Shenzhen Keda rose 11.67%, and the semiconductor equipment ETF (561980) once rose more than 1%, and the institution: the semiconductor cycle reversal is imminent

On the morning of December 11, 2023, the two cities opened low and fluctuated, the three major stock indexes all fell nearly 1%, the semiconductor equipment sector on the disk went against the market, Shenzhen Keda rose nearly 12%, Changchuan Technology and Tianyue Advanced rose 3.76% and 2.17% respectively, and Fuchuang Precision, Tuojing Technology, Huahai Qingke, Huaxing Yuanchuang and other stocks rose more than 1%.

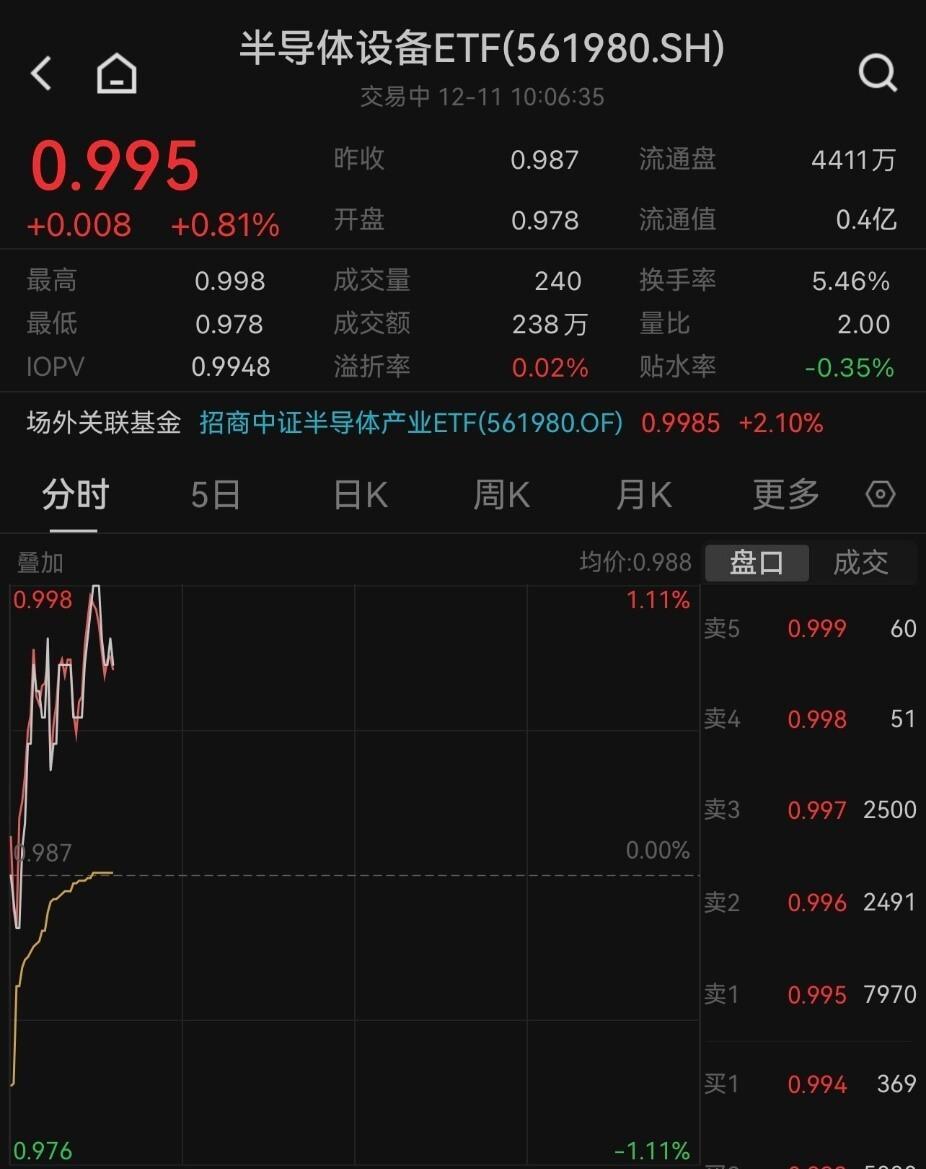

In terms of on-site sub-ETFs, the semiconductor equipment ETF (561980), which focuses on the semiconductor equipment sub-sector, rose rapidly at the beginning of the session, rising by more than 1% at one point and up 0.81% as of this article.

