Affected by the bottom of the industry cycle, SMIC's fourth-quarter revenue ended seven quarters of growth.

SMIC said that the industry cycle in the first half of the year is still at the bottom, the impact of external uncertainties is still complicated, revenue in the first quarter of 2023 is expected to decline by 10% to 12% sequentially, and gross margin is expected to fall to between 19% and 21%.

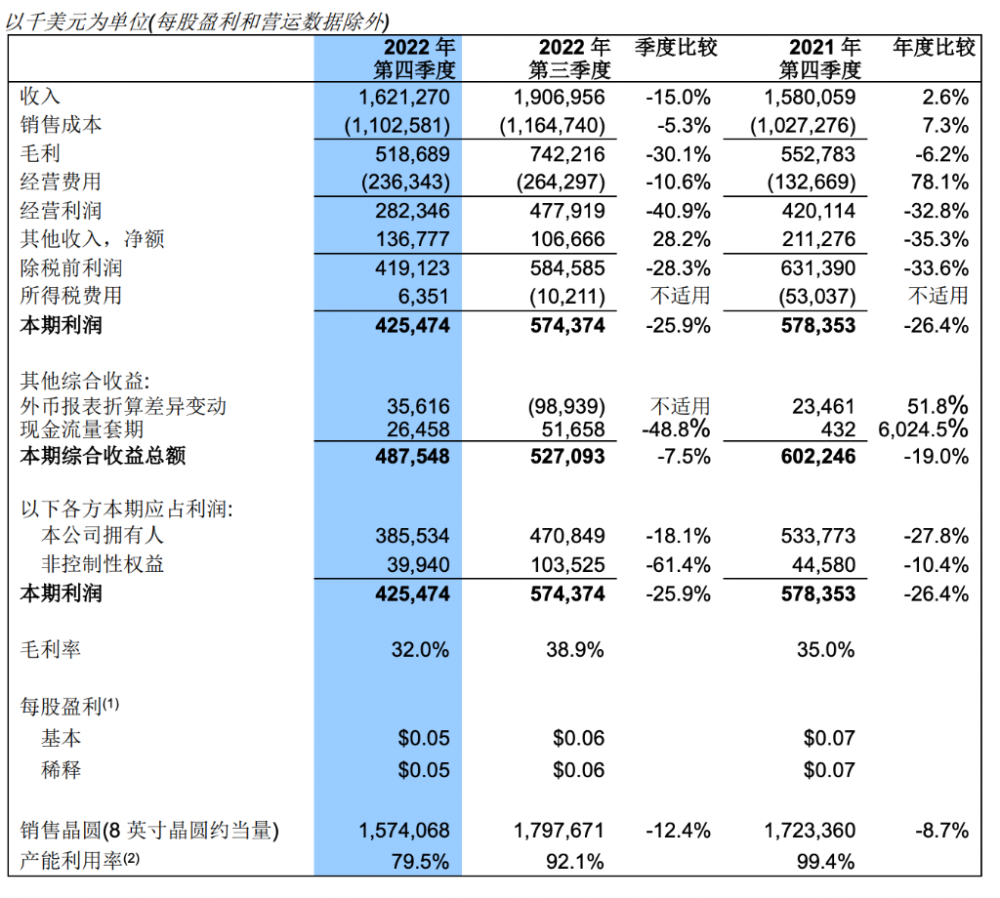

Q4 revenue fell 15% month-on-month, and this year's Q1 is expected to decline 10%-12% month-on-month

On the evening of February 9, SMIC disclosed its fourth quarter and full year results for 2022, with SMIC's fourth-quarter revenue of US$1.62 billion, estimated at US$1.65 billion, an increase of 2.6% year-on-year and a decrease of 15% sequentially. Fourth-quarter net income was $385.5 million versus $310.3 million.

In addition, SMIC's gross profit for the fourth quarter of 2022 was $518 million, and the gross margin for the fourth quarter was 32%.

In 2022, the sales revenue for the whole year was US$7.273 billion, a year-on-year increase of 34%, achieving an annual growth rate of more than 30% for two consecutive years in 2021 and 2022, and the gross profit margin increased to 38% in 2022, a record high.

By business, the proportion of wafer revenue fell to 91.1% from 92.5% in the third quarter. Among them, smartphone revenue accounted for 28.6% of wafer revenue in the fourth quarter, up from the previous quarter; Smart home and consumer electronics accounted for 10.8% and 21.6% of revenue, respectively, down from the previous quarter; Others accounted for 39%, showing a steady increase. In addition, 8-inch wafer and 12-inch wafer business revenue accounted for 35.6% and 64.4%, respectively.

Regarding performance, SMIC said:

Fourth-quarter sales revenue of $1,621 million, gross margin of 32%, mainly due to the decline in capacity utilization and product sales in the fourth quarter of 2022, in line with the company's judgment and guidance on the industry.

The company's annual capital expenditure was US$6.35 billion, and by the end of the year, the equivalent of 8-inch monthly production capacity reached 714,000 pieces, and the annual capacity utilization rate was 92%. By the end of 2022, SMIC Shenzhen will enter the production stage, SMIC Beijing will enter the trial production stage, SMIC Lingang will complete the capping of the main structure, and SMIC Xiqing will begin civil construction. SMIC Capital is expected to delay the delivery of bottleneck equipment by one to two quarters.

Looking ahead to 2023, the industry cycle in the first half of the year is still at the bottom, the impact of external uncertainties remains mixed, and the company's guidance for the first quarter is that revenue is expected to decline by 10% to 12% sequentially and gross margin is expected to fall to between 19% and 21%:

Based on the premise of a relatively stable external environment, the company expects that the year-on-year decline in sales revenue in 2023 will be ten digits lower, and the gross profit margin will be about 20%. Depreciation increased by more than 20% year-on-year, and capital expenditure was roughly flat compared to the previous year. By the end of the year, the monthly production capacity increase was similar to the previous year.

Capacity utilization continues to decline Capital expenditures are expected to be flat

In the fourth quarter, the company's production capacity continued to rise, but capacity utilization continued to decline. According to the financial report, the company's monthly production capacity increased from 706,000 8-inch wafers in the third quarter of 2022 to 714,000 8-inch wafers in the fourth quarter of 2022, and the capacity utilization rate fell from 92.1% in the third quarter to 79.5%.

Capital expenditures increased in the fourth quarter, with the company reporting R&D expenses of $197.5 million and capital expenditures of $1.98 billion in the fourth quarter, $1.82 billion in the third quarter and $6.35 billion for the full year. Capital expenditures planned for 2023 are broadly flat compared to 2022, mainly for the expansion of mature capacity and the construction of new plant infrastructure.