A share red October can be expected! The top ten institutions interpret the fourth quarter market

In September, affected by many factors, the three major A-share indexes fluctuated. While the Fed did not raise rates, Powell said he was prepared to raise rates further if appropriate.

Before the long holiday, the market went decent. For October, institutions are generally optimistic, and the consumer, technology and other sectors are optimistic about institutions.

Top 10 institutions interpret the future market

AVIC Securities: Look at the bulk in September, and look at consumption in October

Dong Zhongyun, chief economist of AVIC Securities, said that the rebound in commodity prices may be beneficial to the third quarter performance of upstream resource goods companies. In late August, the market may expect the demand side to accelerate the recovery driven by the domestic real estate chain and industrial production, thereby raising the price of ferrous and industrial metals. Under the repair of economic momentum, residents' willingness to increase leverage to buy houses and borrow for business and consumption purposes has recovered from July.

The A-share profit cycle may have started to recover, and the improvement of PPI data shows that the growth rate of A-share profit is expected to improve simultaneously, and it may be a positive layout period now. It is expected that the upward trend in commodity prices since June is expected to be reflected in the third quarter results of upstream resource goods companies, and the cyclical industry is expected to continue its strong performance under the background of market trading returning to the main line of performance. In the short term, it is recommended to pay attention to the more active consumer sectors around the November holiday in the past decade.

Everbright Securities: There is a high probability of good performance after the holiday

It is expected that the A-share market will perform well after the National Day this year. On the one hand, historically, affected by liquidity changes, A-shares are likely to rise after the National Day. On the other hand, the current market is at a relatively low level, investment is cost-effective, and the policy of activating the capital market and stabilizing the economy is also gradually promoting the overall index is easy to rise and fall, and the direction is expected to gradually fluctuate upward. On the whole, it is expected that A-shares will also have a good performance after the National Day this year.

Galaxy Securities: Continued the style of the third quarter

Looking forward to the fourth quarter, the domestic economic growth rate is expected to continue to improve, the differentiation of domestic and foreign policy interest rates will increase slightly, and on the whole, the fourth quarter is more likely to continue the style of the third quarter.

Looking forward to the fourth quarter: (1) the industries with high performance growth rate, low valuation, and greater possibility of future return of northbound funds are: power equipment, food and beverage, national defense industry, public utilities, transportation and other industries; (2) The effect of the previous policy has gradually emerged, and there are still transactional opportunities in the non-bank financial and real estate chains; (3) The overall valuation level of the consumer sector is at a low level, and the consumption potential in the fourth quarter is expected to be further released, and the performance of some consumer industries is expected to continue to improve; (4) It is recommended to pay attention to the upstream energy sector, petroleum and petrochemical, coal and other industries that benefit from the rise in international energy prices in the short term; (5) It is recommended to pay attention to the TMT and domestic technology sectors with high allocation value in the medium and long term.

Sichuan Finance Securities: A-shares are expected to stabilize and recover

Chen Yi, chief economist and director of the research institute of Sichuan Finance Securities, said that at the macro level, the domestic macroeconomic recovery trend has not changed, and corporate profits will gradually recover; From the perspective of liquidity, while continuing to raise interest rates overseas and maintain high interest rates, China has always maintained loose monetary policy, liquidity is relatively abundant, and overseas disturbances are expected to ease.

At the valuation level, the overall valuation of A-shares is already at a relatively low historical level, which has a high allocation value; At the market level, many departments have successively introduced a "combination fist" since August to promote market activity, and with the continuous support of policies, A-shares are expected to stabilize and recover.

Chen suggested focusing on three major areas: first, traditional energy sectors such as coal and crude oil, where the continuous rise in energy prices and the stable performance and dividend rate of the industry have a high allocation value; Second, the digital economy related sectors, the development of digital economy is a strategic choice to grasp the new round of scientific and technological revolution and industrial transformation new opportunities, how to realize the digital economy to empower the industry is the focus of current economic work, the industry has a large space for development; Third, the banking sector, historical data, the fourth quarter of the banking sector is often prone to excess returns, and with the improvement of real estate policies, the risk transmission of real estate to the banking system has gradually slowed down.

Ping An Securities: The overall opportunity outweighs the risk

Ping An Securities believes that the current market is in the bottom area, the marginal stabilization of the economy and the continuous efforts of policies are expected to bring further improvement in market expectations, and the overall opportunities outweigh the risks.

