Ruan Runsheng / Charting Worm Creative / Courtesy of Peng Chunxia / Cartography

Securities Times reporter Ruan Runsheng

The third quarter is the traditional peak season of the electronics industry, but the fear of weak downstream market demand this year has always hung over the entire industry, and there has been a phased correction in the semiconductor sector on the disk. Among them, the representative semiconductor storage supply and demand appeared at an inflection point, and the industry predicted that DRAM and NAND Flash would enter a price decline cycle. On the other hand, the Securities Times reporter noted that in the face of chip shortages, international giants continued to expand production, while the performance of domestic storage head echelon enterprises in the third quarter was generally good, accelerating product iteration and in-depth integration of the industrial chain, and actively laying out markets such as automobiles.

Storage market prices are loose

"From the perspective of market conditions and trends, storage should be down." People from Shenzhen Huaqiang North confirmed to reporters that the price of MCU, which is particularly fierce in price increases, has also loosened slightly, and on the whole, high-category electronic components have long been out of stock.

Entering the third quarter, chip prices have diverged significantly. Memory chips, as an important branch of the semiconductor industry, drAM prices have fallen continuously. Wind shows that in the case of a certain indicator 8GB of DDR4 memory, the spot price of the product fell from $3.11 each in August to the latest $2.24; the smaller 4GB product also fell.

Jibang Consulting pointed out that due to the contraction of the market's procurement of DRAM, coupled with the decline in spot prices, it is expected that the fourth quarter contract price reversal opportunity is large, and it is expected to fall by 3% to 8%, ending only three quarters of the upward cycle; In addition, it is expected that the procurement demand of the NAND Flash market will also weaken, and the fourth quarter contract price will turn into a slight decline of 0 to 5%, ending the two-quarter upward cycle, and it is expected that the overall NAND Flash market will enter the price decline cycle in 2022.

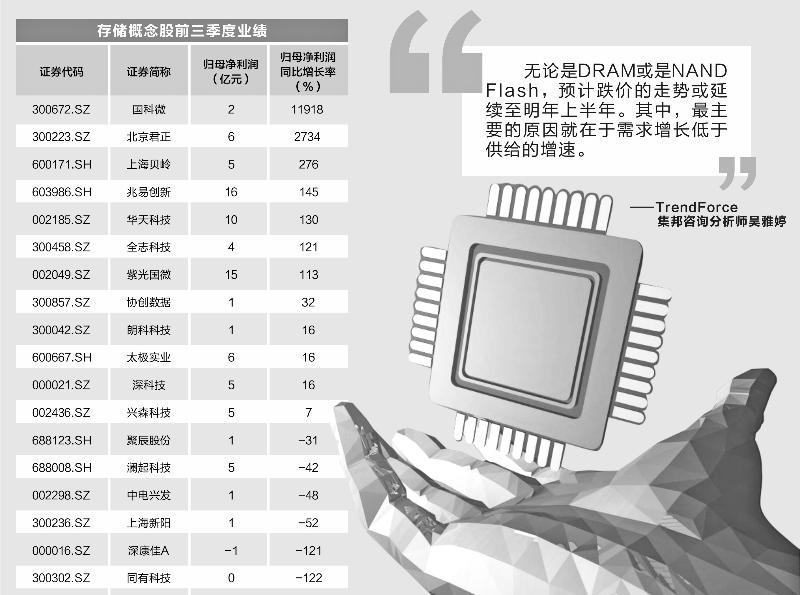

Wu Yating, an analyst at TrendForce Jibang Consulting, told reporters: "Whether it is DRAM or NAND Flash, it is expected that the trend of price decline may continue to the first half of next year. Among them, the main reason is that the growth of demand is lower than the growth rate of supply. ”

Statistics show that the smart phone, server and notebook market is usually the main consumption of DRAM market, this year's strong growth, relatively increased the year-on-year base in 2022, so next year's production, shipment of substantial growth difficulty increased; in addition, the shortage of electronic components in the long term is difficult to alleviate, terminal product assembly will also be limited, it is expected that the growth rate of DRAM demand side in 2022 is estimated to be only 16.3%, will be lower than the growth rate of the supply side.

Gou Jiazhang, general manager of Huirong Technology, a storage master control chip factory, said in an interview with the media that the demand for terminal consumer electronics in the first half of this year was strong, but from June onwards, the demand for mobile phones declined, and the weak trend in the Chinese market spread to the world, which reduced the demand for storage products to a certain extent; compared with the strong demand for business computers, consumer computers began to decline sharply in July this year, and there has been a slow recovery trend recently.

