(Report Producer/Author: Northeast Securities, Wang Xiaoyong)

1. Energy change is an inevitable trend, and green power will become the main energy source

Green electricity refers to electricity with zero or near-zero carbon dioxide emissions in the production process, which has a much smaller impact on the environment and is greener than traditional thermal power generation. The sources of green electricity include hydropower, wind energy, solar energy, hydrogen energy, biomass thermal energy, geothermal energy, etc. Green power is a clean energy source in the narrow sense. Natural gas is also generally considered a generalized clean energy source because its carbon emissions are lower than that of coal and oil, which are traditionally high-carbon energy sources and are relatively pure.

The degree of carbon emissions from various energy sources can be expressed in terms of carbon content per unit calorific value. High-carbon energy sources include coal and oil, where the carbon content per unit calorific value of coal is about 26t/TJ and oil is about 20t/TJ. Natural gas is relatively low carbon, with a carbon content of about 15t/TJ per unit calorific value. Hydropower, wind power, solar energy, etc., almost do not emit carbon in the process of generating electricity.

1.1. Energy consumption will continue to increase over the long term as the economy develops

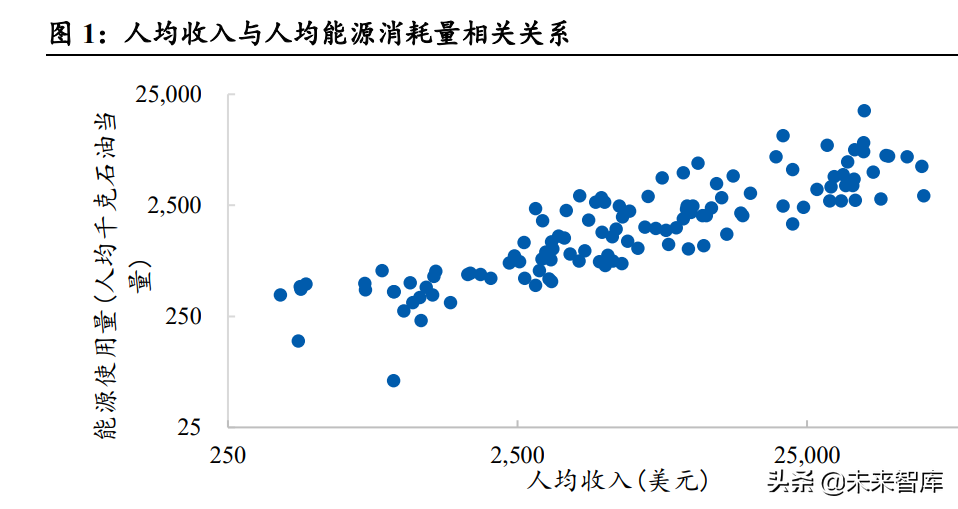

Energy is one of the important elements for human survival, and the improvement of people's production efficiency and quality of life is inseparable from the large use of energy sources. By analyzing World Bank statistics, we found a significant positive correlation between per capita income levels and per capita energy use. Globally, in 2014, the world's per capita income was $8,323 and per capita energy consumption was 1,920 kilograms of oil equivalent. Developed countries such as the United States, Germany, and Japan have reached 3.63, 1.97, and 1.81 times the world average respectively. In India and sub-Saharan Africa, per capita energy consumption is only about 1/3 of the world average (of course, this also has the influence of latitude, and high latitudes consume more energy due to cold).

Overall, the higher the per capita income, the higher the energy consumption per capita. This also confirms the statement that in the traditional energy structure fueled by oil/coal/natural gas, the right to carbon emissions is the right to development. In the future, as human beings continue to pursue a better life and the economy continues to develop, the global energy demand/consumption will continue to increase.

1.2. The ecological risks posed by the continued massive emission of carbon dioxide are intolerable

The greenhouse effect refers to the effect of a planet's atmosphere absorbing radiation energy, causing the temperature of the planet's surface to rise. The gases that cause the greenhouse effect are called greenhouse gases, including carbon dioxide, methane, various HCFCs, ozone and water vapor. Human activities, especially since industrialization, have led to an increase in greenhouse gases in the Earth's atmosphere. Global emissions of about 51 billion tonnes of greenhouse gases into the atmosphere each year are on the rise. Carbon dioxide emissions increased from 11.189 billion tons in 1965 to 34.356 billion tons in 2019, an increase of 207% in 54 years, with a compound annual growth rate of 2.1%.

The concentration of carbon dioxide in the atmosphere has increased by more than 1/4 in the past 100 years, and there are currently records of carbon dioxide concentrations of more than 400 ppm in many meteorological monitoring stations around the world, more than all historical periods since the emergence of humans. High concentrations of greenhouse gases cause the global thermal cycle to become unbalanced, and temperatures rise, leading to drastic environmental changes. Although the specific changes in the environment after global warming cannot be accurately predicted, the ecological risk is clearly beyond the range of human tolerance. Reducing carbon emissions and curbing global warming trends have gradually become a consensus.

1.3. Green electricity will gradually replace oil and gas as the main energy source

According to the research of Zou Caicai, an academician of the Chinese Academy of Sciences, and others, the energy revolution in history has experienced the conversion of firewood to coal and coal to oil and gas, and is currently in the period of oil and gas conversion to new energy. Looking back, the earliest human energy source was firewood, which met basic needs such as cooking and heating. With the advancement of technology, the invention of steam technology and coal-fired power generation technology has greatly promoted the development of the coal industry, and coal has gradually replaced firewood as the mainstream. In the mid-20th century, the rapid development of internal combustion engine technology created a common prosperity of the oil and gas industry and the automobile industry, and the proportion of total oil and gas consumption increased rapidly.

Today, as curbing global warming becomes a consensus and countries continue to make carbon reduction commitments, the mainstream status of high-carbon energy will gradually be replaced by clean energy. Under the Paris Agreement reached in 2015, countries and regions around the world will work together to limit the increase in global temperature to 2°C above pre-industrial levels, and to this end countries are required to submit a revised emission reduction plan every five years, that is, a country-determined contribution to the reduction. In 2020, countries and regions have made the latest emission reduction commitments. Among them, the United States, Japan, South Korea, the European Union and other commitments to achieve carbon neutrality by 2050, China and Saudi Arabia to achieve carbon neutrality by 2060, and India to achieve carbon neutrality by 2070.

Before the rise of new energy sources, natural gas was seen as the main way to reduce carbon emissions to mitigate the greenhouse effect. From 2000 to 2019, the mainland's natural gas consumption increased from 24.5 billion cubic kilometers to 306 billion cubic kilometers, an increase of 11.49 times, with a compound annual growth rate of 14.21%.