Structurally, on the one hand, it is recommended to pay attention to the financial, real estate and consumer sectors that benefit from favorable policies, and as the fourth quarter approaches, the value blue-chip sector allocation cost-effective with high dividends and low valuation is gradually highlighted; On the other hand, the domestic technology industry still continues to be prosperous, and the TMT (technology, media and communications) sector is relatively more certain in the medium and long term.

Guosheng Securities: October is expected to usher in a repair

At present, the market is in the stage of consolidating the bottom, whether from the perspective of valuation or stock-bond income ratio, it is recommended to strengthen confidence, remain optimistic, and wait for changes. With the steady recovery of the macroeconomy and the emergence of more positive signals, the October market is expected to come out of the bottom and usher in repair:

1. Under the recent intensive increase in policy easing, the real estate market has shown signs of marginal improvement; 2. The recent depreciation pressure on the RMB and the rise in US interest rates have also eased the adverse factors leading to northbound outflows; 3. Monetary easing is still the general direction, there may still be room for interest rate cuts during the year, and the supply and demand pattern of market capital will continue to improve in the future; 4. As the congestion of TMT, consumption and other sectors falls back to historical lows, it will be easier for the market to form an upward synergy once the market warms up.

Strategically, focus on the recovery chain and the direction of technology growth: it is recommended to grasp sectors with high certainty such as consumption, such as tourism hotels, pharmaceuticals, home appliances and other directions; Focus on hard technology sector opportunities with long-term investment value, such as digital infrastructure with policy efforts, artificial intelligence under technological change and other fields.

China Merchants Securities: The fourth quarter is expected to usher in a major turnaround

After experiencing the adjustment from the second quarter to the third quarter, A-shares ushered in an upward inflection point in fundamentals, liquidity and policy. The pressure of external liquidity is gradually released, and foreign capital is expected to return to the inflow trend in the fourth quarter.

A-shares are expected to usher in a major turnaround in the fourth quarter, interpreting the last upward trend of the N-shape. At the style level, the logic of the growth of the broader market in the fourth quarter is stronger, and at the industry level, from the perspective of economic recovery, industrial trends and foreign investment preferences, electronics, computers, home appliances, automobiles, pharmaceuticals and other industries are worth paying attention to.

Bohai Securities: The layout of the fourth quarter is timely

The performance environment of A-shares will usher in a bottom improvement process, and the bottom of the fundamentals has been basically confirmed, considering the superposition of the replenishment cycle in the later period, which will promote the continuous recovery of fundamentals.

For the grasp of industry allocation in the fourth quarter, under the background of the initial stabilization of economic fundamentals, on the one hand, we can pay attention to the thematic opportunities under the stability of the performance side to promote the market risk appetite, and the other is the policy game opportunities of the "real estate chain" and the large financial sector; The second is the TMT sector catalyzed by new industrialization and Microsoft's large model. On the other hand, you can pay attention to the possible valuation switching market at the end of the year, and with the repair of performance expectations, the consumer sector, which is already at a low level of valuation, is expected to start the valuation switching market at the end of the year.

Wanlian Securities: Grasp the opportunity of the allocation window

Boosted by a number of favorable policies, A-shares are expected to gradually come out of the weak shock stage. It is recommended to seize the opportunity of the allocation window period and actively layout the industry, it is recommended to pay attention to: 1) the non-bank financial and real estate sectors that are expected to improve the fundamentals of the industry and recover from the low prosperity under the favorable policies; 2) Leading enterprises with higher performance growth expectations in the themes of scientific and technological innovation and digital economy in the growth style are preferred.

Zheshang Securities: The policy is expected, and the market is gradually warming up

The wind deviation is improving, grasp the window period. October Gold Portfolio: Non Bank: Huatai Securities; Electronics: Vijie Chuangxin; Electronics: Hudian shares; Computer: Kingsoft Office; Computer: iFLYTEK; Communications: Jiaxun Feihong; Dianxin: Yijiahe; Machinery: Shanghai Yanpu; Agriculture: Sunnong Development; Social service: Chongqing Department Store.

The "calendar effect" attracts attention

There has always been a "calendar effect" in A-shares.

In the past decade, funds have shown a hedging tendency before the November holiday, and the turnover of the two cities is at a relatively low level; After the holiday, trading rose and the market rebounded.

From a historical point of view, A-shares have seen many "red October" markets in October, and the probability of the Shanghai Composite Index rising from 2010 to October 2022 is 62%.

