minimum expected yield to be the lowest yield they are willing to stake (using their best way to stake). Ethereum's (inverse) supply curve is then derived from the minimum expected yield for future ether holders.

The reserved yield of holders can be described as the "no-difference point", at which point the utility they receive from staking is equivalent to not staking. This means that lowering the issuance can actually increase utility for everyone, even stakers, as long as Ethereum remains reliable and secure.

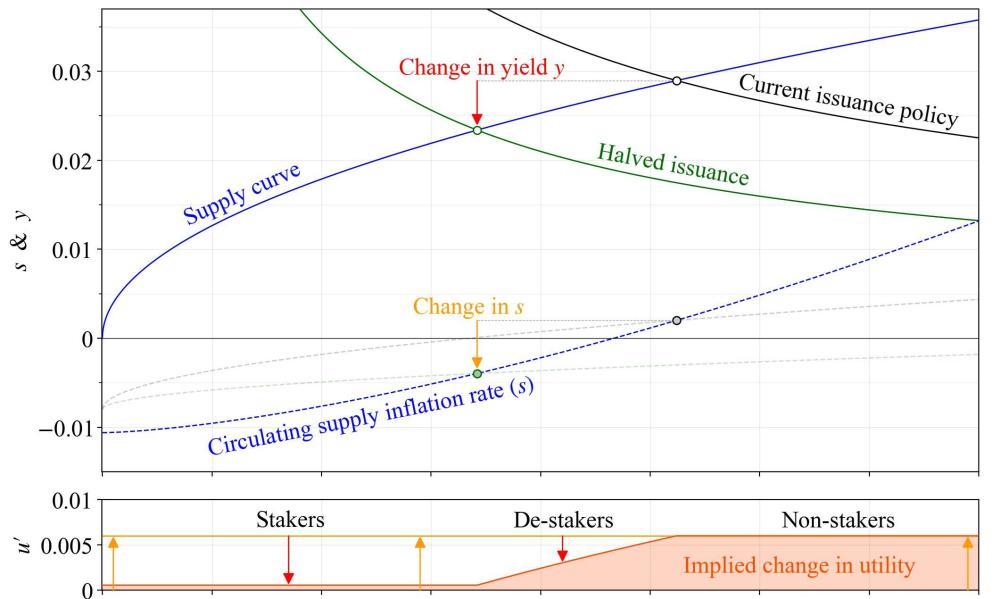

Consider a hypothetical supply curve (blue) with a supply-yield elasticity of 2. In this example, I set it to 2% yield when the number of collateral D reaches 25 million ETH, i.e. when 25 million ETH is staked, the minimum expected yield for marginal stakers is 2%.

The supply curve in reality is a rather complex phenomenon, and we have not yet reached the equilibrium point where we can anchor its position, but we will start with this simple and fairly realistic scenario. We will also ignore the complexity of compound interest.

The burn rate b is set to 0.008. This is the number of burned ETH as a proportion of the total supply expressed in annualized terms since the merger. But this is not the key point, because we are concerned with the shift in supply and demand between the medium-term equilibrium points (circles), not the drift of the total supply of ETH.

Realized Withdrawal Value (REV) (slightly over 300,000 ETH per year) has been added to the protocol issuance to form a black demand curve (current policy) and a green demand curve (halving the issuance by reducing the base reward factor F from 64 to 32).

The halving issuance lowers the yield y (red arrow). This reduces the issuance yield yi=y-yv (where yv is the yield from REV), which reduces the issuance i=yid and the circulating supply inflation rate s=i-b (orange arrow).

In a year, the percentage of outstanding ETH holdings that someone can obtain changes P, depending on s and the yield y y of each holder, according to the formula: P=1+y/1+s-1

The current issuance policy gives P1 and the halved issuance gives P2, then their proportional relationship is: P′=1+P2/1+P1-1

The relevant amount of utility change is defined as u′=P′, but when calculating P2, for those who stop staking, their respective lowest expected rate of return is used. Below that yield, they wouldn't have staked in the first place, so they won't suffer additional utility losses as the yield falls further.

According to this definition, everyone gains higher utility at the new equilibrium point. While stakers see a decline in earnings, the decline in supply inflation is greater, which allows them to receive a larger percentage of ETH.

Of course, non-stakers are obviously better because the only change for them is that less ETH is issued to stakers. The person who stops staking is the only participant who receives a reduced percentage of the outstanding ETH at the new equilibrium point.

