Financial Associated Press (Shanghai, intern reporter Xu Chuan) news, A-share listed banks three quarterly reports officially disclosed. The data shows that while the net profit of listed banks has increased steadily, the asset quality has continued to improve. Among them, the 41 listed banks in the first three quarters achieved a total net profit attributable to the mother of 1473.914 billion yuan, and if calculated in 270 days, the listed banks earned 5.459 billion yuan per day.

However, the overall performance of bank stocks in the first three quarters of this year did not show a positive correlation with profit growth. As of the close of trading on October 29, the Cumulative Decline of the Shenwan Bank Index year-to-date was 0.65%. At the same time, the large-scale net breaking of the stock price is still a "big and difficult" problem, the average price-to-book ratio of the Shenwan Bank Index is 0.64, and only a few 7 banks such as China Merchants Bank and Bank of Ningbo have not broken the net.

Industry insiders said that with the improvement of asset quality and the stabilization of net interest margins, the drag on net profit growth slowed down, and the industry boom is expected to continue to rise.

Net profit increased overall

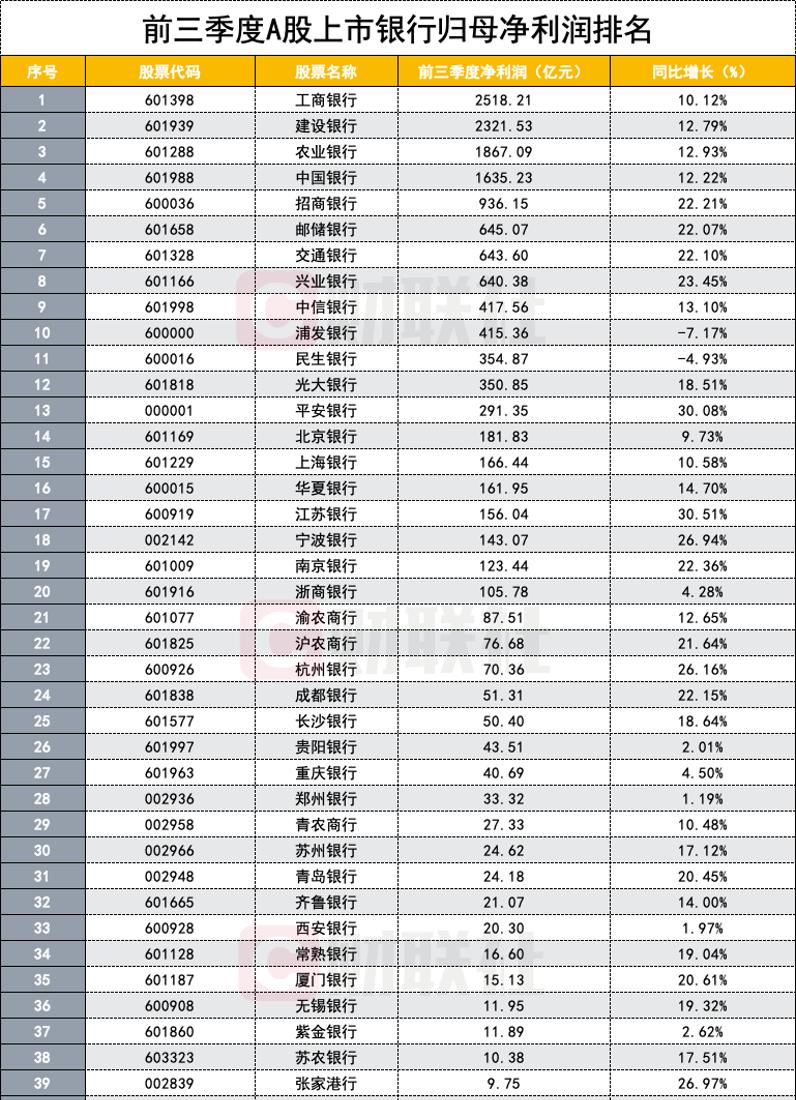

Compared with the previous two quarters, ICBC, CCB, ABC, BOC and CMB are still the five listed banks with the largest net profit attributable to their parents in the first three quarters, with ICBC ranking first with 251.821 billion yuan, with a single-quarter net profit growth rate of 54.04%.