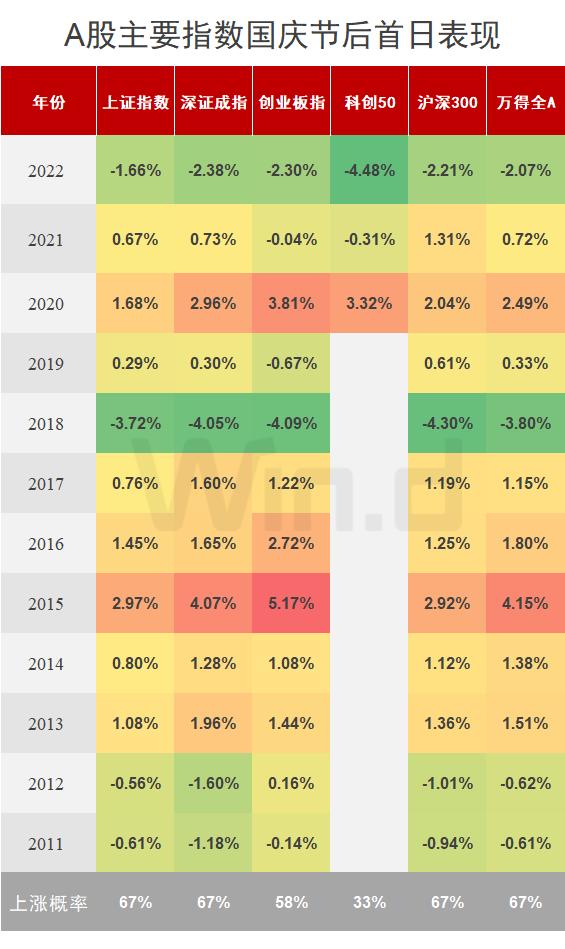

According to Wind data statistics, the performance of the main A-share index on the first day after the National Day is as follows:

Consumption and growth rose at the top of the list

In August, the profits of industrial enterprises above designated size turned from decline to increase, the economy was significantly repaired, and the general trend was improving.

According to Wind data, the 5 trading days after the November holiday performed the best, with consumption, growth, and cycle growth first. As stock indices rebounded after the holiday, average yields across the vast majority of sectors were positive.

In 2023, the popularity of tourism consumption during the November Golden Week will increase significantly compared with the same period of previous years, and the popularity of the consumption sector is expected to continue.

TF Securities is optimistic about the investment opportunities in the liquor sector under the irreversible trend of consumption upgrading in the industry, considering (1) the performance of sales / inventory / wholesale price during the Mid-Autumn Festival National Day; (2) poor performance expectations in 23Q3; (3) Changes in domestic and foreign policies & economic expectations are the core catalysts of the current plate, and it is recommended to pay attention to three main lines: (1) the operation is at a relative bottom type target: Wuliangye/Shuijingfang, etc.; (2) Or enjoy the main line of valuation switching dividends (strong α): Kweichow Moutai / Luzhou Laojiao / Shanxi Fenjiu / Jinshi Yuan / Yingjing Tribute Wine, etc.; (3) It is recommended to pay attention to the main line of strong β: drunkard wine/shede liquor, etc.

Nanjing Securities said that this year's holiday concentrated travel characteristics have become more prominent, various tourism products have attracted high attention, and travel demand such as summer escape, study and health care is expected to become an important support for the growth of the summer tourism market. In addition, the holding of various performing arts and performance activities has also significantly promoted the comprehensive consumption of transportation, accommodation, catering and so on in addition to the box office of the performance.

Focus on companies related to the scenic spot performing arts industry with strong performance delivery ability and catalyzed by holiday travel: the head hotel group accelerates its expansion with strong brand power and organizational management capabilities, further increases its market share, and pays attention to the beneficiaries of the upward cycle of the industry: Jin Jiang Hotels and BTG Hotels; With the rise of civilian consumption, traditional scenic spots are exploring new opportunities for growth through content innovation, live streaming and drainage, cultural and creative products, etc., including Emeishan A, Qujiang Cultural Tourism, Huangshan Tourism, Tianmu Lake, Changbai Mountain, etc. The recovery of inbound and outbound tourism supply has accelerated, and the recovery of inbound and outbound tourism in the second half of the year is expected to accelerate.

(Comprehensive CBN, Securities Times, etc.)