Case Theme Words: Industrial Value Chain • In-depth Marketing

Hejun Consulting Case Series: Zhenghong Feed Marketing Chain Reconstruction

Zhang Bo wrote in the summer of 2007

The core idea of in-depth marketing is to maximize the system efficiency of the industrial value chain, and then maximize the efficiency of the enterprise. For industries such as fast-moving goods and home appliances, the core link of the industrial value chain lies in marketing, and the core proposition of in-depth marketing is to improve the system efficiency of the marketing chain, and the implementation of the specific model is the marketing model with channels as the core. The Midea store model, the "1 + N" model of the building materials industry, and the manufacturer value integration model that is widely suitable and adapts to the principle of division of labor and efficiency in the industry are all specific implementation models.

Although the marketing link of the feed industry elaborated in this case is still the core link, due to the highly homogeneous products, special credit sales habits and chaotic industry environment, it is difficult to improve the operational efficiency of the enterprise only by implementing the channel-centered marketing model in the marketing link, and it must be considered from the overall industrial value chain, focusing on the most critical and weakest link in the industrial value chain (the breeding link in the free range state) to formulate the enterprise development strategy, and then determine the marketing model and build the core competitiveness. Only in this way can we get out of the predicament, achieve scale development and improve profitability.

The consulting services provided by Hejun Consulting for Zhenghong Feed are carried out in accordance with this idea. The core points of the Zhenghong case are: to conform to the evolution of the aquaculture industry, starting from service marketing, actively organize and integrate relevant resources, develop a breeding consortium based on the characteristics of free range breeding and division of labor, improve the efficiency of the aquaculture industry, change from the original simple feed production and distribution to the comprehensive service of supplying aquaculture, regain the dominant position of the industrial chain, and establish a competitive advantage in the future.

Hejun Consulting served Zhenghong Feed in 2001. In the past 6 years, Zhenghong has not only operated in accordance with the direction of this development strategy and marketing model, but also continuously deepened it. Moreover, this model has gradually evolved into a common model for China's strong feed enterprises, and most of the large feed companies such as Tongwei, Liuhe, and Yongda have adopted similar development strategies and marketing models.

First, the background of the case

1. Feed industry introduction

The Chinese feed industry originated in the late 1970s, when the Thai Chia Tai Group introduced feed to China.

The 1990s was the golden age of the development of the feed industry, and domestic feed enterprises such as Sichuan Hope Feed, Shandong Liuhe Feed, and Hunan Zhenghong Feed rose and developed rapidly.

(1) The basic situation of the industry. At present, the annual output of feed in the whole industry is about 70 million tons, of which about 10 million tons of concentrate, about 2 million tons of premix, and the rest are full-priced. The feed industry belongs to the bulk agricultural and sideline products industry, and the logistics cost is high. Therefore, the transportation radius can not exceed 500 kilometers, otherwise it is very economical, so the way feed enterprises are bigger is to build factories in other places.

Due to the high profits and low threshold of the feed industry in the early stage, coupled with the regional characteristics of the industry, new manufacturers continue to enter, and in less than 10 years, 20,000 to 30,000 feed enterprises have emerged in the country. Because of this, since 1998, the competition in the feed industry has become increasingly fierce (price war, promotion war), resulting in a gradual decrease in the level of industry profits.

(2) The basic characteristics of the industry. The feed industry is an intermediate industry linking planting and breeding, and the cost of production and the price of products are subject to multiple restrictions such as grain prices and the price of breeding products.

1) The rise in raw materials such as upstream grain prices has led to an increasing cost of feed raw materials.

2) Due to the relationship between supply and demand, the price of downstream aquaculture products often appears in the situation of "harvest valley and poor farmers", which makes the demand for feed by farmers decline, resulting in large sales fluctuations of feed enterprises, excess production capacity, and then higher costs.

3) The product homogenization is serious, additives are placed randomly, the quality is uneven, and the market order is chaotic.

4) The low industry threshold and the consumption habits of credit sales have made the industry mixed, the price war, the promotion of sales wars, and the war on credit sales are not stopping, the scale advantage cannot be brought into play, the cost remains high, and the economic benefits have dropped significantly.

5) Because the breeding efficiency is affected by various factors such as breeding technology, epidemic prevention, variety, raw materials, etc., under the credit sales and false publicity of small manufacturers, the quality advantages of large manufacturers are difficult to show, which is also one of the important reasons for the existence of obvious regional characteristics in the feed industry.

