What is the probability of the bottom of the A-share market? What are the main lines of investment? Here comes the top 10 brokerage strategies

Finance Associated Press, October 29 (edited by Ruoyu) The latest strategic views of the top ten brokerages have been released, as follows:

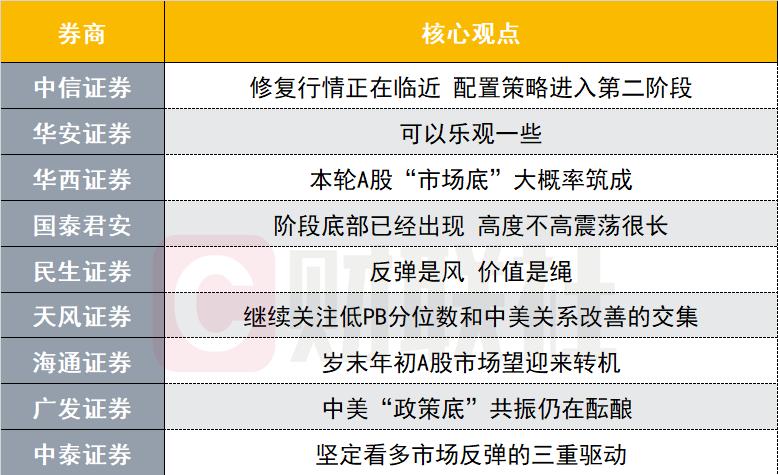

CITIC Securities: The repair market is approaching the second stage of the allocation strategy

In November, the financial exceeded expectations to accelerate the process of economic repair, the liquidity influencing factors at home and abroad began to ease, the quasi-"leveling" role played by Huijin's increase in holdings appeared, the risk appetite of market funds began to increase, the bottom of the market has been consolidated, and the repair market is approaching.

In terms of industry allocation, November is about to enter the second stage of the "three-stage strategic layout", and it is recommended to actively deploy technology and pharmaceuticals with large declines in the early stage. The medical advice focuses on innovative drugs and overseas varieties; In the direction of independent and controllable science and technology, it is recommended to closely track the potential breakthroughs in AI applications and the localization process of semiconductors; In the pro-cyclical direction of science and technology, it is recommended to pay attention to the improvement of residents' terminal consumption, the promotion of orders for consumer electronics, intelligent driving manufacturers and parts, and the expected increase in government and enterprise spending in the future will bring about a reversal of the dilemma of software, security and other industries in 2024.

Huaan Securities: We can be optimistic

With the recent increase in the issuance of treasury bonds and the increase in the deficit ratio, the Shanghai Stock Exchange rebounded at the end of the month and recovered 3,000 points. Looking ahead to November, positive factors continue to accumulate, and A-shares are expected to rebound with clearer support. The main changes include the gradual implementation of domestic policies, focusing on the market's expectations for the Central Economic Work Conference, and the continued high volatility of U.S. bond interest rates but it is difficult to rise rapidly; The macroeconomic data in October may be affected by base disturbances, but the economic recovery continues to improve; The domestic easing remains unchanged, and with the issuance of fiscal bonds, the probability of a RRR cut in November is high, and there is some room for interest rate cuts.

In terms of industry allocation, it is recommended to pay attention to the rebound of growth industries with potential, including electronics and communications, which have benefited from the repeated fermentation of Huawei's chain catalysis, power equipment with increased value after the overfall, and pharmaceutical and biotechnology with obvious inflection points at the bottom of valuation and medium- and long-term investment expectations. As well as focusing on the marginal improvement of the economy and the financial style recognized by the market to increase holdings, including banks and non-bank financial sectors, they can increase allocation.

Huaxi Securities: There is a high probability that the "market bottom" of this round of A-shares will be built

According to multi-dimensional indicators such as valuation and price comparison of major assets, market trading sentiment and investor behavior, the bottom of this round of A-shares may have been built. The following three positive factors are expected to drive the market to the upside: first, the recent high-level interactions between China and the United States have frequently released warmth, and if the two heads of state meet at the APEC summit, it will further improve the market's risk appetite; Second, the active fiscal force at the end of the year means that the demand of the policy level for the economy is increasing, and a number of important meetings will be held in China in the future, and the implementation of incremental policies is worth looking forward to; Third, Central Huijin's increase in holdings is expected to continue, while the net reduction of holdings in the secondary market has slowed down and listed companies have intensively repurchased, and the micro liquidity of A-shares has improved.