In addition, the latest market data disclosed by data research institute Counterpoint Research shows that China's smartphone sales in the third quarter of 2021 fell by 9% year-on-year and increased by 3% month-on-month, reaching 76.5 million units. Due to the weak consumer demand and the impact of the shortage of electronic components on terminal demand, the domestic smartphone market failed to show any significant improvement in sales in the third quarter of 2021.

Industry insiders pointed out that last year, due to the client, especially consumer electronics, worried about traffic obstruction during the epidemic, pulling up inventory, storage prices continued to rise, and later with the easing of the epidemic, part of the price of memory began to fall, and this year the market appeared a similar situation, the current stage of inventory water level is high, coupled with the empty window period of new product demand, resulting in the market performance peak season is not prosperous, and then hope for a wave of stocking at the end of the year.

Giant expansion

Although the storage market has adjusted, international storage giants are optimistic about the market demand for data centers, automobiles and other markets, and consider the lack of core conditions, they continue to promote production expansion.

SK Hynix, the world's second-largest memory chip manufacturer, disclosed that its net profit in the third quarter was about 3.315 trillion won ($2.843 billion), up 67% month-on-month and about 2 times year-on-year. Among them, due to the plan of some customers to digest their own inventory first, and the weak demand for the PC market, the negotiation time with some customers has been extended, and the growth of DRAM Bit shipments of the main body of revenue is slightly lower than expected, however, the average unit price of the company's DRAM products has remained nearly 10% of the growth, coupled with the improvement of dram product yield and the increase in the proportion of production, which has reduced the unit cost and ensured the profitability of this part of the business; in addition, the NAND business has turned a profit.

Looking ahead to the future, SK Hynix said that for suppliers including Hynix, inventory is still at a historical low, and the company will be more flexible to respond to the market environment; considering the demand from data centers, the GROWTH potential of the NAND market is broad. Therefore, the supply of DRAM will be more conservative from the second half of this year to the first half of next year; and the supply of NAND will be in line with the growth of market demand.

SK Hynix also announced on October 29 that it will acquire South Korean wafer foundry key Foundry for approximately $492 million. Key Foundry, which manufactures chips such as power management, display drivers and microcontroller unit semiconductors (MCUs), expects SK Hynix to triple its 8-inch foundry capacity upon completion of this acquisition.

Another storage OE giant, Micron Technology, revealed that it will expand the scale of fabs in the United States. For the memory chip market movement, Micron Technology executives acknowledged that memory chip shipments will decline moderately from very strong levels in the short term; however, in 2022, the memory market will be driven by data center, server, 5G mobile phone shipments, and automotive and industrial markets.

Samsung Electronics executives also said on the recent earnings call that considering the global chip shortage, resulting in production problems in key industries from cars to smart phones, Samsung plans to expand wafer foundry, and is expected to reach 3 times the current production capacity by 2026.

For the expansion of international giants, Wu Yating pointed out to reporters that although capital expenditure will still maintain a high water level next year, it is mainly used for process transfer and longer-term capacity planning, so the expansion of projection in 2022 will not be too obvious; considering that the current storage has entered oversupply, the average price has begun to decline; but because the industry still has the order of production planning, it is expected that the price decline will not be lower than the production cost after the total amortization, so most suppliers will continue to be profitable.

In addition to storing original plants, other wafer foundries are also actively expanding production. TSMC, the leading foundry of wafer foundries, has recently announced that it will join forces with Sony to set up a factory in Japan; GF, the world's fourth-largest foundry, officially landed on the NASDAQ on October 28, and will invest $6 billion in the next two years to expand its production capacity in Singapore, Germany and the United States.

According to Jibang statistics forecast, driven by the price increase led by TSMC, it is expected that the wafer foundry output value will reach 117.69 billion US dollars next year, with an annual growth rate of 13.3%, and the expansion of production capacity announced by major fab foundries will be opened in 2022, and the new production capacity is concentrated in 40nm and 28nm processes, and it is expected that the extremely tight chip supply at this stage will be slightly alleviated; but considering the stocking of the industrial chain at that time, the phenomenon of expected capacity relief is probably not very obvious.

IDC warns of the risk of semiconductor overcapacity in the future. It is expected that the semiconductor industry will reach equilibrium in mid-2022, and with large-scale capacity expansion at the end of 2022 and 2023, there may be overcapacity in 2023.