In such a harsh industry environment, the feed industry generally has the phenomenon of "bad money expelling good money". The production scale, technology, capital and other advantages of large feed manufacturers are difficult to play, highlighting the "bottleneck" of development.

(3) Outstanding problems in the industry. China's feed industry mainly has the following problems:

1) The market order is chaotic, and it is difficult for dealers to make money. Due to the high degree of homogenization of products, dealers do not have breeding service support for farmers, etc., and must rely on bottom funds to maintain customers, the cost of funds is high, and the scale is not large. In addition, more and more feed is sold, everyone has no unique selling points, farmers choose distributors at will, so the source of customers is unstable. The price transparency of brand-name products does not make money, and the risk of miscellaneous brand products is high, and the recognition of farmers is low, and it is not profitable.

2) The breeding efficiency is low, and the farmers do not earn money. Improper prevention and control of diseases, backward breeding technology, large breeding risks, unstable pig prices, poor varieties, low proportion of breed improvement, free range breeding, lack of scale, etc., resulting in farmers not making money. In 2002, in the Hunan market, the price of soil offal pigs dropped from 2.9 yuan / catty to 2. 45 yuan / catty, the price of fine breeding pigs by 3. 6 yuan / jin down to 3. 15 yuan / catty.

2. Zhenghong Enterprise

The predecessor of Zhenghong Feed Enterprise is the state-owned farm feed factory. In the mid-1980s, Chairman Wu Mingxia led several entrepreneurs to develop a chia substitute product, Zhenghong 001 pig concentrate, on the basis of Chia Tai products, so that Zhenghong gradually developed.

Enterprises of a certain size in China's feed industry are trapped by the "disorderly competition" of small and medium-sized feed manufacturers and the credit sales habits of the industry, and Zhenghong Feed Enterprise is no exception. In 2000, Zhenghong's production capacity has reached 800,000 tons, but the annual sales volume is only 200,000 tons.

In 1999, in the face of the homogenization of the feed industry's promotion war, price war, terminal war and the bad habit of industry credit sales, Zhenghong began to implement the industrialization model of "company + farmer", providing farmers with in-depth services such as pig seedlings, feed, breeding and disease guidance, and commodity pig recycling, and recycling at the agreed price or not lower than the market price at that time, so that farmers can "make money", so as to avoid vicious competition in the industry, achieve effective sales, and reduce capital risks. To this end, Zhenghong also invested in the construction of the largest breeding farm in Hunan with more than 10,000 heads, and set up a Xingnong Company that specializes in purchasing pigs.

However, problems have arisen in practical operation. Farmers not only blame the manufacturers for all the problems of sick and poor pigs, but even more do they sell the pigs they raise well, hand over all the pigs that are not well raised to the factory, and even "steal the beams and change the pillars" and hand over the unqualified commercial pigs that are not the pig seedlings of the manufacturers to the manufacturers. The end result was that the "company + farmer" lasted less than two years and ended in failure.

Second, the interpretation of the problem

The strategic choice of the enterprise must adapt to the changes in the industry and the market, that is, interpret the industry and see through the industry, and then make strategic choices, and then establish the business model - a structured combination of various businesses.

1. Feed industry analysis

(1) Changes in the industrial environment. Before the mid-1990s, the original level of aquaculture industry development was in a state of natural dispersion, and the purpose of farmers was to consume surplus grain - to use rice for breeding, in exchange for money (rice is sold at a low price, and it is not easy to sell), basically there is no concept of economic benefits of production ratio, risk avoidance is the most important requirement of farmers. In this context, Zhenghong provides high-quality feed, greatly improves the efficiency of farmers' surplus grain feeding, and successfully establishes brand differences through first-mover advantages and scale advantages, which is the key to Zhenghong's success.

In the late 1990s, the farming purposes and expectations of farmers changed, and pig farming became a means for farmers to make profits. They are concerned about the comprehensive efficiency and effectiveness of breeding, and have higher requirements for breeding species, technology, breeding pigs, etc., and these factors have gradually become key factors affecting breeding efficiency. In addition, in the case of oversupply, the circulation of livestock is also very critical, and the role of feed is rapidly weakening. Therefore, the effective provision of integrated aquaculture services is the core of competition. In this case, whoever can recognize this change and respond in time will gain a first-mover advantage in the new competition rules.