At the same time, compared with the end of the second quarter, there have also been some changes in the net profit ranking of banks. Postal Savings Bank achieved a net profit of 64.507 billion yuan in the first three quarters, surpassing the Bank of Communications and rising to the sixth place; China CITIC Bank achieved a net profit of 41.756 billion yuan in the first three quarters, ranking up to the ninth place; Qingnong Commercial Bank achieved a net profit of 2.733 billion yuan in the first three quarters, jumping from 31st to 29th, second only to Yu Rural Commercial Bank and Shanghai Rural Commercial Bank in the first three quarters.

The Financial Associated Press reporter noted that in the first three quarters, the net profit of 14 banks increased by more than 20% year-on-year, and a total of 32 exceeded 10%. Among them, the net profit of Bank of Jiangsu and Ping An Bank increased by more than 30% year-on-year, 30.51% and 30.08% respectively.

By bank type, state-owned banks and joint-stock banks contribute more than 90% of the profit sources. Among them, the net profit of the six state-owned banks accounted for 65.34% of the net profit of all listed banks, the nine A-share listed joint-stock banks contributed 24.93%, and the urban and rural commercial banks accounted for 9.73% in total.

The Financial Associated Press reporter noted that net interest income is still the "power source" for listed banks to generate profits, and the net interest income of each bank at the end of the third quarter accounted for more than 59% of all revenue; on the other hand, the proportion of non-interest net income of some banks also continued to rise, such as China Merchants Bank and Bank of Hangzhou, which had a non-interest net income of more than 20% in the first three quarters of the previous year.

"Listed banks have both the willingness and ability to maintain stability on the profit side." Zhang Yu, chief bank analyst of Guotai Junan, said that from the third quarter of 2021, the credit cost of banks is expected to achieve a real downward trend and promote the continuous release of profits.

The tianfeng securities banking team also pointed out that the bank's release of profits, on the one hand, helps itself to replenish endogenous capital, reduce the capital gap, enhance soundness, on the other hand, it also helps to alleviate the pressure of the financial system on the bank's capital increase. Therefore, whether from the perspective of the bank itself or from the perspective of policy, there is an appeal to accelerate the release of performance.

The data shows that the capital adequacy ratio of listed banks as a whole rose slightly in the third quarter, and the core Tier 1 capital adequacy ratio of 32 listed banks rose month-on-month.

The defective rate continues to decline

As of the end of the third quarter, the overall asset quality of listed banks remained stable, with an average non-performing loan ratio of 1.27%. Except for shanghai rural commercial banks, which did not disclose their second quarter reports, the non-performing loan ratio of a total of 37 banks remained unchanged or decreased from the end of the second quarter. The non-performing rate of the remaining three banks has risen slightly, namely Bank of Xi'an, Qingnong Commercial Bank and Zheshang Bank, and compared with the end of 2020, in addition to the above three banks, the non-performing rate of Chongqing Bank has also increased by 0.06 percentage points.

Specifically, at the end of the third quarter, there were 10 banks with a non-performing loan ratio of less than 1%, compared with only 7 banks at the end of the previous year. The lowest non-performing rates were bank of Ningbo, Changshu bank and postal savings bank, all below 0.9%. From the perspective of the decline, the non-performing rate of Zijin Bank at the end of the third quarter was 1.35%, but it fell by 0.32 percentage points from the previous quarter.

Listed banks generally said that in order to maintain the stable development of asset quality, they have adopted measures such as continuously strengthening the implementation of credit risk policies, actively withdrawing from risky customers, and strictly controlling the addition of new non-performing assets; at the same time, they continue to strictly classify assets, prudently make provisions, and accelerate the collection and disposal of existing non-performing assets.

The third quarterly report of postal savings bank pointed out that it is necessary to carry out a comprehensive risk assessment of subsidiaries, strengthen risk consolidation management, deepen the application of internal ratings in automated approval, differentiated post-loan, risk monitoring and reporting, do a good job in credit risk identification and prevention, and strengthen risk investigation in key areas.

Ping An Bank also said that in terms of public loans, for important business areas such as real estate and political credit, combined with the changes in the current external policy environment, ping an early response will be made to adjust the business orientation and access rules in a timely manner.

"The core book non-performing indicators of listed banks will continue to improve." A brokerage bank analyst said that from the perspective of absolute volume, even if there is a local bad generation on the margin, it is impossible to reverse the general trend of the overall liquidation of the bank's asset quality.