The domestic storage echelon is united in depth

Judging from the performance of the third quarter, the performance of A-share semiconductor listed companies is generally good. Wind statistics show that as of October 29, about 90% of the listed companies in the (Shenwan) semiconductor industry that have disclosed their performance have achieved year-on-year net profit growth in the first three quarters, and the median year-on-year growth rate has also set a record for the same period in history in the past three years; further, the performance of many listed companies including storage business has grown significantly, and strengthened the in-depth binding with the industrial chain and expanded cooperation with the automotive field.

Among them, the net profit of Guoke Micro in the first three quarters of this year increased by about 119 times year-on-year to 181 million yuan, of which the main profit contribution was concentrated in the third quarter. During the period, the revenue of many product lines of the company increased and the performance was thickened.

Guoke Micro is mainly responsible for providing data storage, multimedia and satellite positioning chip solutions, and uses the Formulas model to operate and produce. Compared with the SSD peer enterprises, the company masters its own controller chip, its self-developed solid-state storage controller GK2302 series chips have achieved the development of multiple versions, and passed the dual certification of national testing and national secret, and have achieved large-scale mass production; the company's new generation of solid-state storage controller chip GK2302 V200 is also currently in mass production, and the products based on the chip have also been officially listed in 2021. At the same time, the company has also deepened upstream and downstream links to ensure wafer production capacity in the out-of-stock market.

Tian Dahai, general manager of the product department of Guoke Micro Industry, pointed out in a recent interview with the media that the company and Yangtze River Storage have become strategic partners in 2019 and signed a long-term supply agreement; in addition, this year's storage master control chip is out of stock, and Guoke Micro uses self-developed master control chips and places orders a year in advance, so it can calm the impact of the lack of core tides, from the current market share, Guoke Micro has been in the first echelon in the domestic storage market.

As a domestic storage leader, GigaDevice's net profit in the third quarter was 862 million yuan, an increase of 178.47% year-on-year, and the net profit after deducting non-deductions increased by about 2 times year-on-year. Gigabit Innovation, which focuses on NOR Flash storage, entered the third place in the world last year; at the same time, Gigabit Innovation has cut into the DRAM chip market, and cooperation with Changxin Storage is mainly for niche markets, which has formed a profit contribution. In June this year, GigaDevice launched its first private label DRAM product, which has been certified on mainstream consumer platforms and used in mass production on many clients. According to the company's executives in the September institutional survey pointed out, 19nmDDR4 has been mass-produced, 17nmDDR3 is actively developed, if it goes well, it is expected to contribute revenue to the company next year. In the automotive field, Gigabit Innovation has launched a nationally produced vehicle specification flash memory chip, and the data throughput rate is more than 5 times that of existing products.

Through the acquisition and merger of Beijing Silicon Cheng (formerly ISSI), Beijing Junzheng also cut into the memory chip business and led the domestic automotive storage IC. In the third quarter of this year, the company continued its high-speed growth trend, with earnings nearly 25 times year-on-year to 280 million yuan. In addition to DRAM products, Beijing Junzheng is also promoting the application of Flash product lines in the automotive, medical and high-end consumer markets, and the company's Nor Flash chips for the mass consumer market have completed sample production and launched market promotion.

In the context of the shortage of wafer foundry capacity, Beijing Jun has also strengthened its capital binding with the upstream supply chain. In July this year, Beijing Junzheng increased the capital of the wafer foundry Rongxin Semiconductor, and plans to spend 100 million yuan to invest 4 million yuan in the registered capital of Rongxin Semiconductor; on the other hand, the 1.3 billion yuan fixed increase launched by Beijing Junzheng will be subscribed by Weier shares for 550 million yuan, forming a business strategic cooperation between automotive CIS and automotive storage ICs.

In addition, the net profit of Montage Technology, a storage interface chip vendor on the Science and Technology Innovation Board, was about 200 million yuan in the third quarter, down 25% year-on-year, and the net profit after deducting non-deductions increased by about 13% year-on-year. According to reports, due to the cloud computing industry from the second half of last year into the destocking stage, coupled with the DDR4 memory interface chip into the late stage of the product life cycle, resulting in a decline in product prices compared with the same period last year, dragging down the performance; and with the continuous recovery of the industry and the good performance of the Jinju server platform product line, the company's performance is obvious quarter by quarter. Operating income in the third quarter of 2021 more than doubled year-on-year. In addition, in October this year, the company's DDR5 first sub-generation memory interface chip and memory module supporting chip has successfully achieved mass production.