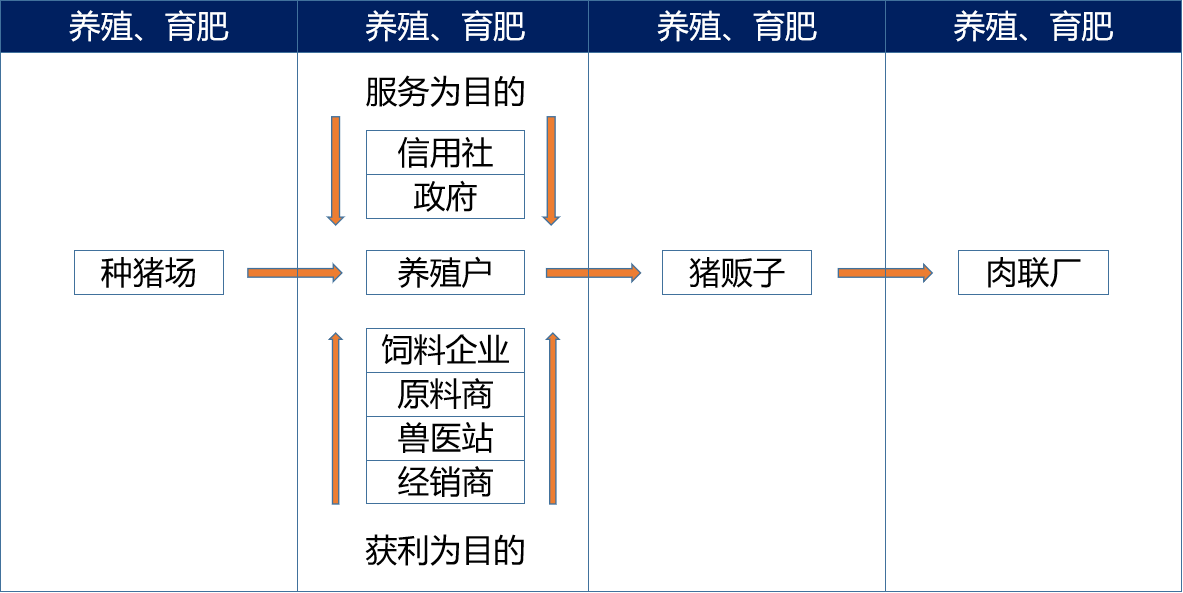

(2) Value chain analysis of the livestock industry. The core link in the ± of the pig industry value chain (see Figure 6-1) is the breeding and fattening process of farmers, first, because this is the largest value generation link in the value chain; second, because other links are organized by scale, and in the case of universal free range, the reproductive fattening process cannot be won by scale. Therefore, how to integrate a large number of industrial resources into these scattered farmers has become a key issue in the value chain of the aquaculture industry.

Figure 6-1 Pig industry value chain

Feed enterprises, raw material suppliers, veterinarians and epidemic prevention stations, feed raw material dealers are all carrying out business activities around farmers, they are aiming at their own profits, and at the same time, the government and credit cooperatives are also serving farmers. In addition, front-end and back-end breeding farms and pig dealers are also carrying out activities around farmers. When all industrial resources are concentrated in farmers, farmers become the core resources for future competition.

All aspects of industrial resources are centered around farmers, and this form of industrial organization is market-driven and spontaneously formed. The following two points are worth noting.

1) What is the role of feed enterprises in it? For farmers, the most critical resources are fine breeding pigs, the price of fences, funds, followed by information and epidemic prevention, disease treatment. These resources are important because of their scarcity and benefits for farmers. Feed is not important because none of the above two are available. Market conditions with severe oversupply make feed the least scarce of these resources; the indifference of feed products (or the inability of farmers to make a clear distinction) makes its benefits to farmers irreplaceable.

The conclusion is that feed enterprises have basically no place in this way of industrial organization.