Despite the friction, their situation is implicitly better due to increased utility. For example, marginal stakers at the old equilibrium point do not care about staking at all, so they can stop staking and get the full utility improvement brought about by supply deflation.

When people who stop staking find themselves somewhere in between, they still benefit from falling inflation, but suffer some losses in earnings until they become indifferent to staking and destaking. We've shown that from a utility perspective, the publishing policy is not a zero-sum game.

In addition, the utility boost obtained by any group will generally benefit all token holders.

As long as there is the underlying ETH, everyone can benefit from MVI. This does not include CEX and other staking service providers (SSPs) that profit from staking fees. They will not benefit from a reduction in supply inflation and want to keep yields high to keep production cuts high.

But issuances above MVI force unwilling stakers to suffer a decline in utility when staked, or a decline in economic consequences when not staking. Under the realistic supply curve, even willing stakers can get worse. Note that the example doesn't even account for tax implications.

A PoS cryptocurrency with a yield of 5%, everyone stakes, and the average tax on the staking yield is 20%, with 1% of its market cap being taxed every year. This is higher than the amount of Bitcoin that will dissipate to miners after the next halving.

The debate does not necessarily depend on the user's perception of the level of taxation or how the staking proceeds are interpreted. We can still conclude that by enforcing MVI, Ethereum remains more neutral in terms of differences in tax policies between nation-states.

Arguably, Proof of Stake requires lower rewards to achieve the same level of security as Proof of Work, and it's important to take advantage of this to maximize user utility. For example, the total reward with a yield of 2% and a stake of 25 million is Y=0.02× 2500=500,000 ETH.

The "rate of return" for maintaining this solid security is about r=Y/S=0.4%, which is surprisingly low. We take full advantage of this to maximize utility to our users. The potential balance with the current issuance policy is indicated by a black circle.

The yield is about 3%, and 50 million ETH is staked, which is Y=1.5 million ETH/year. The difference in rewards of 1 million ETH per year (over $1 billion at current token prices) can be awarded to Ethereum users in a way that does not dilute token holders.

For MVI, an average withdrawal of 15% of the staking fee will provide CEX and SSP with approximately $250 million in excess profits per year. Some will be passed on to the company's shareholders, and some may be used to lobby to keep yields above MVI forever.

From a macro perspective, the benefits of MVI

I often think that ether permeating the ecosystem is desirable. In the case of L2, Bridging Ethernet increases their financial security by tying L1 and L2 together and providing external funding to users on L2.

If you create a system where users have to rely on some kind of opinionated ETH derivative as funding to avoid inflation taxes, the entire ecosystem is more vulnerable to destruction.

For example, consider the following scenario: a user who cannot stake gives their ETH to the organization (SSP) running the authenticator for them. These organizations can issue LST as collateral and use it on Ethereum.

If the protocol does not operate under MVI but at a higher deposit ratio, one or a few LSTs may replace the currency in the Ethereum ecosystem, embedding it in every layer and application. What is the impact of this?

First, the positive network externalities introduced by monetary capabilities may allow LST to remain dominant, while its SSP provides worse services than competitors (e.g., charging higher fees or simply offering poorer risk-adjusted rewards).

Second, and most importantly, LST holders and any applications or users who need LST preservation will share a common destiny with LST and eventually LST Issuing Organizations (SSPs).

This requires Ethereum to destroy a large part of itself. Affected users may prefer to reinterpret the mistake or misconduct as something completely different. Once you become the currency of Ethereum, you become the social layer in a way. We are no longer only concerned with the proportion of ETH staked under LST, but the proportion of total ETH under LST. Corrupt institutions are correspondingly placed on top of consensus mechanisms.

It is clear from The DAO that if the proportion of total circulating supply affected by outcomes becomes large enough, the "social layer" may shake its commitment to potentially expected consensus processes.

Risk mitigation in the form of the early warning system discussed by Buterin may not be effective if the community can no longer effectively intervene in an event such as a 51% activity attack.

In this case, the consensus mechanism becomes so large and interconnected through derivatives that its ultimate arbiter, the social consensus mechanism, is overloaded.

Now consider different scenarios under MVI. First, each LST will face tougher competition from non-staked ETH. As a result, the ability to monopolize monetary functions and then charge high fees or offer higher-risk products diminishes.

