Financial Associated Press (Shanghai, editor Xiaoxiang) news, what is the global financial market most afraid of at the moment? Earlier this week, the "oolong" of interest rate hikes made by US Treasury Secretary Yellen may have told investors the answer.

Yellen said at an event in The Atlantic on Tuesday that "while the government's additional spending plan is small relative to the size of the economy as a whole, it is possible that the Fed will have to raise interest rates to ensure that the U.S. economy does not overheat." As soon as Yellen spoke, the three major U.S. stock indexes quickly dived intraday that day, and the Nasdaq hit the biggest one-day decline in a month.

Although Yellen rushed to clarify shortly thereafter, denying that her statement was to predict the Fed's actions. But such a painless and itchy sentence has brought such a big shock to the market, which is very telling in itself. Especially right now, the market is entering a very sensitive May!

What's special about May? Many common investors may think of the first time, perhaps "five poor six seven turned over", "May sell and then leave" and other well-known Chinese and Western stock proverbs. But many people in the industry who study the Fed will not forget what the then Fed Chairman Bernanke said in May eight years ago, and what kind of earthquake caused in the global market.

"Shrink Panic" & "Bloody May"

It was that year that the term "taper tantrum" was officially engraved in mainstream financial dictionaries.

Eight years ago, in May, when then-Fed Chairman Ben Bernanke hinted that the Fed might begin to scale back its crisis-era bond-buying program, global bond yields soared and risky assets plummeted. In the month following Bernanke's speech, the benchmark 10-year Treasury yield jumped 50 basis points, with the MSCI Emerging Markets Index tumbling 14 percent and the NASDAQ 100 down 4 percent over the same period.

And just as Yellen's casual speech this week can cause a market uproar, the current market situation is too similar to eight years ago!

Over the past two months, Bank of America's monthly fund market surveys have shown that the possibility of a "panic" in the bond market, or rising inflation, has replaced the COVID-19-related risks as the tail risks that investors are most worried about.

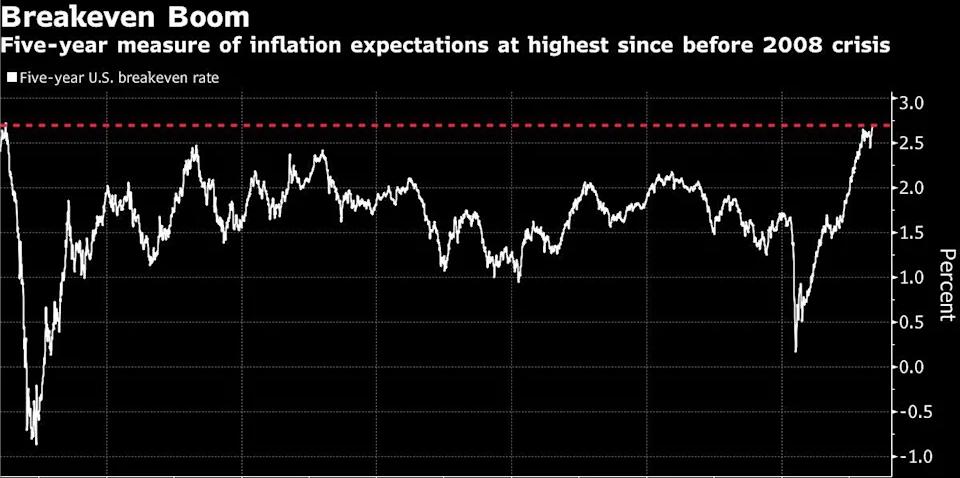

U.S. 5-year breakeven inflation has now climbed to its highest level since July 2008, and the Bloomberg Commodity Index hit a new ten-year high, leading a growing number of asset managers to believe that rising inflationary pressures will force the Fed to tighten monetary policy early. Some keen hedge funds have begun to reduce their holdings in technology stocks this week, instead of increasing their holdings in cyclical blue-chip stocks, especially bank stocks, which are more sensitive to the interest rate hike policy, and even began to increase their short selling of US Treasuries.

Dario Perkins, head of TS Lombard's Global Macro Division, said that an important reason why hedge funds urgently adjusted their positions to cope with potential monetary policy tightening pressures was to prevent the market shock caused by the "shrinkage panic" in advance.

Although several senior Fed officials, including Fed Chairman Jerome Powell, have repeatedly stressed that the Fed still intends to stand still and tolerate inflation slightly above 2% without taking action to cool the economy. But the market is still worried that in some near future, all these promises will become a "mirror flower and water month".

Central banks in the U.K. and Canada, in particular, have slowed bond purchases over the past few weeks as their economies have improved, reminding traders that the Fed cannot shy away from scaling back on bond purchases forever, especially as growth rates spike across U.S. economic indicators.

Eight years ago the market situation vs the current market situation

An interesting set of contrasts is that in That May eight years ago, before the "shrinkage scare" broke out, whether it was the indicator 10-year US Treasury yield, the inflation-protected bond (TIPS) breakeven yield, or the 2-year-10 us Treasury yield curve, they were all at a very similar price point to today. Perhaps the biggest difference is the valuation of U.S. stocks, with the current forward price-to-earnings ratio almost doubling what it was then.

Many industry insiders said that given the current valuation of the US stock market is already high, once there is a hint that the Fed will deviate from the existing policy - no matter from any source, any context, it will be seen as the biggest risk to trigger stock market turmoil.

"The biggest threat to the market is the jump in interest rate volatility, as we saw at the end of February," said Pilar Gomez-Bravo, head of investment at MFS Investment Management. "The valuation of risk assets is already high, so there's not much room for complacency."

While the current measure of implied volatility in foreign exchange, Treasuries and U.S. stocks has pulled back somewhat after rising at the end of February, suggesting that the market believes that the Fed will not immediately announce a reduction in bond purchases. But you know, when the Fed suddenly announced the tightening of QE policy in 2013, it also caught the market off guard, and many investors who were heavily positioned in US Treasury longs and short dollars suffered a lot of losses.

As some industry insiders have mentioned earlier, trading activity in the options market is suggesting that the annual meeting of the world central banks in Jackson Hole in August could be one of the windows for the Fed to signal to scale back its buying. The "Eurodollar Whale," which last week bet the Fed would release tightening signals in August, further increased its holdings significantly this week.

And from the Fed's schedule in May, Brown Brothers Harriman & Co. Win Thin, global head of foreign exchange strategy, said investors should carefully analyze the minutes of the Federal Open Market Committee (FOMC), and based on past experience, any clues to the Fed's internal discussions about shrinking bond purchases may appear in these minutes first. The minutes of the April Monetary Policy Meeting will be released on May 19.

"All I can say is that Chairman Powell will do his best not to surprise the market with the decision to scale back the debt purchases," Thin wrote Thursday. "The communication of this signal is expected to be carefully arranged, and the minutes of the meeting are the first places that the market should pay attention to."