Product introduction

There are two kinds of silicone, one is inorganic silicone and the other is silicone.

Inorganic silica gel, that is, silica silica, is described as follows in the national suborder annotation of Tax No. 2811.2210: Silica gel, the chemical molecular formula mSiO2·nH2O, is a porous amorphous amorphous substance with a three-dimensional spatial mesh structure, with a large inner surface area. Transparent or milky white granular solid, insoluble in water and any solvent, non-toxic and odorless, chemically stable, does not react with any substance except strong alkali and hydrofluoric acid.

Silicone gels are generally referred to as silicone compounds, and according to the heading annotation of heading 29.31, the silicon atoms thereof are directly connected to at least one organic-based carbon atom, including organosilanes and siloxanes.

Categorization and analysis

Inorganic silica gels that meet the chemical definition of pure substances (specifically referring to Chapter 28 or Chapter 29 Note I, the same below) are classified as their listed tax number 2811.2210. However, its colloidal dispersions are generally classified under heading 38.24 (except for specific uses), as are inorganic silicone rubbers modified by organic surfaces.

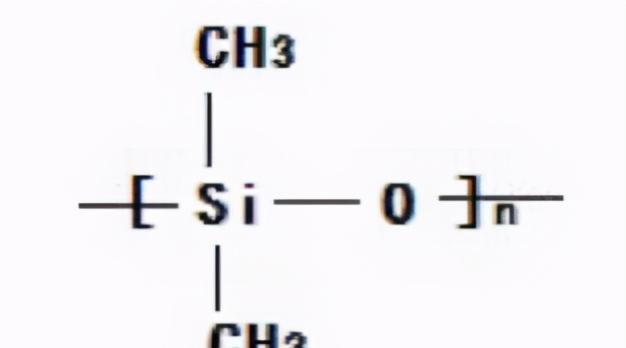

Silicone gels that meet the chemical definition of pures are usually classified under heading 29.31, but polysiloxanes are not chemically defined due to uncertainty in their molecular formula and are classified under heading 39.10. Note that polysiloxanes as defined in the Tariff Notes are organosilanes, which, according to heading 39.10, contain more than one silicon-oxygen-silicon bond in their molecules, and their silicon atoms have organic groups directly connected by silicon-carbon bonds.

Polysiloxanes are often referred to as silicone rubber, but they are still part of a Chapter 39 (plastic) rather than a Chapter 40 (rubber) commodity. In addition, polysiloxanes that comply with the provisions of Chapter 34, Note III, are considered organic surfactants and are classified under heading 34.02 in accordance with the relevant exclusion clauses.

Example 2: Alumina pellets

According to the headings 28.18, alumina (anhydrous or calcined alum) (Al2O3) is made by calcined aluminum hydroxide or obtained from ammonium alum, and is a lightweight white powder, insoluble in water, with a specific gravity of about 3.7.

Alumina that meets the definition of pure substance is classified under its listed tax number 2818.2000, but some alumina containing "impurities" should be subject to specific circumstances.

According to Chapter 28 General Note I, the term "impurity" refers only to those substances that remain in the process of manufacturing (including purification) of a single compound. These substances can remain due to any factors at the time of manufacture, mainly the following: untransformed raw materials, impurities of raw materials, reagents used in the manufacturing (including purification) process, by-products. However, these substances shall not be considered permissible impurities when they are deliberately left in the product with the aim of making the product specifically suitable for certain special uses in addition to having a general purpose.

Chongqing Customs District recently declared a commodity called alumina pellets, which contains a small amount of tin. It has been verified that the tin contained in it is an additive with a specific function, although the content is low, but it cannot be regarded as an impurity, and the commodity should be classified as heading 38.24.

Example 3: Lactam

According to the headings of heading 29.33, lactams are obtained from amino acid dehydration, and a ring of its molecule may contain one or more amide groups, according to the number of amide groups thereof, they are called mono, bis or tri-lactams and the like.

Lactam is a heterocyclic compound, and according to Chapter 29, Sub-Chapter 10 General Notes, a heterocyclic compound is an organic compound consisting of one or more rings that contain other atoms in addition to carbon atoms, such as oxygen, nitrogen, or sulfur, which are often referred to as heteroatoms.