In terms of style, under the pattern of stock funds, the market style will not be "switched" in the short term, and it will be more manifested in the rotation of the industry. In terms of allocation, the low valuation dividend is used as the ballast stone, and at the same time, we will pay attention to Huawei's industrial chain, which has benefited from the recovery of local substitution and demand, and the pharmaceutical industry, which has adjusted its valuation to a historically low level and improved policy expectations.

Guotai Junan: The bottom of the stage has appeared, the height is not high, and the oscillation is very long

The stage bottom has appeared, and the rebound momentum comes from the new expectations of the policy outlook and the correction of the previous pessimism, bringing short covering and a technical rebound. The core contradiction of market operation has not changed much, and the index judgment maintains the view that "the height is not high and the volatility is very long". In addition, benefiting from the stabilization of Sino-US relations and the demand for overseas replenishment, domestic high-end manufacturing and emerging consumer exports are expected to accelerate.

It is recommended to pay attention to: 1. High-end equipment: layout of key machines and parts localization, and recommend semiconductors (Zhongke Flying Measurement/Tuojing Technology)/energy equipment (Dongfang Cable/Daikin Heavy Industries benefit); 2. New materials: The application of titanium alloy in the field of electronics is accelerating, and key basic materials lead the development of emerging industries, and 3C new materials with industrialization foundation (Everbright Tongchuang/Genesis)/semiconductor materials (Anji Technology/Guanggang Gases benefit); 3. Huawei's industrial chain: Smart models have entered an intensive release period, and the demand for domestic computing power has increased, which is recommended (Rayhoo Mold/Digital China); 4. Export chain: textile and clothing retail and cross-border e-commerce benefiting from the rebound of overseas demand and new consumption trends (Huali Group/Huakai Yibai).

Minsheng Securities: The rebound is the wind and the value is the rope

This week, the market ushered in the expected repair market under the background of the weakening of domestic medium and long-term problems and the same marginal easing of overseas liquidity, but under the multiple games, the market does not seem to show an obvious main line, and the pro-cyclical and growth market has been staged repeatedly. At the beginning of the fundamental expected repair market, the market has reached the bottom of various assets because of the long-term decline, and all kinds of game logic seem to have tenable reasons, so there is a certain rationality in the acceleration of the industry rotation speed, but even if all kinds of assets face the same positive drive, the future may face different resistance. The market is like a kite, if the rebound is the wind, then the value is the rope.

Commodity-related assets (copper, aluminum, oil, oil transportation, precious metals, coal) may be the link with a real profit advantage in the future; In the growth rebound, the relative advantage can consider the new energy industry (lithium battery, photovoltaic, vehicle) and military industry; The financial sector has obvious excess returns (banks, insurance, brokerages) during the period of bottoming out fundamentals, and as the current round of economy is more based on the recovery of production flows, dividend assets can also be deployed at this time.

Tianfeng Securities: Continue to pay attention to the intersection of low PB quantiles and the improvement of Sino-US relations

The issuance of special treasury bonds dispelled some pessimistic expectations: "In the past, everyone was worried that there would not be too many policies to stabilize growth in China under the condition of high U.S. bond interest rates, continued high pressure from the Federal Reserve, and great pressure on the depreciation of the RMB exchange rate." At the same time, the CSI 300 and the Hang Seng Tech Index have some room for repair, similar to around October 13. However, it is necessary to observe the GDP target and the strength of urban villages in the follow-up before it is possible to look forward to the main upward wave of PMI, ROE and CSI 300 and Hang Seng Tech Index.

With the disclosure of the third quarterly report basically over, the boots with poor performance have landed, and we will continue to pay attention to the intersection of low PB quantiles and the improvement of Sino-US relations: consumer electronics semiconductors, CXO innovative drug industry chain, and new energy vehicles.

Haitong Securities: The A-share market is expected to usher in a turnaround at the end of the year and the beginning of the year

Judging from the current round of situation, since the end of last year, the bond market and high-dividend stocks have risen successively, which may indicate that the market has been at a stage bottom. Looking ahead, the recovery of fundamentals and favorable policies are expected to provide support for the market at the end of the year and the beginning of the year. The market is expected to usher in two catalysts to open the market: first, Sino-US relations are expected to improve, on the afternoon of October 25, President Xi Jinping met with California Governor Newsom in the Great Hall of the People, and the first meeting of the Sino-US financial working group was held by video on the same day, and then the high-level leaders of China and the United States are expected to meet at the APEC meeting in November, and there may be more positive changes in the relationship between the two sides in the future, which will help boost market risk appetite; On October 23, following the announcement of the increase in holdings of the four major banks, Central Huijin announced that it would increase its holdings of ETFs on the same day, and the continued entry of related funds is expected to boost investor confidence, and the follow-up may drive more funds to enter the market.