In recent years, the rapid advancement of new energy technology has made the cost of obtaining green electricity continue to decline. Among them, the cost of onshore wind power on the mainland has dropped from 0.41 yuan / kWh in 2012 to 0.23 yuan / kWh in 2020. The cost of kWh on commercial-side PV fell from 0.93 yuan/kWh in 2012 to 0.41 yuan/kWh in 2020. The cost of kWh of user-side photovoltaics decreased from 1.04 yuan/kWh in 2012 to 0.43 yuan/kWh in 2020. The cost of onshore wind power and photovoltaic power generation has approached the benchmark price level of coal-fired benchmarks, making the large-scale application of green electricity gradually have a realistic economy.

1.4. The resource conditions for the development of green electricity in the mainland are relatively good, and the potential space is huge

In terms of wind energy resources, according to the calculation of the "China Green Power Development Overview", the average annual wind power of the layer on the mainland with an average wind power density of 300W/㎡ can be developed in 2000/2570/3400GW, respectively, and the resource-rich areas are mainly in the northeast, Inner Mongolia, northern China, Gansu Jiuquan and northern Xinjiang. Within 100 meters offshore, wind power technology with a water depth of 5-25 meters can be developed at about 190GW, and within a water depth of about 320GW within 25-50 meters, and the resource-rich areas are mainly in the Taiwan Strait of China, eastern Guangdong, Zhejiang offshore and north-central Bohai Bay.

In terms of solar photovoltaic power generation, the mainland is rich in resources, according to the information of the National Meteorological Science Data Center, 2/3 of the mainland has an annual radiation volume of more than 1400kWh/㎡, and the theoretical reserves of land solar energy are as high as 1.86 million GW. However, the solar energy resources between various regions on the mainland vary greatly, and the overall performance is that there are fewer resources in plains and rainy and high wetland areas, and there are more resources in plateaus and dry areas with less rainfall.

The current national standard "Solar Resource Grade - Total Radiation" in the mainland divides the annual irradiation of total solar radiation into four grades: A, B, C and D. In 2020, the mainland's annual irradiation above 1750kWh/㎡ is mainly in the Qinghai-Tibet Plateau, northern Gansu, northern Ningxia and other regions, the annual irradiation is 1400-1750kWh/㎡ mainly in Shandong, Henan, southern Guangdong and other regions, the annual irradiation at 1050-1400kWh/㎡ is mainly in the middle and lower reaches of the Yangtze River, Fujian, Zhejiang and other regions, the annual irradiation is less than 1050kWh/㎡, mainly Sichuan and Guizhou.

In terms of hydropower, there are many continental rivers, large drops, and abundant hydropower resources。 According to the flow and drop of the river, the theoretical value of hydropower resources, that is, the reserves of hydroenergy resources, can be calculated. According to the China Hydropower Engineering Society, the mainland has 676GW of hydropower resources and 378.5GW of developable hydropower resources. Among the ten major river basins in The country, the largest developable hydropower resources are the Yangtze River Basin, the Brahmaputra River and other river basins in Tibet, and the Southwest International River Basin, reaching 197.2GW, 50.4GW and 37.7GW respectively。

2. The steady progress of the dual-carbon strategy demonstrates China's determination and confidence in carbon reduction

Double carbon refers to carbon neutrality and carbon peaking.

2.1. Policy guidance is the key to the development of green electricity

The core driver of this round of energy transformation from oil and gas to green electricity is the protection of the natural environment. There is a famous concept in microeconomics called the tragedy of public goods, which describes the fact that public goods with limited resources are doomed to waste when the public can use them freely, which in turn reduces the overall utility of society. The natural environment is a typical public goods. In fact, the concept of public tragedy was first proposed by biologist Garrett Hardin in Science, which focused on the management of the natural environment.

From the perspective of the externality of economic activities, because the act of protecting the environment and polluting the environment has an impact on society and other individuals, but there is no corresponding obligation or return, in the absence of third-party intervention, there will be problems of insufficient consumption and excessive consumption, respectively. In order to improve the overall effectiveness of society, the government must intervene in these acts by: 1) internalizing externalities through subsidies and taxes; 2) Clearly identify private property rights - carbon accounting; 3) Reduce transaction costs – build an efficient carbon exchange.

Subsidies and taxes can be achieved through carbon trading. According to the 2021 World Bank's "Carbon Pricing Development Status and Future Trends" report, the world currently generates $53 billion in annual carbon trading, but there is still a lot of potential for carbon pricing. To meet the Paris Agreement's temperature control target below 2°C, the carbon price would need to reach $40-80 per tonne of carbon dioxide equivalent, and regions where carbon prices currently reach that price range together account for less than 5% of global emissions, the report said. China's current carbon price is low, and data from March 10, 2022 show that the national carbon market carbon emission allowance (CEA) price is only 57.26 yuan per ton of carbon dioxide equivalent, and with the further advancement of the dual carbon strategy, China's carbon price is expected to continue to rise.

In terms of carbon accounting, the mainland has formulated carbon emission accounting methods and reporting guidelines for enterprises in a number of key industries, which provides a method reference for the carbon emission accounting and reporting business of enterprises. At present, there are two main methods of accounting for carbon emissions, carbon measurement method and actual measurement method. Carbon metering means that, under the given parameters, the emissions are calculated according to the production activity process of the enterprise, which is the most widely applicable and widely used accounting method, but the accuracy is relatively low. The actual measurement method is to collect samples and submit them to the relevant departments for testing, or to set up monitoring equipment at the emission site for actual measurement.

In terms of carbon exchanges, the mainland's national carbon emission trading market was officially launched in July 2021, and by the end of 2021, it has accumulated 179 million tons of carbon dioxide equivalent and a cumulative turnover of 7.661 billion yuan. China's Certified Emission Reduction Credit (CCER) national trading market is also expected to restart in 2022, encouraging enterprises that do not undertake mandatory emission reduction obligations to take the initiative to develop forestry carbon sinks and other emission reduction projects, and the emission reduction can also be traded as carbon emission reduction products after certification.

2.2. China set a carbon peak target in 2014 and has been exceeding its targets ahead of schedule in the process

During the period from 2015 to 2020, the central and local governments of the mainland have repeatedly announced the completion of carbon reduction targets ahead of schedule.

In the United States, the Trump administration has notified the United Nations in November 2019 that it will withdraw from the Paris Agreement, and the withdrawal process will take one year according to the agreement, and in November 2020, the United States officially withdrew from the Paris Agreement, becoming the only party to withdraw from the Paris Agreement so far. (Source: Future Think Tank)

2.3. The introduction of the dual carbon 1+N policy shows China's determination and confidence in carbon reduction

On September 22, 2021, the Central Committee of the Communist Party of China and the State Council issued the Opinions on The Complete, Accurate and Comprehensive Implementation of the New Development Concept to Achieve Carbon Peak carbon neutrality, referred to as the "Opinions", which is the "1" in the carbon peak carbon neutrality "1 + N" policy system, which clarifies the 3060 double carbon target, that is, China's carbon dioxide emissions will peak by 2030 and achieve a stable decline, and achieve carbon neutrality by 2060.

