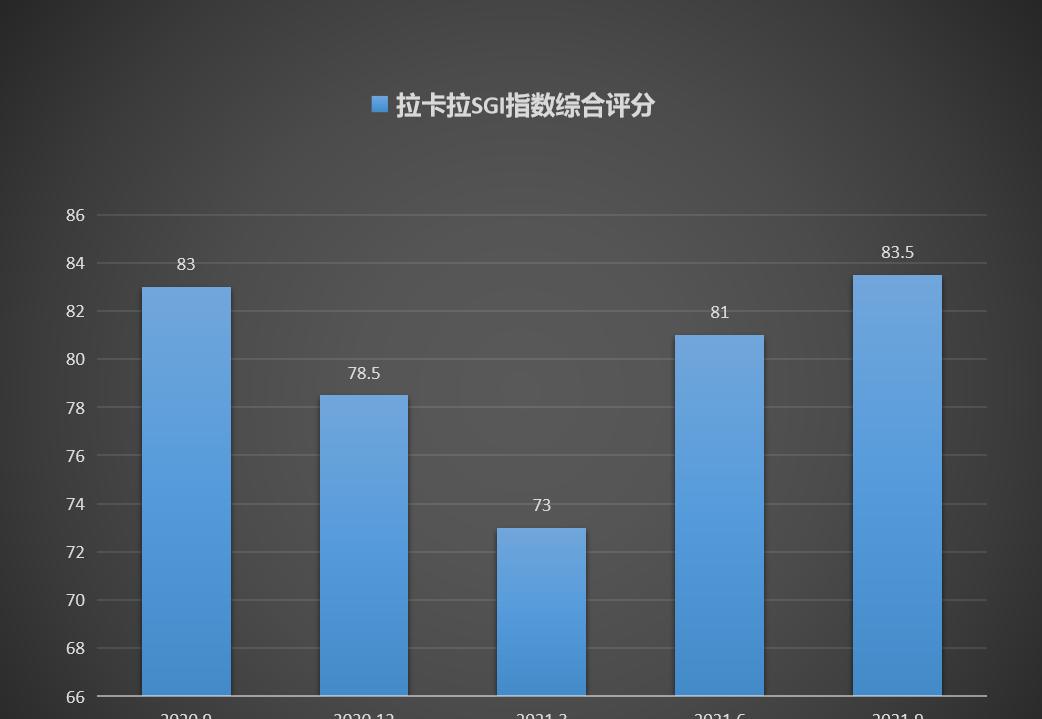

On October 28, the latest SGI score of Lakala Payment Co., Ltd. (hereinafter referred to as "Lakala") was released, and the company received a score of 83.5. Compared with the previous two quarters, the rebound is obvious, and the recent development situation has improved.

According to the third quarterly report, Lacala's operating income was 1.643 billion, an increase of 1.82% year-on-year during the reporting period, an increase of 19.88% from the beginning of the year to the end of the reporting period, an increase of 19.88% from the beginning of the year to the end of the reporting period, an increase of 1.85% over the same period of the previous year, an increase of 11.25% during the reporting period, and an increase of 5% from the beginning of the year to the end of the reporting period compared with the same period of the previous year.

Founded in 2005, Lakala is one of the first third-party payment enterprises in China to obtain a license from the central bank, which was originally mainly provided through "online + offline" and "hardware + software" forms of personal payment, merchant acquiring and derivative services. In 2015 and 2016, the payment business experienced explosive growth, but the good times did not last long and entered a bottleneck period. As shown in the chart below, La Cala's gross profit margin has repeatedly declined, from 40.36% in the same period last year to 34.8%, and the net profit margin is also hovering at 167%.

It is understood that Lakala is constantly exploring new business growth models, during the reporting period, Lacala accounts receivable of 933 million yuan, an increase of 114% year-on-year, the company said it is to carry out supply chain finance business caused.

La Cala has focused on expanding ka merchants and waist merchants this year, and the digital yuan has become a stepping stone for its expansion of ka merchants. Through digital yuan, Lakala has established cooperation with large supermarkets such as Bailian and Wumart and some 5a scenic spots. It is revealed that the digital yuan has entered the B2B business, the demand in this field is strong, and the entire transaction scale can reach more than 50 trillion yuan, and there is a lot of room for imagination in the future.

At present, there are two major categories of Lakala business: merchant payment business and merchant technology service business. In the merchant payment business, institutional and individual investors pay more attention to the business progress of mobile phone pos and the layout of cross-border business. In addition, Lakala has built five saas technology platforms of "payment, finance, cross-border, supply chain, and topping". Among them, the financial technology saas service platform achieved revenue of 210 million yuan; computer software technology services received 2.2 million yuan, mainly from the cloud store, cloud acquiring, money account and other payment + saas product income.

However, in the past year, Lacala's stock price has fallen and fallen, from the highest level of 42.73 yuan to 23.5 yuan now, almost waist-cutting, the latest data show that Lacala's stock price has fallen for seven consecutive days. From the secondary market point of view, investors hold negative investment sentiment towards Lakala and are not optimistic about the company's prospects.

In addition, Lakala's investment in research and development has been below 5%, and the proportion of R&D investment in operating income in the third quarter was 3.73%, which was relatively low and had a downward trend.