Second, the social layer will continue to be tied natively to Ethereum and ETH, rather than to external organizations and their issued ETH derivatives. Keeping the collateralization ratio low enough through MVI changes the participants' risk calculations.

Under MVI, when the collateralization ratio is low enough to prevent moral hazard from developing, the proxy problem (PAP) can be priced more accurately when the collateral ratio is low enough to prevent moral hazard from developing. No LST will grow to the point of "too big to fail" in the eyes of the Ethereum social layer.

This pricing would reflect the fact that the greater the share of the pledge controlled by an agent acting on behalf of the principal (or any party able to intervene in the relationship), the better its chances of gaining a deterioration of consensus for its own gain.

The principal staker must always consider what security guarantees it has (e.g., the value risk of the staking agent or the intervening party) and know that it could lose everything if the worst happens.

Taking out the direct dominance of the Ethereum currency, and assuming that the deposit ratio has grown to utility-maximizing scale under MVI, larger SSPs are likely to find a non-monopoly strategy more profitable (i.e., increased fees).

This is just a comment related to the present. But importantly, it reflects the fact that for every "cartel class" we can eliminate, the value proposition of secure and consistent SSPs has increased relatively much.

An important step towards MVI is MEV burning, which may also have the potential to eliminate the "cartel class" that is more important than the function of money. MEV burning helps reduce the reward variance of independent stakers, which increases if the issuance yield is reduced.

It also brings greater precision to targeting MVI because it eliminates a source of revenue that may change over time in a way that cannot be predicted in advance.

It is worth noting that various approaches may be employed in the future to deal with the principal-agent problem (i.e., one-time signature) in some aspects of delegated staking. But fundamental questions of building trust, monopoly incentives, and censorship can be hard to escape.

Another benefit of MVI is that it improves the conditions for (independent) staking, which is directly related to the staking size, the number of validators, and the size of validators. If the staking size changes, so does the validator size or number of validators (network load).

This effect spreads throughout the protocol design space and affects any targets that may be substituted for higher or lower network loads, such as parameters related to variable validator balances.

This is an essential attribute of the current consensus mechanism. If the issuance policy results in d=0.6 instead of d=0.2 at the medium-term equilibrium point, independent staking will require three times the ETH in order to maintain the same network load, all other things being equal.

Going back to the basics, I think the most important benefit of MVI is its ability to provide utility to the average user. Ethereum is in a unique position to be able to make native cryptocurrencies a global currency, and I think this is an opportunity worth pursuing.

When countries implement price inflation by increasing the monetary base, they control the choice between time for ordinary people and believe that this control is still feasible in a digitized and globalized world.

Ethereum should not control ordinary people, nor should they be forced to save liquid energy. We should give them maximum ease of use and utility from the Ethereum currency. The "risk-free rate" in Ethereum is simply holding (and trading) ETH.

Address potential issues with MVI

After elaborating on the potential benefits of MVI, the second part will address some of the suggested drawbacks. These include reduced economic security and the notion that if we lower yields, delegated staking will replace all independent staking.

This is indeed true when it comes to the first point, since a higher deposit ratio does force the attacker to spend more resources, for example, to restore finality. This is not something to be taken lightly.

Our goal is not "minimum issuance". We must always make sure that it is "doable". Buterin offers some visual explanations of how expensive the Ethereum 51% attack should be.

We can also think of the nearly 14 million ETH that secured Ethereum at the time of the merger as a "preference" of staking that the ecosystem considers secure enough under the current consensus mechanism (in terms of resisting women's attacks, not just super committee accountability).

At the same time, having a decent margin is really good, and the current mortgage ratio (d≈0.2) may also provide a meaningful improvement in the resistance to false accounts compared to the mortgage ratio at the time of the merger (d≈0.1).

The slope of the reward curve cannot be too steep, which is why we may want to operate at a certain distance from the preference point and eventually determine d from the probabilistic analysis of staking supply and demand.

Some might argue that delegated staking somehow makes it easy to attack resource allocation, which is just "superficial" security. But by exposing all staking to penalties and eliminating moral hazard (through MVI), the settlor must be very careful when entrusting staking, as mentioned earlier.

In this setup, the market determines the appropriate capitalization ratio for the staking operator and prices the risk of staking. Instead, Ethereum is responsible for punishing misconduct and maintaining the value of ETH relative to the value it assures.