On October 24, 2021, the State Council issued the Action Plan for Carbon Peaking before 2030, referred to as the Plan, which is the overall deployment of the carbon peaking stage and is a policy document headed by "N". While maintaining the convergence of goals and directions with the Opinions, the Plan will make the tasks before 2030 more detailed. Among them, the target of 20% of non-fossil energy consumption will be advanced by 5 to 2025.

On February 10, 2022, the National Development and Reform Commission and the National Energy Administration issued the Opinions on Improving the Mechanism and Policy Measures for The Green and Low-Carbon Transition system of Energy. At present, the National Development and Reform Commission is studying and formulating carbon peak implementation plans for electric power, steel, non-ferrous metals, petrochemicals, building materials, construction, transportation and other industries.

2.4. The 14th Five-Year Plan clearly guides the direction of green power investment

In March 2021, the 14th Five-Year Plan was released, which clearly guided the focus on investing in the construction of green power assets, building a modern energy system, and promoting the energy revolution. In terms of clean energy bases, it is necessary to build hydropower bases in the lower reaches of the Brahmaputra River, the upper and lower reaches of the Jinsha River, the Yalong River Basin, the upper reaches of the Yellow River, and clean energy bases such as Jiziwan, Hexi Corridor, Xinjiang, Jibei, and Songliao, and build offshore wind power bases in Guangdong, Fujian, Zhejiang, Jiangsu, and Shandong. In terms of coastal nuclear power, it is necessary to promote the construction of three generations of coastal nuclear power, and the installed capacity of nuclear power operation has reached 70GW. In terms of power transmission, it is necessary to build and study and demonstrate a number of UHV transmission channels. In terms of power system conditions, it is necessary to build pumped storage power stations such as Tongcheng and carry out research on large-scale energy storage projects of the Yellow River cascade power station. In terms of oil and gas storage and transportation capacity, it is necessary to build new oil and gas pipelines such as the domestic section of the China-Russia Eastern Line, and to speed up the construction of underground gas storage reservoirs such as Wen 23.

2.5. The tone of steady growth in 2022 is clear, and green power investment may be invested ahead of schedule

In January 2022, the provinces successively issued government work reports, proposing development goals for 2022, which clearly defined the key role of investment and enhanced the driving force for economic growth, including investment and construction with a focus on green electricity.

For example, Yunnan Province proposed to increase fixed asset investment by more than 7% in 2022 (4% in the same period last year), add more than 11GW of new energy installed capacity, strive to start construction of 20GW, and promote the start of 4.8GW of thermal power installed capacity projects. Guangdong Province's target is to increase fixed asset investment by 8% (6.3% in the same period last year), with 5.49GW of offshore wind power, 2.25GW of photovoltaic power generation and 0.7GW of pumped storage. Zhejiang Province aims to increase infrastructure investment by 5.5%, start the construction of 7GW of clean thermal power, 1GW of new energy storage projects, and add more than 4GW of installed wind and photovoltaic capacity. Sichuan Province's goal is to increase fixed asset investment by 8% (10.1% in the same period last year), accelerate the promotion of several 1,000 kV UHV AC transmission projects, actively promote clean energy bases such as the "Sanjiang" hydropower base, and build a national natural gas (shale gas) 100-billion-cubic-meter production capacity base. The goal of the Tibet Autonomous Region is to build a multi-energy storage and multi-energy complementary base for water, wind and photovoltaic storage in the upper reaches of the Jinsha River and the middle reaches of the Brahmaputra River, accelerate the preliminary work of the Yajiang hydropower faucet project, actively promote the construction of GW-level photovoltaic bases and high-altitude wind power, and strive to build and build 16GW of "new energy + energy storage" installed capacity.

3. The high prosperity of green electricity is expected to continue, helping the carbon peak to tackle the tough work

3.1. The total installed capacity of power generation in the mainland continues to grow at a high level, and the proportion of green electricity increases rapidly

The continent's power generation grew from 1,325.6 billion kWh in 2020 to 8,112.2 billion kWh in 2021, an increase of 5.1 times, with a compound annual growth rate of 9.01%. From 2012 to 2021, the total installed capacity of continental power generation maintained steady and rapid growth, from 1142GW at the end of 2012 to 2377GW at the end of 2021, with a compound annual growth rate of 8.49%. During this period, the proportion of various energy types in the installed capacity of power generation has changed greatly.

In 2012, the installed capacity of thermal power / hydropower / wind power / nuclear power / photovoltaic power generation in China accounted for 71.25%/21.79%/5.30%/1.10%/0.57% respectively, and by 2021, the proportion was 54.59%/16.46%/13.83%/2.24%/12.88%, respectively, an increase or decrease of -16.66%/- 5.33%/+8.53%/+1.14%/+12.31% compared with 2012. Judging from the changes in the structure of installed capacity, the proportion of thermal power has declined by a large margin, and the proportion of green electricity has risen. Among green electricity: the proportion of wind power and photovoltaic power generation has increased more; the installed capacity of nuclear power is still in a low position, accounting for only 2.24% of the total installed capacity of power generation in the mainland by the end of 2021; although the installed capacity of hydropower has also increased, the growth rate is lower than that of other green electricity, and the proportion has declined.

In terms of installed capacity of thermal power, from 816GW at the end of 2012, it increased to 1297GW at the end of 2021, with a compound annual growth rate of 4.14%. In terms of installed hydropower capacity, from 249GW at the end of 2012, it increased to 391GW at the end of 2021, with a compound annual growth rate of 5.61%. In terms of wind power installed capacity, from 61GW at the end of 2012, it increased to 328GW at the end of 2021, with a compound annual growth rate of 20.65%. In terms of installed nuclear power capacity, from 13GW at the end of 2012, it increased to 53GW at the end of 2021, with a compound annual growth rate of 6.75%. In terms of installed capacity of photovoltaic power generation, from 7GW at the end of 2012, it increased to 306GW at the end of 2021, with a compound annual growth rate of 53.41%.

3.2. Hydropower: It is expected to maintain an annual investment of 100 billion yuan

The annual power generation of hydropower stations in the mainland showed a steady upward trend, from 328.5 billion kWh in 2004 to 1299.1 billion kWh in 2019, an increase of 2.96 times, with a compound annual growth rate of 9.61%. Hydropower generation is affected by the flood season, showing obvious seasonality, generally July to September is the flood period, the highest power generation, 1-3 months is the dry period, the lowest power generation。

The annual utilization hours of hydropower generation equipment on the mainland fluctuate in the range of 3000-3850. In the past few years, the average electricity price of hydropower has fluctuated in 0.25-0.30 yuan/kW time.

