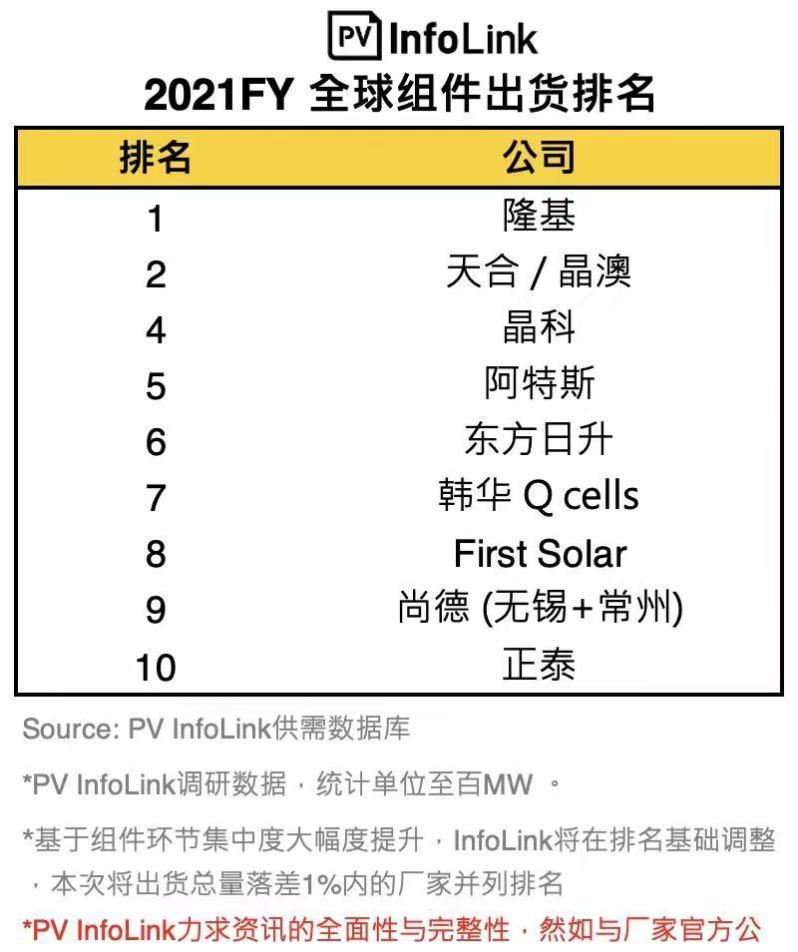

PV InfoLink, a third-party market research and consulting organization in the photovoltaic field, released the latest 2021 global module shipment rankings, showing that among the top 10 PV module suppliers, Chinese companies occupy eight seats and occupy the top six. According to the statistics of InfoLink supply and demand database, after LONGi stood on the first place in the list in 2020, it continued to sit on the first place in 2021, and it is estimated that its total shipments of domestic and foreign components far exceeded the second place by more than 10GW.

Due to the significant increase in the concentration of component links in 2021, the list will rank manufacturers within 1% of the total shipment gap, and the second is Trina and JA Ao. Jinko ranked fourth, followed by Canadian Solar, Risen Risen, Hanwha Q-Cells, First Solar, Suntech and Chint.

InfoLink's 2021 Global Component Shipment Rankings are available

There is no suspense in the "Global Component Shipment Ranking" of Chinese companies. Photovoltaic industry media PV Tech also recently announced the top ten global module suppliers in 2021, which is basically consistent with infoLink's ranking, but there is a disagreement on the seventh to ninth places.

PV Tech 2021 Global Top 10 PV Module Suppliers Ranking

With the strong growth of the global photovoltaic power generation industry, the corresponding magnitude of the list has jumped significantly. The surging news noted that 10 years ago, when a company's annual module shipments exceeded 1GW, it could rank among the top ten, and now, the basic module shipments of TOP5 manufacturers are more than 10GW.

From the specific ranking, the TOP 10 shippers in 2021 are basically the same as in 2020. The biggest change is JinkoSolar, which ranked second in global module shipments in 2020 and fourth in 2021. This is related to its temporary adjustment of product sales strategy in the industrial chain price increase tide in order to stabilize profits, JinkoSolar mentioned in the prospectus that due to the rising price of silicon materials and other reasons, in the first half of 2021, the company strategically reduced the acquisition and execution of low-cost component orders, negotiated with customers for low-priced orders, negotiated to extend the delivery time, and increased the external sales of silicon wafers and cells according to market supply and demand and price conditions.

In 2021, the shipment volume of manufacturers ranked after the TOP10 fell at the level of 3-4GW, showing that the differentiation between manufacturers has increased significantly. InfoLink analysis said that from the trend of 2021, the component link still has a high degree of concentration, vertical integration of manufacturers with their own body, cost advantages, overseas channels to suppress the second- and third-line component manufacturers, InfoLink statistical table TOP 10 module shipments of about 160GW+, the estimated proportion of the annual component demand of 172.6GW calculation, far beyond the previous 7-80% share, the market share of more than 90%. Among them, the proportion of dismantling overseas shipments is observed, the advantages of vertical integration manufacturers in the distribution channel layout are obvious, and the proportion of areas with high overseas price acceptance in the second half of the year has increased significantly, and the proportion of Chinese manufacturers in the TOP10 has reached 70% of overseas shipments throughout the year.

In terms of size, InfoLink statistics TOP10 manufacturers (excluding First Solar) large-size shipments fell above 60GW, of which the second half of the year compared to the first half of the double growth, large size accounted for the annual TOP10 manufacturers total shipments (excluding First Solar) about 40%, has become the current mainstream specifications.

The agency believes that the trend of high concentration is bound to make it more difficult for small and medium-sized component manufacturers to survive. Looking forward to the follow-up component link to follow the expansion of N-type, some manufacturers still have a large number of battery and module expansion plans, and it is not ruled out that in the second half of the year, in the case of competing for market ownership, the price competition will repeat itself. Coupled with the impact of raw material shortage, small and medium-sized component manufacturers still have to face the test of market share division, sluggish start-up and profit.