(Text/Li Pengtao Editor/Ma Yuanyuan) As the number of cats and dogs increases year by year, the mainland pet economy has also ushered in rapid growth, of which the market size of pet food has increased from 15.7 billion yuan in 2012 to 128.2 billion yuan in 2021.

In this context, various capital branches have entered the market, and related enterprises have successively rushed to the capital market. In addition to the A-share listed zhongpet shares, Petty shares, Lusi shares and other enterprises, Baobao Pet will also be the first meeting on July 27, and it is proposed to be listed on the ChiNext board.

In this listing, Qibao Pet will raise 600 million yuan, of which 367 million yuan will be used for the expansion and construction project of pet food production base, 71.9105 million yuan for intelligent warehousing upgrade project, 30.6048 million yuan for R&D center upgrade project, 25.1126 million yuan for information upgrading construction project and 105 million yuan for supplementary working capital.

It is worth noting that the capacity utilization rate of Baobao's pet staple food products is less than 70%, and the company's inventory of goods nearly doubled last year, but it needs to use 60% of the raised funds to expand production capacity. For whether there is blind expansion and other issues, the observer network contacted the baby pet, as of press time has not received a reply.

At present, the production capacity of the two major production bases of Baobao Pet in China and Thailand has exceeded 100,000 tons, and the company's inventory of goods has nearly doubled from 132 million yuan in 2020 to 259 million yuan.

On the black cat complaint platform, there are 141 complaint records of The Pet's own brand "McFudi" pet food, involving false publicity, product safety/quality issues, etc., of which many consumers said that "pets get sick or die after eating McFudi products". On platforms such as Xiaohongshu, some consumers have also complained about the quality of McFudy's pet food.

In fact, the safety of pet food is an untouchable bottom line for pet owners. A number of pet owners told the observer network, "When you just have a pet, you will refer to the recommendations of users on the social platform when you choose food for your pet, and if you see feedback from a brand that has quality problems, there is a high probability that you will not buy the brand's food for your pet." At the same time, when the economic situation allows, foreign high-end brands are preferred. ”

It used to be an "OEM" foundry

Founded in 2006, Baobao Pet is an enterprise engaged in the research and development, production and sales of pet food, mainly engaged in pet dogs and cats.

At the beginning of its establishment, Baobao Pet mainly processed pet snacks such as chicken jerky for overseas pet food brands. Up to now, the "OEM" products of Baobao Pet are mainly sold to more than 30 countries and regions such as Europe, America, Japan and South Korea, and the customers include wal-mart, Pinpu, Smark and other large retailers and well-known pet brand operators.

Until 2013, based on the experience of oem work for overseas customers for many years, Qibao Pet began to create its own brand "McFudi", laying out the domestic pet food market and selling directly to C-end consumers. In 2021, the company will enter the high-end pet food market by acquiring the American brand "Waggin'Train" and the new Zealand brands "K9Natural" and "Feline Natural".

Why do you want to create your own brand seven years after your company was founded? In fact, in early 2013, the US FDA detected antibiotic residues in chicken jerky snacks produced in the mainland, some large supermarkets in the United States reduced the import of chicken meat pet snacks, and the mainland exported pet snacks to the United States also decreased year by year.

At that time, the mainland pet food industry was in a transitional stage from a period of growth to a period of rapid development. Between 2000 and 2014, pets in the mainland gradually transformed from "functional" roles to "emotional" roles, and with the development of the Internet, the first batch of online pet service platforms in China rose.

In the subsequent time, with the continuous development of the Guoming economy and the increase in per capita disposable income, people regard cats and dogs as relatives and friends more, and the demand for refined pets has increased.

According to the white paper on China's pet industry, the market size of pet food in mainland China will grow from 15.7 billion yuan to 128.2 billion yuan from 2012 to 2021, with an average annual compound growth rate of 26.3%, far exceeding the global average of 6.2%.

With exports blocked and the domestic pet market in a transitional stage, Qin Hua, founder of Qibao Pet, stepped onto the train of pet economic development.

Although Baobao Pet has long been transformed from "OEM" OEM processing to production and sales of its own brand, in the company's current revenue share, the "OEM" business with low gross profit still accounts for nearly 50%.

From 2019 to 2021, the revenue of the pet processing business was 694 million yuan, 1.001 billion yuan and 1.186 billion yuan, accounting for 49.6%, 50.45% and 46.33% of the total revenue, respectively; During the same period, the gross profit margin of the business was 21.49%, 26.57% and 24.22%, respectively.

In the same period above, the revenue of private brands was 706 million yuan, 993 million yuan and 1.33 billion yuan, accounting for 50.4%, 49.55% and 51.95% of the total revenue, and the gross profit margin was 36.15%, 39.79% and 40.82% respectively.