In terms of capital investment in hydropower and power sources, the peak of the past decade occurred in 2012/2013, both exceeding 120 billion yuan, and 90.5 billion/107.7 billion/98.8 billion yuan in 2019-2021, respectively, maintaining a high level. The hydropower installed capacity target for the 14th Five-Year Plan is expected to be announced in the "14th Five-Year Plan for Renewable Energy Development", and according to the characteristics of hydropower eco-friendliness, low cost and long investment and construction period, we expect it to maintain an annual investment scale of nearly 100 billion yuan.

3.3. Wind power + photovoltaic power generation: 1200GW in 2030 or for a more conservative target, wind power photovoltaic installed capacity may be exceeded ahead of schedule

However, it is worth noting that from the perspective of past development speed, the 1200GW of wind power and photovoltaic power installed capacity target in 2030 is a more conservative target, which is likely to be exceeded ahead of schedule. The reasons are: (1) Combined with the installed capacity at the end of 2021 and the target of 1200GW by the end of 2030, the compound annual growth rate from 2021 to 2030 is 7.34%. From the historical experience, from 2012 to 2021, the compound annual growth rate of wind power and photovoltaic power generation installed capacity was 28.4%, and the single-year growth rate was never less than 15%, which was much higher than 7.34%. (2) It is expected that the new scale of wind power and photovoltaics in 2022 will be about 50GW and 90GW, and the total installed capacity of wind power and photovoltaics will increase by 20.8% year-on-year, much higher than 7.34%.

It can be seen that the target of 1200GW in 2030 is more conservative. If the expected growth rate from 2021 to 2030 is adjusted to 12.00%, the installation target will be exceeded ahead of schedule in 2026.

According to the China Electricity Council, the new installed capacity of wind power and photovoltaics in 2022 will be about 50GW and 90GW, totaling 140GW. In 2021, the new installed capacity of wind power and photovoltaics will be 47GW and 53GW。 According to IRENA's calculations, the investment cost of photovoltaic power generation/onshore wind power/offshore wind power in the mainland in 2020 is about 4.1/8.0/18.8 yuan/W, while the ratio of onshore wind power to offshore wind installed capacity worldwide is about 20:1, and the wind power investment cost is weighted according to this proportion is about 8.5 yuan / W. If the wind power installed capacity investment and construction is 8.5 yuan / W, photovoltaic power generation is 4.1 yuan / W, then the scale of wind power and photovoltaic power generation investment and construction in 2021 will be 616.8 billion yuan, reaching 794 billion yuan in 2022, an increase of 28.7% year-on-year。

3.3.1. Distributed photovoltaics: The application of BIPV/BAPV will be accelerated in the implementation of green buildings and the promotion of the whole county

Different from thermal power, hydropower, etc., photovoltaic power generation can also take distributed power generation in addition to large-scale centralized power generation. In distributed photovoltaic power plants, the scheme of combining photovoltaic modules with buildings is called BIPV or BAPV. BIPV (Building IntegratedPhotovoltaic) refers to the integration of photovoltaic buildings, also known as "building materials" solar photovoltaic buildings. BAPV (Building AttachedPhotovoltaic) refers to photovoltaic power generation systems attached to buildings, also known as "installed" solar photovoltaic buildings.

BAPV is usually installed through a simple bracket, which can be retrofitted later, without changing the appearance of the building, and does not conflict with the original function of the building. BIPV has built photovoltaic modules into building materials in the early design, which has a higher integration process and usually a more concise and beautiful appearance.

In terms of market space, BIPV needs to be planned in the early stage of the building, generally applied in new buildings, and the potential space is very broad in the long run, but in the short term, it is limited by the number of new buildings and the construction cycle. BAPV can be used for the renovation of existing buildings, and the implementation difficulty is relatively low, which is suitable for the rapid development of distributed photovoltaic needs.

In terms of the main body of the order, BIPV undertakes the function of building materials itself, involving load-bearing, waterproof and other needs, building materials enterprises are relatively experienced, and the ability to obtain related orders is strong. BAPV is a relatively pure photovoltaic product, related projects are more dominated by photovoltaic companies, for construction companies, because it is only responsible for installation, the technical content and profit level are relatively low.

In terms of policy environment, the evaluation and promotion of green buildings continues, and we believe that they are expected to further accelerate under the dual-carbon strategy, which is conducive to BIPV and BAPV with the functions of reducing energy consumption and using renewable energy. In 2019, the Ministry of Housing and Urban-Rural Development issued a new version of the "Provisions on the Evaluation System for Green Buildings", which divides buildings into basic, three-star, two-star and one-star green buildings. Among them, the rational use of renewable energy and building energy consumption are all scoring items。

In 2020, the Ministry of Housing and Urban-Rural Development and other departments issued the "Action Plan for the Creation of Green Buildings", proposing that by 2022, the proportion of green building area in new urban buildings should reach 70%, and star-rated green buildings should continue to increase. 2022 The Ministry of Housing and Urban-Rural Development issued the "14th Five-Year Plan for the Development of the Construction Industry", which points out that green buildings should be fully implemented in government-invested projects and large-scale public buildings.

The steady progress of the county-wide pilot work will further accelerate the development of the BIPV and BAPV markets. In June 2021, the National Energy Administration issued the "Notice of the Comprehensive Department of the National Energy Administration on Submitting the Pilot Program for the Development of Distributed Photovoltaics on rooftops in whole counties (cities, districts)," requiring all regions to actively coordinate the implementation of roof resources and carry out development and construction in the form of whole districts, streets, towns, townships, etc., of which the proportion of photovoltaic power generation can be installed in the total area of the roofs of party and government organs is not less than 50%, the total area of photovoltaic power generation in public buildings such as schools and hospitals is not less than 40%, and the roofs of industrial and commercial plants The proportion of photovoltaic power generation that can be installed in the total area is not less than 30%, and the proportion of photovoltaic power generation that can be installed in the total area of rural residents' roofs is not less than 20%.

In September 2021, the National Energy Administration announced the first pilot list of 676 pilot counties (cities, districts). The State Energy Administration will evaluate and announce the development progress of the pilot areas in the previous year in the first quarter of each year.

3.3.2. Centralized photovoltaic: wind and solar bases have started construction one after another

In November 2021, the National Development and Reform Commission and the National Energy Administration issued the "Notice on the First List of Large-scale Wind Power and Photovoltaic Base Construction Projects Focusing on Desert, Gobi and Desert Areas", which plans the first batch of projects involving inner Mongolia Autonomous Region, Gansu Province, Shaanxi Province, Ningxia Autonomous Region and other places, with a total installed capacity of 97GW.