Lactam has a tax number of 2933.7, which is the product with the highest misclassification error rate among heterocyclic compounds, and its related classification principles mainly include the following points:

First, when the heterocyclic only contains nitrogen heteroatoms, it can be classified into item 29.33, and when it contains other heteroatoms in addition to nitrogen, it is usually classified into item 29.34.

Second, unless otherwise specified, when the lactam group coexists with other nitrogen-containing heterocycles, it is classified according to lactam.

Third, unless otherwise specified, laemides that meet the definition of lactam are still classified according to lactam.

Fourth, according to the subheading of subheading 2933.79 (hereinafter the same), lactam containing an additional heteroatomic atom (except for nitrogen atoms containing lactam groups) in the same ring should not be classified into the daughter of lactam.

Fifth, if the amide group is part of two or more rings, and none of them contains additional heteroatoms (except for the nitrogen atom of the lactam group), such a molecule should be regarded as a lactam.

Sixth, the lactam classified into subheading 2933.79 must contain a different lactam group separated by at least one carbon atom at each end. However, the suborder does not include products whose carbon atoms are separated and immediately followed by lactam groups to form oxygen groups, iminos or thio groups.

Example 4 Stearic acid and its salts and esters

According to the heading annotation of heading 29.15, stearic acid is present in fat as a glyceride, white, amorphous, and similar to wax.

According to the headings of item 38.23, commodity stearic acid (stearin), white solid substance, special smell, has a certain hardness, fragility, is beaded, powder or powder when sold, and also transported in isothermal oil tanks after heating, which is liquid when sold.

Stearates are compounds in which stearate ions bind to metal or ammonium ions.

Stearic acid classification factor is mainly purity, and stearic acid with a purity of 90% or more (by weight of the dried product) is classified under its listed tax number 2915.7010, otherwise it is usually classified in its other column tax number 3823.1100.

Stearates differ from stearic acid in that they are classified based on whether they meet the definition of pure substance. If it is met, it is classified as Tax No. 2915.7090; if it is not, it is classified according to its specific purpose, and if it is not listed, it is classified as item 38.24. In addition, according to the relevant exclusion clause, the salts of crude stearic acid are usually classified as headings 34.01, 34.04 or 38.24.

The classification principle of stearate is roughly equivalent to stearate, but there are the following provisions: glycerol monostearate, glycerol bistearate and a mixture of glycerol tristearate, fat emulsifier, if it has the characteristics of artificial wax, should be classified in heading 34.04, otherwise it should be classified as heading 38.24.

It is important to note that, unless otherwise specified, animal and vegetable oils containing stearic acid (bound to glycerol by ester groups) shall be included in Chapter 15, which contains fatty acids in addition to stearic acid.

Example 5: Deuterium-containing compounds

Deuterium, also known as heavy hydrogen, is a non-radioactive isotope of hydrogen atoms, and its most common compound is heavy water, also known as deuterium oxide.

According to the heading annotation of item 28.45, heavy water, in ordinary water, its content is 1/6500. It is usually obtained as a residue of electrolyzed water. Used as a source of deuterium and used in nuclear reactors to slow down neutrons splitting uranium atoms.

The reason why deuterium-containing compounds are prone to misclassification is that headings 28.44 and 28.45 have absolute priority in the classification of goods.

According to Category 6 Note I (i), goods that meet the requirements of subheadings 28.44 or 28.45 (other than radioactive ore) shall be classified separately under those two subheadings and not in the other subparagraphs of this Harmonized System. Among them, item 28.44 is more important than 28.45, and the commodities classified in the former contain radioactive isotopes, while the commodities classified in the latter do not.

According to the above principle, because deuterium is not radioactive, deuterium-containing compounds (which do not contain other radioactive isotopes) are classified under heading 28.45, while tritium, another isotope of hydrogen, is radioactive, so tritium-containing compounds are classified under its listed tax number 28444090.20.

It is worth noting that the heading 28.44 column contains mixtures, while the heading 28.45 column does not. Because most mixtures contain trace amounts of radioactive isotopes to a greater or lesser extent, Chapter 28 Note VI (iv) limits the radioactivity of the mixtures listed in heading 28.44 as follows: Heading 28.44 applies only to alloys, dispersions (including cermets), ceramic products and mixtures containing radioactive elements or isotopes and their inorganic or organic compounds and having a certain radioactive intensity exceeding 74 becquerel/g (0.002 microcurry/g).