Image source: Wind

The ETF's underlying index mainly covers upstream industry chain companies such as semiconductor materials and equipment, and the semiconductor equipment innovation cycle and domestic substitution cycle are expected to open under the background of the continuous enhancement of the main theme of semiconductor autonomy and controllability, the bottoming out of the cycle, and the new demand catalyzed by AI.

On the news side, the underlying index of the recent semiconductor equipment ETF ushered in the rebalancing of positions and shares in December, with the addition of 5 shares such as Jinhaitong, Haiguang Information, Huahai Qingke, Luwei Optoelectronics and Fuchuang Precision, and the exclusion of Jingsheng Electromechanical, GigaDevice Innovation, Ziguang Guowei, Jiejia Weichuang, China Resources Micro and other 5 shares.

Data source: official website of China Securities Index

From the perspective of industry fundamentals, after the "darkest moment", semiconductors "shimmered".

Recently, the World Semiconductor Market Statistics Bureau (WSTS) revised its 2024 forecast upward, revising the global semiconductor sales estimate in 2024 from the previous estimate of US$576 billion (June 6) to US$588.4 billion, an annual increase of 13.1%, surpassing the US$574.084 billion in 2022 and setting a record high.

SIA, the semiconductor industry association, expects year-end sales in 2023 to be lower than in 2022, but the global semiconductor market is expected to rebound strongly next year, achieving double-digit growth.

CICC's latest view says that the A-share small-cap style is expected to continue to prevail, and it is recommended to pay attention to the semiconductor industry chain. Combined with the current macro environment and liquidity and other factors, the A-share small-cap style is expected to continue to dominate, but it is necessary to pay attention to the degree of valuation differentiation of the small-cap style and the impact of subsequent policy settings on economic expectations. At the industry level, it is recommended to pay attention to the investment opportunities in the semiconductor industry chain and the smart car industry chain.

The latest strategic view of China Securities Construction Investment believes that the semiconductor cycle is about to reverse, and terminal innovation and AI will lead a new round of growth. With the support of terminal innovation and AI empowerment, the electronics sector is expected to enter an upward channel in 2024. In terms of terminal innovation, the recovery of mobile phones and PCs, the shipment of folding screen mobile phones and XR is expected to grow rapidly, the penetration rate of OLED is increasing, and AI mobile phones and AI PCs are expected to catalyze consumer demand and drive the growth of related supply chains. In terms of AI empowerment, AIGC has triggered a paradigm revolution in content generation, with strong demand for computing power, a shortage of GPUs, HBMs, etc., and domestic computing power, storage, and corresponding advanced processes and advanced packaging have benefited. At present, semiconductor inventories continue to deplete, and some sectors such as storage and CIS have bottomed out, and demand is expected to pick up in 2024.

Semiconductor Equipment ETF (561980) passively tracks the CSI Semiconductor Industry Index, which mainly covers upstream industry chain companies such as semiconductor materials and equipment. The upstream semiconductor equipment and materials have high industrial barriers, and many fields are backward, which is the main battlefield of domestic substitution, with broad development space, and continues to be highly valued and supported by the national industrial policy. Under the background of the continuous enhancement of the main theme of semiconductor autonomy and controllability, the bottoming out of the cycle, and the new demand catalyzed by AI, the semiconductor equipment innovation cycle and domestic substitution cycle are expected to open.

The content and data of this information source are for reference only and do not constitute investment advice. AI technology strategy is provided for Youlian Cloud.