In February 2022, the National Development and Reform Commission and the National Energy Administration issued the "Planning and Layout Plan for Large-scale Wind Power photovoltaic Bases Focusing on Desert, Gobi and Desert Areas", planning the second batch of large-scale wind and photovoltaic bases with deserts and Gobi areas such as Kubuqi in Inner Mongolia as the key planning and construction of wind and photovoltaic bases, with an installed capacity of about 455GW by 2030, of which about 200GW of planning and construction tasks will be completed in the 14th Five-Year Plan. Both batches of projects require intensive development to avoid fragmentation, and the scale of the single project is not less than 1GW.

3.4. Nuclear power: The development of clean baseload power sources is expected to accelerate

Nuclear power is the use of nuclear fission reaction to release energy to generate electricity clean energy, does not produce carbon dioxide, the consumption of uranium fuel in addition to nuclear power has no other use, uranium reserves are sufficient, as a fuel cost is low, but the nuclear waste generated radioactive needs to be carefully handled. The mainland's nuclear power generation capacity continues to grow, from 62.1 billion kWh in 2007 to 407.5 billion kWh in 2021, a total increase of 5.56 times, with a compound annual growth rate of 13.04%. Because its production is not limited by the rhythm of natural resources, nuclear power can be used as a baseload power source for long-term stable operation, and the average annual utilization hours of nuclear power generation equipment in the mainland is maintained at more than 7,000.

The safety of nuclear power plants is of great concern to the public, especially after the nuclear accident in Fukushima, Japan, in 2011, when the nuclear accident in Fukushima, Japan, the attitude of the world to the development of nuclear power turned conservative, and the mainland also suspended the review of nuclear power projects for a time. Over the past many years, the mainland has steadily advanced the construction of nuclear power projects and made great progress in safety and technology.

Under the dual-carbon strategy, nuclear power, as a zero-emission baseload power source, has obvious advantages, and the policy orientation has become more active, and its development is expected to accelerate. The central government clearly mentioned in the 14th Five-Year Plan that the installed capacity of nuclear power operation should reach 70GW during the 14th Five-Year Plan. The installed nuclear power capacity of the mainland increased from 13GW in 2012 to 53GW in 2021, an increase of 3.24 times, with a compound annual growth rate of 13.94%. In order to achieve the 70GW target in 2025, the compound growth rate in 2021 and 2025 must reach 7.07%, which is far lower than the historical level, which shows that the target is also relatively conservative, and it is likely to be exceeded in advance.

In terms of investment, the amount of investment completed in the capital construction of nuclear power power was at a record high in 2010-2013, exceeding 60 billion yuan per year, and then declined, and has not exceeded 60 billion yuan in 2014, and 488/378/538 billion yuan in 2019-2021. We expect the annual investment completion to increase slightly in the range of 55-65 billion yuan during the remainder of the 14th Five-Year Plan period.

3.5. Hydrogen power generation: the economy needs to be improved

There are two main paths for hydrogen power generation: one is a hydrogen generator, using hydrogen as a fuel, using the principle of the internal combustion engine to drive the motor to generate current; the other is a fuel cell, using electrochemical reactions, the chemical energy is directly converted into electrical energy, and the power generation efficiency is higher. The by-products of the two paths of hydrogen power generation are only water, and the water generated can continue to produce hydrogen, which is a clean energy with zero carbon emissions. Hydrogen power generation also has the characteristics of on-off and stop-and-go, which can be used to regulate the power grid.

Hydrogen energy is a secondary energy source, hydrogen as an industrial gas has been used for a long time, can be produced through fossil energy hydrogen production, industrial by-product purification to hydrogen, electrolysis of water to hydrogen and other methods; among which fossil energy hydrogen production includes coal to hydrogen, natural gas reforming to hydrogen, petroleum hydrogen production. Hydrogen power generation is currently costly, according to Baichuan Yingfu information, the price of hydrogen has dropped recently, to about 2.55 yuan per cubic meter, hydrogen per kilogram about 11.2 cubic meters, fuel cells can produce about 15 degrees of electricity, then without considering the subsidy situation, the cost of electricity is still as high as 1.9 yuan, not yet economical.

The mainland is a big country of hydrogen energy, the continent currently has an annual output of about 33.42 million tons of hydrogen energy, ranking first in the world, and the installed capacity of electrolyzers is expected to reach 80GW by 2030, and the annual demand for hydrogen on the mainland is expected to increase to 130 million tons by 2060. Among the 130 million tons of hydrogen demand: industrial hydrogen is the largest, accounting for about 59.8%; followed by the transportation sector, accounting for about 31.1%; the construction sector accounts for 4.5%; power generation and grid balance account for 4.6%, hydrogen consumption of about 6 million tons, according to the current efficiency calculation can generate about 100 million kWh of electricity, accounting for a very small proportion of power generation. (Source: Future Think Tank)

3.6. Geothermal power generation: the base and growth rate are low

Geothermal power generation is a power generation technology that converts geothermal energy into mechanical energy and then converts mechanical energy into electrical energy, and is also a clean energy with zero carbon emissions. The specific way to achieve this is to send the hot steam from the ground into the steam turbine and promote the operation of the steam turbine to generate electrical energy, the principle is similar to that of thermal power.

The current application and development speed of geothermal energy is relatively limited. World geothermal energy production grew from 67.3 billion kWh in 2009 to 92 billion kWh in 2019, an increase of 36.80% and a compound annual growth rate of 3.18%. The installed capacity of geothermal energy in the mainland increased from 22MW in 2000 to 26MW in 2020, an increase of 19.82%, with a compound annual growth rate of 0.91%. Geothermal energy production has been stable at around 140 million kWh per year since 2010.

3.7. Energy storage: 14.28% of pumped storage capacity installed from 2020 to 2025, cagr 51.17% of new energy storage

Energy storage is a technology that stores energy through a medium or device for use when needed. With the continuous advancement of the dual-carbon strategy, the proportion of wind power and photovoltaic power generation in the mainland will continue to increase, and the importance of energy storage will also increase. Due to the strong rhythm of the natural energy sources on which wind and photovoltaic power generation rely, the use of energy storage technology can achieve peak regulation, reduce the impact of wind and photovoltaics on the power grid and abandon wind and light. There are many technical paths for energy storage, including pumped water storage, electrochemical energy storage, molten salt energy storage, compressed air energy storage, etc., of which electrochemical energy storage has lithium-ion batteries, lead-sulfur batteries, lead batteries and other forms.

