2021 has passed, in the face of the new 2022, where will the global game industry go?

Recently, Google Games released a "Beyond 2021" report on Newzoo to try to answer this question. The report conducts extensive market and consumer research in 16 countries across four regions of the world, spanning the past 18 months.

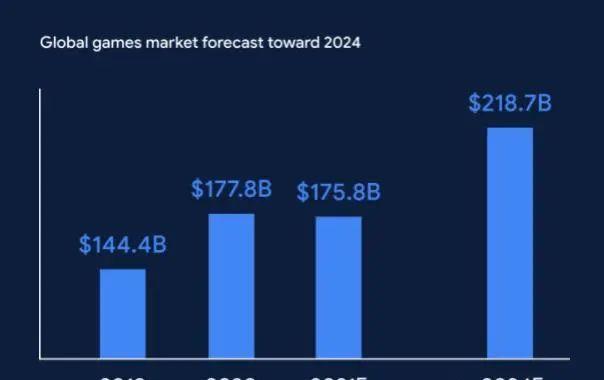

An overview of the overall situation of the global gaming market

According to the report, the global gaming market revenue reached $177.8 billion in 2020, an increase of 23.1% year-on-year, the highest in the past decade. By 2021, however, global markets are expected to experience their first historic decline. The real breakthrough point may come in 2023, when the global game market will enter the threshold of $200 billion, and reach $218.7 billion in 2024.

By the end of 2021, nearly 3 billion players worldwide had spent a total of $175.8 billion on games. Of these, 20 percent of revenue growth was contributed by new players who joined the game in 2020 or later, while the remaining 80 percent were made up of veteran players who had already played the game before 2020.

It is worth mentioning that the Asian region ranks first in the world with 1.615 billion players, accounting for 54%. In the new player growth indicator, the Middle East and Africa region ranked first in the world with a growth rate of 10.1%, 3.9% higher than the second-place Latin America.

From the perspective of growth factors, most of the growth in the past year has come from the increase in the free time of old players. The data shows that 30% of older players play the same number of games as ever, while 42% of older players play more games than ever before.

Among new players, the data shows that 173 million new or returning players participated in the game in 2020. Of these, 53% of new or returned players are women. Overall, 73% of new or returning players are more willing than ever to spend money on games.

Research shows that topics that have sparked discussion in the gaming world in the past will continue to play a key role in shaping the global gaming landscape beyond 2021. Divided in terms of influence, this can be divided into three categories: new trends, accelerating trends, and temporary setbacks.

New trends include games as social platforms and meta-universe application platforms, as well as subscription systems will be used on a large scale, while among the accelerating trends, social, cloud technology and decentralized platform awards have been significantly developed during the epidemic in the new museum. At the same time, the epidemic has also reduced the market revenue of many 3APC/console games as the core, and the development progress of many games has also been delayed.

In terms of continued market development, although 26% of new players/returning players and 18% of old players said they would reduce their games after the pandemic, 65%-70% of new players and returning players still plan to participate in the game at the same or higher level as in the past. In addition, more than 30% of players expressed their desire to further increase their spending on live streaming and esports.

Latin America: Live streaming and esports have great potential

From 2015 to 2024, Latin America is one of the fastest growing regions in the world for gaming audiences. Although the region will account for only 4% of global gaming market revenue in 2021, it ranks second globally in terms of player spending growth (2015-2024).

In 2021, 289.3 million Latin American gamers will spend a total of $7.2 billion on games, of which mobile games account for 48%, console games account for 27%, and PC games account for 25%.

The average age of Latin American players is 34, the youngest of the four regions of the world. It has a higher percentage of new or returning players compared to more mature regions such as North America, which account for 21% of the total number of players.

Mobile gaming is making a new splash in Latin America, such as live streaming and esports. The data shows that Latin American players have set new records for the number of people watching live streams and esports. By 2024, the number of viewers watching live broadcasts in Latin America is expected to increase to 122.4 million, and esports enthusiasts will add 25.3 million.

While Latin American gamers have seen a significant increase over the past 18 months, gamer growth across all platforms is expected to slow in the second half of 2021 and beyond, with only 8% growth expected between 2020 and 2021. Given the low level of payment by players in the region, gamers should explore more effective ways to increase audiences and revenue.

Interestingly, from 2020 to 2021, the number of players who paid to use cloud gaming services increased significantly by 6 times to 1.2 million players, contributing a total of $37.6 million in revenue.

North America: Focus on player engagement and innovative growth in the mobile gaming market

As a mature market, North America's revenue performance has reached a very high level. According to the data, as of 2021, 212.1 million players in North America have spent a total of $42.6 billion on games, of which consoles are the main platforms. As in most regions, the mobile gaming market in North America saw tremendous growth, increasing its share of revenue to $16.1 billion.