In the context of continuous policy efforts, we believe that there may still be opportunities in traditional industries, among which from the perspective of allocation, the allocation of public funds to the large financial sector is still low, and the valuation is still at a historically low level, and it is expected to further usher in recovery in the future; At the same time, the excess returns of the technology sector in the early stage have converged, and the allocation value is gradually emerging. In addition, the pharmaceutical and consumer goods sectors have a cost-effective allocation.

GF Securities: The resonance of the "policy bottom" between China and the United States is still brewing

The domestic policy foundation has been consolidated, and the fiscal easing signal (government leverage) is an effective way to repair the balance sheet problems of Chinese residents/enterprises, which will help consolidate the confidence of the profitability of the molecular end enterprises. The resonance of the "policy bottom" between China and the United States is the last link to confirm the bottom of the A-share market, and the overseas risk off has not yet been fully formed, and the big opportunity for the resonance reversal of the policy bottom between China and the United States is still brewing.

At present, A-shares are in the window period of "(1) the right side of the domestic policy bottom + (2) the economic stabilization has not improved significantly + (3) overseas liquidity pressure", and the "valuation gap" is likely to continue to converge, and the low valuation is more beneficial. 2. Long-term science and technology singularity certainty - digital economy AI+: semiconductors, optical modules, games; 3. Certainty of sustainable operation - high dividend yield & high free cash flow: coal, petroleum and petrochemical, electricity.

Zhongtai Securities: Firmly bullish on the triple drive of the market rebound

On the basis of the expectation of the China-US summit and the expectation of the equalization fund to enter the market, the right side of the rebound driven by the expectation of the China-US dollar summit has been basically established, and the policy signal revealed by the central fiscal policy within the framework will make the time and space of this round of rebound be high, and this round of over-falling rebound will be further expanded and adjusted in level, time and space. At present, the central government is still appropriately raising the deficit ratio on the basis of the principle of "determining expenditure by revenue", and has maintained the strength of the framework. The subsequent introduction of policies such as increasing leverage and promoting consumption needs to have the impact of the risk of fundamentals exceeding expectations. The level of this round of rebound may not only be a new high in the past six months, but also the most important market in the next six months, and it is recommended to actively seize the opportunity of this round of rebound.

In terms of allocation direction, the first stage of the index rebound will focus on "over-falling + weight", that is, Hang Seng Technology, non-bank, new energy + pro-cyclical, it is expected that the transformation of urban villages around young tenants early next year will also be increased by the central government, and the building materials sector may relatively benefit; After the index experienced an over-falling rebound, the market may once again enter the structural market stage, and it is recommended to allocate sectors such as military industry, information innovation, and power grid construction that are expected to be optimistic about industrial policies; After the market rebounded from over-falling to structural market transition in the fourth quarter, it is necessary to pay attention to defense in the process of allocation next year, and it is recommended to pay attention to high-dividend sectors such as medicine and electricity.

Industrial Securities: Two paths out of the bottom

Whether it is from the path of incremental funds to break the negative feedback, or from the path of the expected spontaneous correction and reversal, the current market positive signals are accumulating. Therefore, we tend to believe that the market is expected to have a repair opportunity in the current bottom area in Q4.

In terms of industry allocation, it is recommended to attack the high prosperity, take the dividend and low wave as the bottom warehouse, lay out the inventory cycle, and lay out along the three main lines. The first is to pay attention to the recovery opportunities of value sectors such as the cycle (building materials, chemicals, industrial metals, construction machinery) and consumption (textiles and garments, snack foods, liquor) that have benefited from policy promotion and fundamental improvement in the near future, and continue to grasp the high economic growth (automobiles, semiconductors, media); The second is to focus on petroleum and petrochemical, operators, insurance, power and transportation, and high-quality central state-owned enterprises in the fields of Hong Kong stock telecom operators, energy (oil, coal), public utilities and other fields also have strong high dividend allocation value; The third is to pay attention to the optional consumption sector, that is, household appliances (kitchen appliances, white goods), automobiles (commercial vehicles, auto parts), light industry manufacturing (household goods, entertainment products), etc., TMT sector (publishing, advertising and marketing, optics and optoelectronics) and military electronics, decoration and building materials, chemical fibers, etc.

(Finance Associated Press Ruoyu)

![Agitated! The mortise and tenon craft will be on the moon "News Fast Food" for three minutes a day, taking you to a quick overview of the world[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)