In terms of installed capacity, according to cnESA statistics, by the end of 2020, the installed capacity of energy storage in operation worldwide reached 191.1GW, an increase of 3.4% year-on-year, of which water storage is the most important form of energy storage, with a scale of 172.5GW, accounting for 90.3%, and the scale of electrochemical energy storage is 14.2GW, accounting for 7.5%. Among electrochemical energy storage, lithium-ion batteries have the highest proportion of 13.1GW. In China, by the end of 2020, the installed capacity of energy storage has been put into operation by 35.6GW, an increase of 9.8% year-on-year, of which the installed capacity of pumped storage is 31.8GW, an increase of 4.9% year-on-year, and the installed capacity of electrochemical energy storage is 3.3GW, a year-on-year growth rate of 91.2%. Among electrochemical energy storage, lithium-ion batteries have the highest installed capacity, at 2.9GW.

In September 2021, the National Energy Administration issued the "Medium- and Long-term Development Plan for Pumped Storage (2021-2035)", which set a target of 62GW of pumped storage production by 2025 and 120GW by 2030, and reserved 247 projects with a total of 305GW. In October 2021, the State Council issued the "Carbon Peak Action Plan by 2030", proposing the target of 30GW of installed capacity of new energy storage in 2025 and 120GW in 2030. According to the target, the installed capacity of pumped storage will grow at a compound growth rate of 14.28% from 2020 to 2025 and a compound growth rate of 14.12% from 2025 to 2030. The new energy storage, that is, the form of energy storage other than pumped storage, can be achieved from its target of a compound growth rate of 51.17% in installed capacity from 2020 to 2025 and a compound growth rate of 31.95% from 2025 to 2030.

3.8. UHV: The State Grid plans to invest 380 billion yuan during the 14th Five-Year Plan period

The voltage level of the mainland is generally divided into safe voltage, low voltage, high voltage, ultra high voltage, and ultra high voltage. Among them, ultra-high voltage refers to the transmission technology of AC voltage greater than or equal to 1000KV, DC voltage greater than or equal to ± 800KV. The higher the voltage of the power grid, the less losses in its transmission process, and the higher the efficiency of transmitting electrical energy. The farther the transmission distance, the higher the applicable grid voltage. With the continuous deepening of the development of wind and photovoltaics in the western part of the mainland, the demand for transmission will also increase day by day, which will lead to the construction process of UHV power grids. In 2020, 22 UHV lines on the mainland transported a total of 531.8 billion kWh of electricity, 18 of which were operated by its home grids in China, transporting 455.9 billion kWh, and 4 by the Southern Power Grid, which transported 759 kWh.

The amount of capital investment completed in the mainland power grid has been in the range of 400 billion to 550 billion yuan per year since 2014. In terms of UHV, the scale of investment in the UHV industry in the mainland in 2018/2019 was 63.8 billion yuan/55.3 billion yuan, respectively, and the investment directions included basic civil engineering and transmission hardware equipment, of which transmission hardware equipment included towers, cables and converter stations.

According to China Energy News, the State Grid plans to build 24 ALTERNating Current UHV projects and 14 DC UHV projects during the 14th Five-Year Plan period, involving more than 30,000 kilometers of lines and a total investment of 380 billion yuan. According to the "14th Five-Year Plan for the Development of the 14th Five-Year Plan for the Power Grid" issued by China Southern Power Grid, during the 14th Five-Year Plan period, China Southern Power Grid will invest about 670 billion yuan, of which 320 billion yuan will be used for the construction of the distribution network, without mentioning the large-scale investment planning of UHV projects.

4. Green power construction sector: both growth space and certainty, showing the value of investment

As an important starting point for carbon peaking work, green electricity will be vigorously developed during the 14th Five-Year Plan period, and the construction projects of green power generation equipment, energy storage and power grid will be rapidly advanced, and the green power construction sector is expected to usher in a broad space for growth. Green power construction enterprises with a complete green power project survey and design, construction technology and service system will benefit from it in an all-round way.

4.1. In the integrated transformation of green power investment and construction of construction enterprises, it is expected to improve the level of corporate profitability

4.1.1. The green power business has stronger scientific and technological attributes and higher profit margins

The traditional engineering construction business is limited by factors such as mature technology and intensive labor costs, and the business threshold is low and the profitability is limited. The technical content of green power construction business has been improved compared with that of traditional engineering construction business. Especially with the deepening of the reform of the power system, the current green power construction enterprises are no longer limited to the construction mode of the project delivered to the owners after the completion of the construction, but actively participate in the investment, construction and operation of green power.

The business of power investment and operation is generally better than the engineering construction business in terms of profitability and cash flow health, and the financial performance of enterprises is expected to be optimized. After the integrated operation of investment and construction, enterprises are also expected to further exert the advantages of industrial chain coordination and further improve construction costs, operation and maintenance costs, and technical optimization.

From the perspective of R&D investment, it can be seen that the scientific and technological content of the green power construction sector is actually not lower than that of many traditional science and technology companies. Taking China Power Construction as an example, its R&D expenses in 2018/2019/2020 were 92.5/112.9/15.27 billion yuan, accounting for 3.1%/3.2%/3.8% of operating income, respectively, and the R&D rate has been higher than 3%, and the amount and expense rate have shown an upward trend. In 2018/2019/2020, China Energy Construction's R&D expenses were 40.0/55.1/6.78 billion yuan, accounting for 1.8%/2.2%/2.5% of operating income, respectively, and the amount and rate also showed an upward trend.

At the end of 2021, China Energy Construction Investment set up a wholly-owned subsidiary, ZhongnengJian Digital Technology Group Co., Ltd. and Zhongneng Construction Hydrogen Energy Development Co., Ltd., which shows that the company attaches great importance to digitalization and new energy technology investment.

4.1.2. The green electricity market is relatively concentrated, and green power construction enterprises are expected to enjoy a high share

In recent years, the share of central enterprises in the construction engineering industry has increased, but the industry as a whole is still relatively scattered and the concentration is relatively low, while the business of the green power construction sector is relatively more concentrated. Take the installed capacity targets of China Power Construction and China Energy Construction during the 14th Five-Year Plan period as an example: the new energy installed capacity target during the 14th Five-Year Plan period of China Power Construction is 30-48.5GW, and the 14th Five-Year Plan target of China Power Construction is to hold more than 20GW of installed capacity, and the total of the two is 50-68.5GW.

In the remaining period of the 14th Five-Year Plan, according to the above 6% installed capacity growth assumption (corresponding to 1200GW in 2030) and 12% installed capacity growth assumption (corresponding to the 1200GW target exceeded in 2026), the new installed capacity of the 14th Five-Year Plan was 307GW and 463GW, respectively. Assuming that the new installed capacity during the 14th Five-Year Plan period is within the above range, and the 14th Five-Year Plan targets of China Power Construction and China Energy Construction can be achieved, its market share is 10.8%-18.4%, which is much higher than that of traditional construction engineering business.

4.1.3. Order Situation: Green Power Construction Relay Real Estate drives business growth

Under the background of the end of China's urbanization process and the regulation of housing and housing, the overall prosperity of the real estate industry is sluggish, and the capital chain of some real estate developers is broken. As the upstream of real estate developers, the orders and payment collections of the building decoration sector have inevitably been affected to a certain extent. However, from the perspective of the total amount of investment in fixed assets, the total amount of investment has not been reduced, and it is more of a structural change.