BaoBao Pet mentioned in the prospectus, "The overseas market is an important source of the company's operating income, the company adopts the OEM/ODM model to produce pet food for overseas customers, the demand for labor resources is large, the homogenization of similar manufacturers' products is high, and emerging economies such as Thailand and Vietnam may gain greater advantages in the competition of the pet food market with their low labor costs, and there is a risk of intensified competition in the overseas market in overseas business." ”

The money-burning marketing model is not sustainable

Overall, the revenue growth rate of Baobao pets showed a downward trend. From 20109 to 2021, the company achieved revenue of 1.403 billion yuan, 2.013 billion yuan and 2.575 billion yuan, and its revenue growth rate fell from 43.48% in 2020 to 27.91% in 2021.

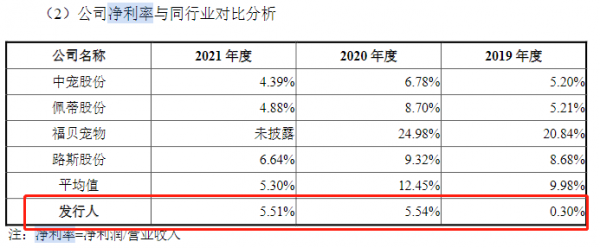

At the same time, the sustained profitability of The Baby Pet is not stable. In the same period above, the company's net profit was 4.1602 million yuan, 111 million yuan and 140 million yuan, and its net profit margin was 0.3%, 5.54% and 5.51% respectively. The net profit margins of peer pet shares, Petty shares and Faube pets in 2020 will reach 6.78%, 8.7% and 24.98% respectively.

Baobao Pet explained this, "The difference in net interest rate between the company and Bei Company is mainly the difference in product structure and the difference in sales expense input; The differences with Zhongpet shares, Petty shares and Luce shares are mainly the difference in selling expenses; The company's domestic private brand revenue accounts for a relatively high proportion, so the marketing expenses are higher. ”

Since the sales of Baobao Pet's own brand mainly rely on online channels, the company's own brand "McFudi" online channel revenue has accounted for 84% in 2021, which also means that it needs to invest huge sales expenses. From 2019 to 2021, the company's sales expenses were 246 million yuan, 341 million yuan and 459 million yuan, respectively, and the total expenditure in the three years was 1.046 billion yuan, more than three times the total net profit of the three years.

Among the sales expenses, the investment in business publicity expenses was the largest, with 79.0157 million yuan, 124 million yuan and 1.73 yuan respectively invested in the same period, accounting for 32.13%, 36.46% and 37.72% of the total sales expenses.

According to the prospectus, Baobao Pet invited Nicholas Tse, boy band member Yin Haoyu, and Korean band member Lee Baht as image spokespersons, and cooperated with CCTV's "Hello Life", Hunan Satellite TV's "Friends Please Listen Well", "Longing for Life" and "Thirty Only", "Love Special Soldiers" and other variety shows, and also cooperated with bilibili, Little Red Book, Douyin, Kuaishou and other platform KOLs to enhance the company's brand influence.

Although considerable sales have been obtained through overwhelming marketing, it is difficult to precipitate into brand stickiness, and the model of relying on burning money to maintain high growth is difficult to sustain in the medium and long term.

At present, among the top 10 cat food brands in the domestic market share, the market share of imported cat food brands has continued to increase, from 12.1% in 2017 to 15.5% in 2021; Among the top 10 dog food brands in terms of domestic market share, the market share of imported dog food brands has decreased year by year, from 11.60% in 2017 to 8.20%.

According to the data of China Pet White Paper, nutrition ratio (55.1%) and ingredient composition (46.5%) are the two major decision-making factors for pet owners to choose staple foods.

In terms of price, foreign high-end imported brands are above 100 yuan per kilogram, while most domestic brands are at 50 yuan per kilogram.

Guoyuan Securities pointed out that high-end imported brands have created their own competitive barriers by virtue of their advantages in formulas, raw materials, process technology, etc., and avoided the low-level price band with a relatively crowded competitive environment.

The company's own brand pet snacks, staple foods and health products are mainly positioned in the mid-end market, and the average selling prices of the company's own brand pet snacks, staple foods and health care products in 2021 are 45.3 yuan / kg, 11.25 yuan / kg and 45.21 yuan / kg respectively.

"We believe that high-end is a difficult and correct path, only through high-end, local pet food brands can shape the real brand power, so as to break through the industry's internal rolls and overseas giants suppression, and then enjoy the long-term dividends of industry development." Guoyuan Securities said.

In the prospectus, the company has begun to focus on the high-end market in recent years, and will use the IPO funds to invest in the construction of R&D center upgrade projects to provide conditions for the company to develop high-end products. It should be noted that the investment plan of the project accounts for only 5.1% of the 600 million raised funds.

At present, the production capacity of the two major production bases of Baobao Pet in China and Thailand has exceeded 100,000 tons, and the company's inventory of goods has nearly doubled from 132 million yuan in 2020 to 259 million yuan.

The expansion and construction project of the pet food production base that Qibao Pet intends to invest in accounts for 61.23% of the total fundraising, and the expansion project includes expanding the manufacturing capacity of 58,500 tons of staple grains, 3133 tons of snacks and 1230 tons of high-end health care products. Does the company really need to expand so much capacity?

This article is an exclusive manuscript of the Observer Network and may not be reproduced without authorization.