2) This form of industrial organization is actually unorganized. Although all these resources are being developed around farmers, they are scattered and provided independently, and farmers need integrated services, and the result is that farmers are integrating these resources and assuming the responsibility of integrating industrial resources. However, there are certainly many obstacles to coordination among different stakeholders, and these resources cannot be perfectly integrated and cannot reflect the maximum benefits. The integration of the resources of the aquaculture industry is provided to farmers, which is the requirement for the future development of the aquaculture industry, and it is also the opportunity for the largest and most financial feed enterprises in the aquaculture industry to establish a position in the future industry.

(3) The strategic point of industrial competition. The key link (but also the weak link) in China's aquaculture industry chain is the breeding link in the state of free range. In this link, only when the relevant breeding elements (excellent varieties, feeding management, epidemic prevention technology, acquisition services, funds and high-quality feed, etc.) can be dynamically matched and optimized, the breeding efficiency can be maximized. In the free-range state, these elements are discrete and independently provided, and the general farmers cannot effectively integrate and obtain them due to cultural quality, technical level and other factors.

The above situation provides a strategic industry opportunity for feed enterprises: conform to the evolution of the aquaculture industry, actively organize and integrate relevant resources, cultivate a breeding consortium based on the characteristics of free range aquaculture, division of labor and coordination, and moderate scale, improve the efficiency of the aquaculture industry, change from the original simple feed production and distribution to the supply of comprehensive aquaculture services, regain the dominant position of the industrial chain, and establish a competitive advantage in the future. This is also the only way for feed enterprises to break through the scale of the "bottleneck" of development. Today, Tongwei, Hope, Liuhe, Hengxing, Yongda and other large feed leading enterprises are developed because of this.

2. Strategic analysis of Zhenghong

(1) The dilemma of Zhenghong's traditional business methods. Just as mentioned earlier, Zhenghong has developed rapidly by relying on the advantage of first mover. However, from the perspective of the core competitiveness of enterprises, in addition to the accumulated brands, the advantages of Zhenghong are very fragile, as evidenced by the serious decline in core niche markets such as Xiangtan and Changsha in Hunan from 2000 to 2002.

1) Analysis of the original marketing value chain of Zhenghong Feed Enterprise (see Figure 6.2). There are three sources of efficiency in the original marketing value chain of Zhenghong Feed: one is the brand advantage of the industry pioneer; the second is the strong strength of the dealer team; and the third is the cost advantage of bulk raw materials. However, these advantages are gradually lost under the impact of factors such as high promotions and high profits of small and medium-sized feed manufacturers, as well as the transparency of their own price system and the lack of maintenance and management of channels.

Since the mid-to-late 1990s, Zhenghong Feed has invested in the establishment of a first-class breeding farm in China. At the same time, technical personnel and college students were dispatched to set up a scientific and technological service team, and township veterinarians were organized to set up a "veterinary angel" service team to carry out technical service work. However, the market share is still shrinking, the brand influence is gradually weakening, the loyalty of a number of businesses is declining, the channel stability and distribution power are also declining, and the cost-effectiveness ratio of promotions is constantly improving.

Figure 6-2 Zhenghong feed enterprises original marketing value chain

In the highly homogeneous and non-standardized market environment of products in the feed industry, we cut into the market from the service point of view, strengthen the service capabilities of customers, and control dealers and terminals in this way. This is true, but the key problem is that this "click-and-click" technical service (including variety improvement, etc.) cannot be carried out among the vast number of farmers, and the main body of the market is retail, so it is not surprising that technical services lack effectiveness.

2) Control the "channel funds". From the book point of view, Zhenghong's payment has not yet formed a significant problem, thanks to the large dealers have been requiring cash spot, in fact, the payment risk is transferred to the large dealers, the price is to give a large part of the profits to the large dealers. The problem is that the dealer has obtained this part of the profit, but rarely bears other responsibilities other than the risk of payment collection, and does not fulfill the responsibility of the dealer to correct the rainbow. If the goods are directly supplied to retail stores or farmers, although the loss of profits in the circulation link can be reduced, it will inevitably increase the payment receivables, because the farmers are buying on credit, while the second batch and retail stores do not have enough working capital to keep up with the cash of Zhenghong. In addition, sales expenses are also difficult to support.

Therefore, the control of "channel funds" has become the key to industry competition and scale development, and Zhenghong's traditional marketing model lacks the cultivation and management of this ability.