Therefore, grasping the opportunity of the times, smoothly transforming new infrastructure, green power investment and construction of construction enterprises is expected to continue a longer-term stable growth. According to the announcement of China Energy Construction's 2021 annual operating data, the new contract amount of its engineering construction business was 800.89 billion yuan, an increase of 45.7% year-on-year. Among them, the urban construction business (including municipal, housing construction, real estate development, etc.) signed a new contract amount of 167.91 billion yuan, an increase of 11.3% year-on-year. The new contracts signed for the new energy and smart energy business were 192.77 billion yuan, an increase of 53.2% year-on-year, and the growth rate was significantly higher than that of the urban construction business. In 2021, the newly signed contracts of China Power Construction were 780.28 billion yuan, an increase of 15.9% year-on-year, of which the new contracts signed for water conservancy and power business were 310.38 billion yuan, an increase of 46.6% year-on-year.

4.2. The valuation level of the green power construction sector is low, and it is expected to usher in the Davis double-click

4.2.1. Comparison of Green Electronics Sections: The construction and construction + operation sub-sector has a low valuation and is expected to be repaired in 2022

The green electricity sector as a whole has experienced a large increase in 2021, and there is a certain correction in early 2022, we believe that the current market sentiment has been fully released, and the prosperity in 2022 is expected to continue. However, there are currently large differences in valuations between sub-sectors of Green Power. For the construction sector, the valuation level of Guangdong Hydropower is relatively low, as a regional water conservancy and hydropower leader, its performance growth is stable, the orders in hand are sufficient, and it has a certain first-mover advantage in hydrogen energy investment, we expect it to maintain steady performance growth in 2022, and is expected to usher in valuation repair.

For the construction + operation sector, its valuation level is relatively low, especially China Power Construction and China Energy Construction, PE is less than 16 times, PB is less than 1.4 times, significantly lower than other green power construction targets and green power operation targets. We believe that part of the reason for this is that China Power Construction and China Energy Construction still have a relatively large proportion of the traditional engineering construction business, which is a low valuation given by the market due to limited growth and a high level of capital occupation, which has a certain drag on the company's overall valuation. On the other hand, because the business of China Power Construction and China Energy Construction is more diversified and the complexity is relatively high, especially the market is not expected to have sufficient results in their transformation of green power investment-construction-operation integration manufacturers, there is a certain discount in pricing.

We believe that the industry environment in 2022 is more optimistic, with the excellent resources and technical capabilities of enterprises, it is expected to fully release the synergistic advantages of the industrial chain, achieve good performance growth, thereby eliminating market doubts, and further promoting valuation repair and realizing Davis double-click.

4.2.2. The holding of green power assets forms an effective support for the market value

According to IRENA's statistics, the investment cost of photovoltaic power generation/onshore wind power/offshore wind power in 2020 is about 4.1/8.0/18.8 yuan/W. In terms of hydropower, based on the above-mentioned completion of investment in hydropower power infrastructure from 2018 to 2020 and the increase in installed hydropower capacity, we roughly measured that the cost of hydropower investment is about 9.2 yuan / W. Taking China Power Construction as an example, according to the company's disclosure, by the middle of 2021, its holding installed capacity has been put into production of 16.4GW, and hydropower and new energy account for 80.71%, that is, 13.2GW. Among them, photovoltaic power generation is 1.45GW, wind power is 6.36GW, and if the remaining part is hydropower, then hydropower is 5.43GW. Since the company does not disclose the proportion of onshore wind power and offshore wind power in the installed wind capacity it holds, we conservatively assume that it is all onshore wind power with lower investment costs. Therefore, in terms of replacement costs, the original value of each GW of photovoltaic power generation/wind power/hydropower installed capacity is 9.2 billion/8 billion/4.1 billion yuan, respectively. Assuming that it has been depreciated by 10%, the above green power assets are now worth 96.073 billion yuan, which has formed a very effective support for its market value.

4.2.3. 2022 is the final year of the three-year reform of state-owned enterprises, and the integration and optimization of state-owned assets is expected to accelerate

Most of the green power construction enterprises are state-owned enterprises. Previously, the holding companies of a number of listed companies in the building decoration sector had clearly stated when they were restructuring that if they constituted substantial competition or conflicts of interest in the main business in the future, they would abandon the opportunity to compete in the same industry or inject related business into the listed company.

For example, when Poly Group reorganized with China Haicheng's controlling shareholder, China Light Group, and Shandong Highway Group, the controlling shareholder of Shandong Luqiao, jointly reorganized with Qilu Transportation Development Group, they all made commitments to avoid competition in the same industry. On the one hand, the injection of assets can reduce disorderly competition and effectively release business synergies, on the other hand, it can help listed companies accelerate industrial transformation and upgrading, which is expected to significantly improve asset quality and profitability.

A few days ago, China Power Construction Holding Shareholder Power Construction Group completed asset replacement with China Power Construction in accordance with the commitment to avoid competition in the same industry, and China Power Construction has placed a sluggish real estate business and placed 18 high-quality power grid auxiliary assets, and the profitability of the placed assets is higher than that of the assets disposed, which is expected to increase the company's earnings. The controlling shareholder of China Power Construction still has assets that compete with the company in the same industry, and we expect to inject them in the future under conditions favorable to the listed entities.

2022 is the last year of the three-year action of state-owned enterprise reform, and it is also the year of decisive victory, and we expect that the work of resource integration between the State-owned Assets Supervision and Administration Commission, central enterprises and state-owned enterprises will be accelerated. In the future, if the assets of Green Power Construction Company are further optimized, it may become a powerful catalyst for the comprehensive repair of plate valuations.

5. Analysis of key companies

5.1. PowerChina

A big country heavy equipment, hydropower construction is the world's first。 The company, formerly known as Sinohydro, was jointly established in 2009 by China Water Resources and Hydropower Construction Group Corporation and China Hydropower Engineering Consulting Group Corporation, and was renamed China Power Construction in 2014. In the national ecological environmental protection and the development of green energy strategy, the company has played the role of the pillar of the heavy equipment of a big country. The company's integration ability and performance of water conservancy and power construction rank first in the world, undertakes more than 80% of the planning and design tasks of domestic large and medium-sized hydropower stations, more than 65% of the construction business, occupies more than 50% of the world's large and medium-sized water conservancy and hydropower construction market, and is the main compilation and revision unit of China's water conservancy and hydropower, wind power, and photovoltaic construction technical standards and regulations.