By ensuring that ETH tokens penetrate the real economy and that all consensus participants have a real stake, we set a price for attacks that are more difficult to avoid through financial engineering.

I mention this because there are indeed some interesting alternatives being discussed, where Ethereum intervenes in the denomination process without any risk to the delegator. Then the risk is much lower for principals who contribute to the deterioration of consensus.

Or at least it seems. When Ethereum forks and/or must be rescued through social intervention, risk-free principals may be surprised at how the social layer evaluates their mandates and the damage they are perceived to have caused if the worst happens.

Here I return to Buterin's request again, don't overload the consensus. My point and one of the themes of this article is that when the percentage of ETH involved in the consensus process is very high, everyone gets involved and may not achieve a "neutral" outcome.

The conclusion on the first question is that d under MVI must be kept large enough to ensure security, and delegation does reduce security to some extent, but as long as their staking is risky, parties will try to assess the risk and delegate wisely.

Retaining independent stakers is indeed a complex puzzle. Economies of scale are difficult to design to eliminate, and we don't pay enough attention to liquidity in staking. However, there are some nuances in the current argument that are more favorable to MVI, which I hope to be able to raise.

Ethereum's independent family stakers incur a certain cost when staking. They paid a large part of the cost upfront, including access to knowledge. They also incur variable costs such as bandwidth, troubleshooting time, and risk of outages.

Many of Ethereum's SSPs also incur significant costs when designing their services and incur other types of operating costs that independent stakers don't have to worry about. However, they rely on economies of scale to reduce the average cost of operational validators.

We must assume that SSPs seek to maximize profits and can consider what their fees might be under different balances. What is the difference between economies of scale between d=0.2 and d=0.6? It seems reasonable to assume that the average cost of SSPs is much lower at d=0.6.

Recall that at d=0.2, a staker alone might be able to run a validator d=0.6 three times smaller. In terms of the proportion of individual stakers we can attract, there may be a difference between a minimum number of validators of 32 ETH and 96 ETH (or 11 ETH - 32 ETH).

Therefore, not only does a higher d force independent stakers to have more ETH under the same network load, they must also compete with SSPs that can charge lower fees. While fees will be set based on market strategies, average costs should ultimately be important.

If we reduce earnings, SSPs want to need to raise expenses to appropriately cover and amortize costs. The cost of delegating a staker is variable and includes PAP and fees. They can easily get rid of the increased fees.

The argument that reducing yields will cause independent stakers to leave (earlier than commissioned stakers) should be taken seriously. But because current home stakers have already incurred fixed costs, their current elasticity of personal income supply may not be high.

However, if we reduce the payoff to a point where it makes it unfeasible for families to stake independently (including for new entrants), their lower resilience in the short term will not help. If we want to maintain independent staking, there is a minimum staking total return that we cannot fall under.

Assume that the total cost of independent household staking (denominated in ETH) is C, and other factors such as the annual risk to funds at the time of staking are considered R. Then, the payoff must be higher than y>C/32+R, even if restaking brings liquidity, a reasonable margin is required.

Here, too, I want to discuss the impact of DeFi revenues. All stakers receive the benefits y, which are intrinsically derived from staking. This "organic gain" comes from issuance, MEV and priority fees. Some may also receive "exogenous benefits" outside of the consensus mechanism.

It is not possible to simply sum y+yc for LST holders and conclude that LST holders always profit relative to independent stakers, no matter how y falls. It can be expected that ETH tokens will bring higher utility relative to LST (when their intrinsic benefits are not taken into account).

The delegate staker must weigh y(1-f), where f is a percentage fee, relative to the risk/cost including the inherent disadvantages of PAP and LST relative to native ETH, and only decide to stake if y(1-f) (not y+yc) exceeds these costs.

When y=0, the broker does not delegate the stake. They can get better liquidity or higher yc with native ETH and face serious disadvantages by delegating staking to SSPs that are losing operations. Independent stakers may not stake either.

For someone who wants to hold ETH anyway, the decision may not depend on whether YC is 1% or 5%. At 5%, ETH can be expected to provide +5%. Of course, that 5% carries risk and is not a free currency (nor should our earnings be, hence the MVI).

As Y rises, potential independent stakers and delegated stakers will gradually find the claims of staking worthwhile, starting with the most ambitious/risk-taking ones. Here we are forming a supply schedule in which each agent makes a decision based on its specific situation.