(2) Zhenghong's "company + farmer" model. As farmers pay more and more attention to profits, the breeding method has also begun to change from "single-family farming points" to "multi-family farming cooperatives", which is triggered by the requirements of industrial resource integration. Changes in market demand put forward requirements for variety improvement, and variety improvement is difficult to be effective at a single point, and a large number of farmers must be organized to form a breeding consortium. This consortium will become the main organizational method of the production link of the aquaculture industry, and it will also be a key resource for all parties involved in the future industry to compete.

Zhenghong also accurately saw the strategic point of industrial competition, and began to implement the "company + farmer" model. The intention of the "company + farmer" model is to provide "service + feed + repurchase", which not only solves the problem of lack of funds for farmers, but also gets rid of the dependence on "pickpocketing" dealers. Although the capital occupation is relatively large, the profits from the repurchase of breeding pigs and livestock pigs can be completely compensated.

Zhenghong thought of the market risks and breeding risks encountered in the "company + farmer" model, but did not take into account the moral hazard of farmers. The moral hazard of farmers is the weakest point of the "company + farmer" model, which has led to the failure of this model. Although Zhenghong's "company + farmer" model failed, the reason for the failure was the problem of method and path, and the direction was absolutely correct. To survive, you must build product-based service differentiation.

Third, the solution

Zhenghong's specific strategic choice is to activate the "company + farmer" model, and the key point is to shift the model emphasis from the manufacturer (Zhenghong) to the channel, so that Zhenghong will be transformed into a breeding service provider, and Zhenghong's existing or future-cultivated services, brands, breeding pigs, pig circulation, and deep processing will gain a "control" position in the marketing chain.

1. New "company + farmer" model

Zhenghong's "company + farmer" model is still feasible for breeding chickens, ducks and other industries with a high degree of industrialization (Shandong Liuhe Feed Chicken and Duck Feed uses a "company + farmer" model similar to Zhenghong), which can provide comprehensive services at low cost and avoid the risk of capital recovery. However, for the livestock industry, which is mainly free-range breeding, it is difficult to provide comprehensive services, and it is also difficult to avoid capital risks.

Zhenghong saw the strategic point of industrial competition, but did not have insight into the purpose of providing comprehensive services in the industrial environment of free range breeding and credit marketing, which should be directed at "controlling channel funds", and then activating various in-depth service business units and industrial elements such as breeding pigs, livestock circulation, livestock slaughtering cold and fresh, and deep processing. This is the correct path for Zhenghong to become a large enterprise with an evergreen foundation in the aquaculture industry. The biggest change between this new business model and the original "company + farmer" model is to shift the focus of the model from manufacturers to channels, so that the model has universal significance, and thus also changes the main body of risk.

Therefore, Zhenghong's opportunity and future-oriented strategy are: no longer to be a simple feed producer, but to become a breeding service provider, through grafting dealers with service functions, the farmers are organized to form a breeding consortium, so that the aquaculture industry value chain can operate efficiently. Based on this concept to organize industrial resources, build a team, let them know how to organize resources, implement industrial strategy and market strategy, in time, Zhenghong will become a leading enterprise in the aquaculture industry.

2. Key points of the "company + farmer" model

The basic idea of the "company + farmer" model is to use the core service resources of the manufacturer to graft the channel resources and other social resources to provide comprehensive services for farmers. However, Zhenghong's existing channels lack this function and lack awareness. Therefore, it is necessary to transform the existing channels so that the channels have one or more of the seven major breeding elements of technology, capital, disease prevention, epidemic prevention, circulation, feed, and raw materials, and constitute a marketing channel system with complete service functions by grafting other functional members or using the service functions formed in the natural state.

From the perspective of the seven major breeding elements of technology, capital, disease prevention, epidemic prevention, circulation, feed, and raw materials, in addition to raw materials and feed, channel members with functions such as capital, disease prevention, epidemic prevention, and circulation are common in the natural state, but can the main body that can provide technical support to a large number of retail households exist? This is the key point of whether the new "company + farmer" model can be feasible.

Therefore, the main point of the new model is to find the main body that can provide technical support among retail investors - breeding experts.

First of all, it is necessary to find breeding experts in the natural state, who have more than 100 pigs and are very experienced. Because the actual pig raising method is relatively primitive, unlike chicken raising, it has reached a considerable degree of industrialization, so it is difficult to cultivate pig breeding experts according to a certain norm or standard, and pig breeding experts can only be found from the natural state. It is not to concentrate all the pig breeders, but to keep the farmers scattered. If we want to integrate these scattered farmers into zhenghong users, we must pass the demonstration and aggregation effect of large farmers.