The operation is stable and progressive, and the performance exceeds the plan. The company's 2020 annual report plans for 2021 are operating income of 446.26 billion yuan in 2021, new contracts of 747 billion yuan, and investment of 173.715 billion yuan. In 2021, the actual amount of newly signed contracts was about 780.283 billion yuan, an increase of 15.91% year-on-year, exceeding the previously disclosed business plan. Among them, the newly signed contracts for water conservancy and power business amounted to about 310.381 billion yuan. By the end of the third quarter of 2021, the company achieved operating income of 336.098 billion yuan, an increase of 22.25% year-on-year, and the increase was also higher than the annual business plan, and the net profit attributable to the mother was 6.356 billion yuan, an increase of 7.69% year-on-year. The company's operation is stable, the indicators are stable and progressive, and the development trend is good.

Assets continue to be optimized, and profitability is expected to increase. Recently, the company's controlling shareholder, Power Construction Group, placed 18 outstanding power grid auxiliary assets into the company according to its previous commitment to avoid competition in the same industry, and the company disposed of 3 companies, China Power Construction Real Estate Group Limited, Beijing Feiyue Linkong Technology Industry Development Co., Ltd., and Tianjin Haifu Real Estate Development Co., Ltd. For the company, the overall profitability of the assets placed in this asset replacement is usually higher than that of the assets sold, and the company's future profitability is expected to increase. At present, there are still 3 enterprises under the Power Construction Group that compete with the company in the same industry, but due to defective ownership and other matters, they do not have the conditions to inject into the listed entity. Power Construction Group has now entrusted these three companies to the company, and promised to actively promote their eligibility and complete the asset injection in the future. If more high-quality assets are injected in the future, the company's profitability is expected to further improve.

Focus on clean and low-carbon energy and electricity, and continue to promote transformation and upgrading。 The company has a complete survey, design and construction, operation and new technology system of hydropower, thermal power, wind power and photovoltaic power generation projects, and focuses more on clean and low-carbon energy and power business, and continues to exert efforts on investment and operation. With the mission of "building clean energy, creating a green environment, and serving a smart city", the company gives full play to the company's core advantages of "understanding water and familiarizing electricity", "being able to invest in operation" and the integration of the industrial chain, and vigorously invests in the development of a modern power system based on new energy. In 2021, the company issued guidelines for new energy investment business, proposing a target of 30-48.5GW of new installed capacity during the 14th Five-Year Plan period. By the middle of 2021, the installed power capacity of the company's holding has reached 16.4GW, of which hydropower and new energy account for 80.71%. (Source: Future Think Tank)

5.2. China Energy Construction

World-class energy integration solution provider. Founded in 2014, the company was jointly initiated by China Energy Construction Group Co., Ltd. and its wholly-owned subsidiary, Power Planning Institute Co., Ltd., and was listed on the Hong Kong Stock Exchange in 2015 and on the Shanghai Stock Exchange in 2021. The company provides holistic solutions for China's and even global energy, power, infrastructure and other industries, with operations in more than 140 countries and regions. By the end of 2020, the company has 10,000+ valid patents, 1100+ national standards and industry standards, and has played the main role in a series of major projects such as the Three Gorges Project and the South-to-North Water Diversion Project, and has undertaken the world's first "three hundred" thermal power project, the world's first AP1000, CAP1400 nuclear power project, the world's largest wind and solar storage and transportation project and many other world firsts.

The performance is eye-catching, and the new energy orders are high. In the first three quarters of 2021, the company achieved operating income of 209.59 billion yuan, an increase of 21.8% year-on-year, and net profit attributable to the mother of 3.361 billion yuan, an increase of 69.05% year-on-year, all of which achieved high growth. The company's new contracts signed in 2021 were 872.61 billion yuan, an increase of 51% year-on-year, and various businesses were in full bloom. Among them, the new contracts signed for new energy and integrated smart energy business were 192.77 billion yuan, an increase of 53.2% year-on-year, and the new contracts signed for traditional energy business were 201.88 billion yuan, an increase of 21.7% year-on-year. From a sub-regional point of view, the number of new signatures in china for the whole year was 655.46 billion yuan, an increase of 64.2% year-on-year, and the number of new signatures signed overseas for the whole year was 217.15 billion yuan, an increase of 21.6% year-on-year.

Comprehensively enter the new energy industry and help optimize the energy structure. The company regards the clean energy business as the core business of the energy integration solution, and is committed to becoming a first-class comprehensive management provider of ecological environment. The company's clean energy business includes clean and efficient thermal power, hydropower, wind power, photovoltaic, solar thermal, biomass power generation and other power generation investment, construction and operation, and has developed a number of clean energy projects in many places in China, Vietnam and Pakistan. By the end of 2020, the company will have an installed capacity of 2.9GW, an installed capacity of 2.0GW under construction, and a water treatment capacity of 3.36 million tons per day.

5.3. Guangdong Hydropower

Regional water conservancy and hydropower project leader, steady performance growth. The company is a leading enterprise in the construction of water conservancy and hydropower projects in Guangdong Province, with special qualifications for general contracting of water conservancy and hydropower projects, and has a high brand influence in the whole country, especially in Guangdong, Sichuan, Hunan and other regions. In the rail transit business, the company has a number of key construction technologies and 18 shield machines, and is deeply involved in the construction of rail transit in Guangzhou and the Pearl River Delta. The company's 2021 revenue is expected to be 14.304 billion yuan, an increase of 13.67% year-on-year, and the net profit attributable to the mother is 320 million yuan, an increase of 21.43% year-on-year. By the end of 2021, the company has signed a total of 248 unfinished project construction projects, with an amount of 26.383 billion yuan, and sufficient orders in hand.

Firmly develop clean energy power generation, focusing on breaking through the difficulty of hydrogen energy。 The company unswervingly promotes the clean energy power generation business, insists on becoming stronger and larger, is the largest installed capacity of clean energy power generation in Guangdong Province, the most developable resources of the enterprise, wind power tower manufacturing business is also the first echelon in China. By the middle of 2021, the company has put into operation a new energy project with a total installed capacity of 1.5GW. Recently, the company and Inner Mongolia Wuhai Municipal Government, Xingbang Technology reached a strategic cooperation, jointly invest in the hydrogen power industry chain, set up an international academician future zero carbon hydrogen energy science and technology innovation center, 2 carbon neutral hydrogen power industrial park, to create upstream, middle and downstream 3 industrial clusters, the total investment is expected to be 16.8-188 billion yuan, is expected to form 10,000 (sets) of hydrogen fuel cell modules, hydrogen fuel cell heavy trucks and bus sanitation vehicles and other applications, and form to meet the needs of 10,000 hydrogen fuel tank vehicles, hydrogenation supply service capabilities.

(This article is for informational purposes only and does not represent any of our investment advice.) For usage information, see the original report. )

Featured report source: [Future Think Tank]. Future Think Tank - Official website