A study of North American gamers found that 83 percent of respondents were already involved in gaming by 2020, the largest percentage of any region surveyed. Another 13% are returning players and the remaining 4% are new players. The largest percentage of players in the range is over 45 years old.

Over the past 18 months, gaming has become the second most popular form of digital social networking in 2020, after traditional social media. At the same time, the number of players meeting in the game or through game-related platforms has not been less than the number of people using video conferencing software.

In mature regions like North America, large-scale social and metaversonic factors are rapidly normalizing. The opportunity lies in how to further integrate gaming with social media and streaming platforms.

Since most North American gamers are already mobile gamers, opportunities for player growth are limited, but revenue will continue to grow. The total number of mobile gamers in North America is expected to grow to 199 million at a CAGR of 0.8% by 2024, and revenue will grow at a compound annual growth rate (CAGR) of 6.4%, helping developers try out novel monetization strategies, explore cross-gaming, and expand beyond mobile audiences.

In terms of live broadcasting, the number of North American live viewers will grow to 91.5 million in 2021, accounting for nearly 13% of the global audience. In 2020, the consumption of game-related content grew by just over 40% and is expected to grow by another 39% in the future. With the growing popularity of mobile games and the push of social networking for live broadcasting, the live streaming and esports markets are expected to continue to soar in the future.

Europe, Middle East and Africa (EMEA): Markets are very different and opportunities are not the same

EMEA is the most diverse gaming region in the world, with some markets showing strong growth potential while others have extremely high average user revenues.

Of the world's top 10 gaming markets, Europe alone occupies four seats (Germany, the United Kingdom, France, and Italy), while the Middle East includes some of the most promising growth markets. As for Africa, the game has not yet gained mainstream status here.

In 2021, EMEA's 842.9 million players are expected to spend $37.8 billion on games. As of 2021, console games remain the largest segment, accounting for 45% and generating $17.2 billion in revenue, but mobile games are in the first place with a growth rate of 4%.

Compared to their counterparts in other regions, EMEA players tend to have less play time, averaging 2.3 hours less per week than North American players, 3.2 hours less than Latin American players, and 5 hours less than Asian players.

Even though many EMEA players expect their in-game activity to decline after 2021, the data shows that their playing time is still higher than before 2020. What's more, flexible spending habits mean that the opportunities for future revenue generation in the EMEA region are still high, and even if players don't want to invest too much time in the game, many people are still willing to spend money on the game.

The EMEA region has a rich market diversity, such as Western Europe is dominated by consoles, Eastern Europe is dominated by PCs, and the market in developing countries is dominated by mobile games.

Studies have shown that European gamers spend less total time on games than their peers in the Middle East and Africa and are more likely to be further reduced after the pandemic. However, their interest in live gaming and esports is more aligned with other regions, with major European markets such as Poland and the UK expecting their consumption to grow by 30% and 25% respectively from 2020.

Asia Pacific: The largest gaming market and the most important standard setter

The importance of the Asia-Pacific region is already evident. As the most important growth engine for the global gaming industry, the Asia-Pacific region has a rich regional diversity, as well as a fast-growing user market, and various innovations have also taken root here.

The data shows that the Asia-Pacific region has 55% of the world's players, as well as the three most important consumer spending markets (Chinese mainland, Japan and South Korea). Almost all of the 1.62 billion players in the Asia-Pacific region play on mobile devices. In 2021, Asia-Pacific players spent $57.9 billion on mobile games, accounting for two-thirds of all consumer spending in the region.

The study found that players in the Asia-Pacific region had the highest average weekly play time of 17.4 hours, driven by younger audiences in growth markets such as Vietnam and India, and a relatively low average age of 34.3 years.

For many years, games in the Asia-Pacific market have been dominated by multiplayer social networking, which has also set a global standard for the social capabilities of games around the world. This convergence of gaming and social takes place at the business and operational levels, and companies such as Tencent have been pushing the boundaries between gaming and social over the years, making the market aware of the potential of social networking in the region. The Asia-Pacific region may be better suited to the primordial metaverse than other regions.

Although console games have not yet gained popularity in the Asia-Pacific region, market indicators indicate that console players in the region have grown significantly due to the mobile-friendly features of the Nintendo Switch, as well as the PlayStation 5 and Xbox One consoles launched by Sony and Microsoft in Chinese mainland, and are still expected to increase by 21% in 2021 and beyond.

Mobile gaming activity in the Asia-Pacific region has continued to increase over the past 18 months. Although 97% of APAC players are already playing on mobile devices, engagement per player continues to grow. Since 2020, the region's players' activity in mobile games has increased by 46%, and it is expected that there will still be a 19% increase in the future.

In addition, mobile games also account for a large part of consumer spending in the region, which has led to fierce competition among game manufacturers and market-oriented innovation. From game items to battle passes, mobile gamers in the Asia-Pacific region have spent their money on more diverse game consumption than players in other regions.

····· End ·····

GameLook Daily Game Industry Report

Global vision / depth is material