Then, to provide help and services, these large breeders to introduce breeding pigs, to develop breeding farms, and to provide services to retail households, including epidemic prevention and sales, etc., to reduce breeding risks, but also to cultivate large households into Zhenghong dealers.

Let the large households lead to complete the activities on this value chain, Zhenghong is still a feed enterprise, and the reason why these links cannot be done by Zhenghong is that the cost is high, and the second is that Zhenghong does not have enough resources and does not have enough ability, and it is far inferior to the breeding experts.

IV. Promote implementation

In the implementation of the model, the project team carried out a pilot in the Xiangxiang market in Hunan (the sales of the market slipped from nearly 2 000 tons/year to about 20 tons/year, and the sales of the pilot exceeded 100 tons in three months). The main tasks of the pilot are twofold: one is to explore specific implementation models; the other is to sum up experience and enrich the models so as to have the feasibility and effectiveness of large-scale replication and promotion.

1. Two typical breeding service models

(1) User organization system of "local business representative + terminal distributor + breeding demonstration household + retail household". Providing comprehensive services for the majority of farmers is the key to the transformation of feed enterprise channels, and it is necessary to effectively organize farmers in the free-range state to overcome discreteness and thus provide effective services economically.

In practice, according to the level and characteristics of aquaculture development in various places, we have summed up some effective ways of organizing farmers. In areas where aquaculture development is general, a user organization system of "local business representatives + terminal distributors + breeding demonstration households + retail households" (see Figure 6-3) has been established, as well as an inclusive veterinary service system, that is, enterprises and terminal distributors jointly hire local excellent veterinarians to provide free epidemic prevention and breeding technology consultation and other services. At the same time, we should actively graft and integrate local credit cooperatives, slaughtering and processing enterprises or individuals, fine seed farms, and raw material dealers, and systematically provide comprehensive services for farmers in combination with the specific requirements of local breeding, while feed enterprises provide support in publicity and organization, technical training, pharmaceutical materials, market information, and personnel management.

Figure 6-3 User organization system of "local business representative + terminal distributor + breeding demonstration household + retail household"

1) Identify the target market as a large breeding household, integrate the existing marketing resources such as products, promotions and technologies to provide systematic aquaculture value-added services for it, and use it as a demonstration household to radiate other aquaculture retail households.

2) Transform the existing general dealers, consciously support local influential veterinarians, livestock traders and other related distribution or cooperative distribution feed dealers, and use their service capabilities such as medical epidemic prevention and pig acquisition to closely serve the majority of farmers and establish service functional channels.

(2) Breeding consortium model. In areas where aquaculture is more intensive and developed, the gradual development of the breeding consortium model (see Figure 6-4) o The core market of feed enterprises is the developed area of aquaculture, the breeding is intensive, the scale is large, the breeding species and technology are relatively good, and it is most likely to realize the industrialization of aquaculture - the breeding consortium model first. The specific approach of the farming consortium model is to organize and develop by enterprises or larger distributors

Figure 6-4 Aquaculture consortium model

Core farmers are the mainstay, establish an organizational form in which large households breed large households with small households, and realize the internal division of labor (generally core households raise good seeds and are responsible for breeding and breeding, large households are responsible for breeding and fattening, and retail households are responsible for fattening out of the pen), and achieve synergy in the form of close cooperation under economic transactions to form regional breeding cooperatives. Zhenghong conducted a strategic alliance (after self-establishment) with large-scale slaughtering processing and circulation enterprises to realize the fixed-point acquisition of the order system, create a brand of safe food in the meat market, and assist in the sales of finished meat products.

Zhenghong integrates resources such as fine seeds and veterinarians to actively guide the improvement of breeding complex varieties, provide breeding and epidemic prevention technical services, strengthen the management and maintenance of daily feeding, and ensure the safety, high quality and low cost of livestock products. In this way, an efficient and coordinated aquaculture industry value chain has been formed, and feed enterprises have become the dominant players in connecting and managing the industrial chain, and have regained the initiative in market competition.