The distribution of the minimum expected yield between potential independent stakers and delegated stakers is unclear. At the medium-term equilibrium point of d=0.2, the proportion of independent stakers may be lower than d=0.6, but another option is also likely.

A higher d may allow SSPs to be more diversified, but the cartel class of monetary functions puts pressure on this. There is also a limited percentage of individuals with enough ETH for standalone staking, which sets a soft cap on the total number of unique stakers.

This is indeed a topic that deserves further study. The point is that the opportunity cost of staking must always be fully accounted for, and economies of scale and monopolies can affect fundamental equilibrium analysis in quite complex ways.

Finally, restaking has the potential to make independent stakers more competitive. It allows them to "re-mortgage" their pledge when they wish (however, they themselves may also encounter principal-agent problems if they want to provide financial security).

One benefit of restaking is that if Active Verification Service (AVS) can quantify decentralization, it can also give economic surplus value to decentralization. This is something that Ethereum cannot do as an open protocol.

The previous argument also applies to functional restaking of EigenLayer outside the regulations. At very low yields, users are better off using non-staking ETH (free staking) directly. It seems reasonable for many use cases for AVS to prefer a token that won't evaporate easily.

Also note that if PEPC expands its scope beyond the "block production use case", the resulting benefits may become more endogenous, depending on the remaining utility provided.

Looking to the future

This concludes the discussion about the advantages and disadvantages of MVI. While there are some concerns about staking alone, MVI is a fundamentally sound design policy that gives Ethereum a real chance to provide users with the best digital currency ever.

Each argument has its nuances, and some discussions cannot be concisely expressed in a tweet. But I think all things considered, it should be possible to accept that MVI is also a favorable design principle under PoS.

We must always focus first on "ordinary users", which requires research based on micro foundations and assessing how we can maximize utility for ordinary people when Ethereum (hopefully) becomes their new financial system.

So the question is how do we implement MVI, which is something I've been digging into deeply. Dietrichs mentioned the importance of communicating current distribution policy research on a recent developer call, and my journey began with this tweet.

Changing the issuance policy is a sensitive issue. What we aspire to is a distribution policy that maximizes utility without further developer intervention, so that it can always be proportioned to MVIs that maximize utility.

However, the current reward curve does not allow this protocol to affect the collateralization ratio (security), but rather the staking size. In the medium term, the results are closely related to these two, but in the long term, there may be a clear divergence, with the drift of circulation supply.

This is the topic of my 2021 article at Ethresearch and my talk at Devconnect: Defining how the circulation supply S drifts toward equilibrium (i=b) so that we can improve the reward curve and achieve a minimum viable issuance under proof-of-stake.

Since according to the current reward curve, the issuance i can be expressed as i=cF√d/√S, it will change with changes in the circulating supply (the collateral ratio d provides some room for adjustment). The graph shows the issuance rate diagonal of Ethereum and the average b since the merger.

The burn rate b does not depend on the circulating supply – the demand for block space does not change due to changes in the unit of currency denomination. If i > b, S rises and pulls i down until it equals b. If i

In 2021, there was no REV for stakers, so I directly used the minimum expected yield y-, and came to the fact that Ethereum's security is d=b/y.

Today, we simply add the "REV rate" v to the equation to get d=(b+v)/y. This is that we cannot control the collateralization ratio and security in the long term unless we are prepared to change F from time to time.

We can cut F as a temporary solution to avoid paying too much for security (this will be discussed in the next tweet). However, Ethereum will eventually return to the same long-term equilibrium collateralization ratio at a lower circulating supply (all other things being equal).

That's why we ultimately want to change the reward curve to be d related rather than D related. It is then tempting to simply replace D with S0d (where S0 is the current circulating supply). This brings us a step closer to an autonomous issuance policy, but there is still no guarantee that it will be achieved.

Assuming MEV burning, then the protocol can fully adapt to income changes, but still cannot accommodate the expected yield, i.e., a permanent shift in the supply curve. This can be handled by allowing the entire reward curve (demand curve) to drift slowly.

The ultimate goal is a dynamic equilibrium in which the circulating supply can change at a constant rate in the absence of external influences. Whether it is inflation or deflation depends on the supply curve and how the value of the block space is reflected in the ETH market cap.

So we achieved what Polynya calls "constant" security, which I think aptly describes our ultimate goal, to eventually wrest control of the issue from developers and make Ethereum autonomous under MVI.