2. Experience summary and model extension

Although the breeding service model has been determined, many practical difficulties have been encountered in the implementation of specific markets. First of all, the distribution of farmers under the characteristics of free range farming is scattered and generally small; second, the development of aquaculture levels in various places is unbalanced, and the characteristics, habits, and preferences of breeding are different; third, the degree of circulation and development of rural markets is different, and the differences are relatively large, coupled with the influence of rural infrastructure (transportation, communications, finance, etc.), humanities, policies, and other related factors, resulting in large differences in service demand, great difficulty in management, and large implementation costs, and enterprises directly carrying out comprehensive services, with large resource inputs, poor results, and low efficiency.

In view of the large market differences, based on the actual resource situation, the original distribution network can be transformed according to the situation through development, optimization and innovation, so that it has the comprehensive functions of comprehensive breeding services and efficient distribution.

(1) Development of functional channels for services. In the newly developed market and some of the original markets, we will consciously support the local influential veterinary distributors or cooperative distributors, use their service strength and influence in practicing medicine and epidemic prevention, occupy the existing breeding households in the regional market, and provide them with other breeding supporting services to support them, and guide the development of the breeding consortium centered on the "veterinary dealer". In addition, it is also possible to develop dealers with service functions such as fine seeds, recycling, distribution, and financing, such as local livestock product distributors and raw material dealers, and actively develop service functional channels.

(2) Grafting of distribution compatibility channels. Due to the widespread sale of feed market terminals on credit, there is a great demand for channel funds. In the process of channel transformation and development, we can actively graft the distribution channels of other agricultural products, such as dealers who distribute pesticides, fertilizers, seeds, and other products, and the network of rural supply and marketing cooperatives, and make use of the customer relations of the original dealers to provide financing services, supporting breeding technology and information services to the farmers, and jointly develop the farmers. In this way, dealers have increased feed sales in the original business, improving operational efficiency, and farmers have also received the convenience of purchase and more service support.

(3) Synergy of regional aquaculture value chains. Through grafting local slaughtering and processing and internal and external sales enterprises, signing long-term contracts with dealers to organize farmers to purchase at fixed points, dealers sell feed on credit, buy back # livestock products, feed enterprises organize the supply of fine seeds and veterinary services, build a regional breeding industry chain, carry out various linkage collaboration, realize one-stop operation, and improve breeding efficiency. In this kind of regional industrial cooperation, all relevant entities have gained benefits, especially the breeding efficiency of farmers has been significantly improved, and risks have been effectively shared. Feed enterprises can establish stable channels, loyal customers and good corporate image, and obtain the absolute advantage of regional market competition.

Fifth, experience

The direct reason for the decline in the Zhenghong market is due to the service marketing of large feed enterprises such as Xiangda and Dabeinong and the "chaotic fist" of small and medium-sized feeds. In the state of highly homogeneous products, it is necessary to create differentiation in services, and it is impossible to achieve effective services simply by relying on Zhenghong's own resources, and the failure of the "company + farmer" model proves this.

Our consulting purpose in Zhenghong is to find a simple and effective service model that can provide the majority of retail investors. In addition, controlling the channel, especially controlling the channel funds, is also a problem that must be solved. The user organization system and the breeding consortium model of "local business representative + terminal distributor + breeding demonstration household + retail household" solve these two problems very well. At the same time, we also see that "upstream - breeding pigs" and "downstream pig deep processing", especially the downstream extension can provide core services (the most controlled services), but also have huge industrial opportunities (cold fresh, low-temperature cooked food, etc.). This kind of business portfolio can also enable Zhenghong to improve the service and price power of the feed link with high-margin upstream and downstream.

Zhenghong's consulting process has enabled us to deeply understand the true meaning of the phrase "strategy is out.". The task of Zhenghong Consulting is to solve the sales problem from the feed marketing link, but in the process of solving the problem, we gradually deepen from the feed service marketing strategy, to the feed marketing strategy - service marketing model, to the vertical integration of the entire industry, so as to see the appearance of leading Zhenghong to implement the "large-scale agricultural industrialization". Later, Zhenghong also carried out vertical-integrated operation in this direction.

In some industries, only by rising from the strategic level to the strategic level of thinking about marketing propositions can it be possible to think about the fundamental propositions of business operation and development with a broader vision and more depth, rather than solving the problem of temporary sales performance. Peter Drucker, a generation of management gurus, believes that the main function of the enterprise is marketing and innovation. I think there may be such an understanding.