The May 2022 Fed interest rate meeting announced a 50 basis point rate hike and launched a balance sheet reduction in June, which is basically in line with market expectations. Fed Chairman Powell's speech dispelled the market's concerns about a faster rate hike in the future (single 75bp), and showed a high degree of flexibility in the path of interest rate hikes, and the market felt "dovish". Considering the signal released by the Fed this time, as well as the recent easing of core inflation in the United States, the hidden worries of economic growth and employment, and the tightening of financial conditions, we believe that the Fed's most "eagle" period may be passing, and the corresponding impact on the allocation of large-scale assets is worth paying attention to.

On May 4, 2022, US time, the Federal Reserve announced the statement of the May FOMC meeting, and Fed Chairman Powell was interviewed. After the announcement of the meeting, the market reaction was not large. After Powell's speech, the market reacted positively: the US Treasury yield fell sharply by 10bp to 2.90% in 10 years; the US Nasdaq, S&P 500 and Dow Jones Industrial Index closed up 3.19%, 2.99% and 2.81% respectively; the US dollar index plunged from a high of 103.4 to around 102.5, a daily decline of 1%.

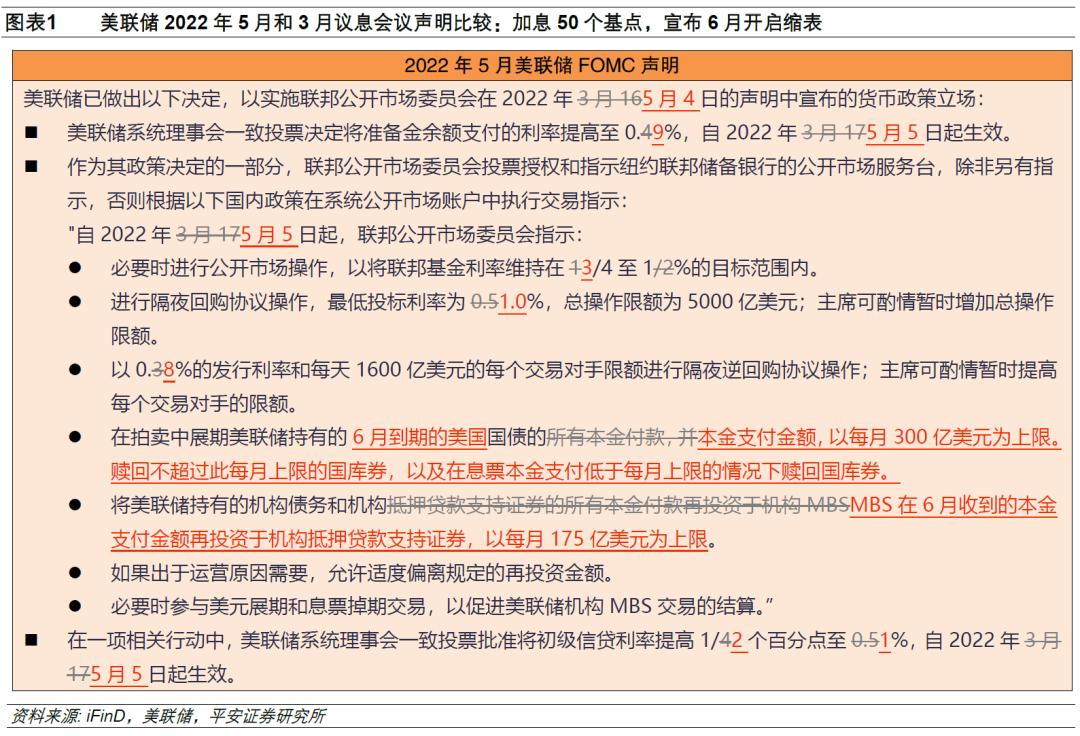

Monetary Policy: The Federal Reserve's May statement announced an increase in the federal funds rate of 50bp to a target range of 0.75-1.00%, in line with expectations. At the same time, it announced that it will start to reduce its balance sheet on June 1, with a monthly reduction of $47.5 billion in assets and a monthly reduction of $95 billion in assets after three months (in line with the results of the March meeting minutes); it did not specify the end of the balance sheet reduction, but only said that it would slow down the pace of balance sheet reduction when it was about to reach the "sufficient level".

Statement statement: 1) More cautious judgment of the current state of the economy. The statement removed the broad description of "indicators of economic activity and employment continue to strengthen" and adjusted the description of job growth from strong to robust. 2) Believe that the impact of the Russian-Ukrainian conflict is more reflected in inflation than economic growth. 3) The risk of inflation caused by the disruption of international supply chains is newly mentioned.

Powell's speech: The market is paying more attention to the impact of the Fed's tightening and whether it will cause a recession. Powell's speech reassured the market: First, he said that he was not actively considering a 75 basis point hike, and mentioned that he might return to the usual rhythm of a 25 basis point hike after several 50 basis point hikes, dispelling concerns about a faster rate hike. Second, it said that the definition of "neutral interest rate" is flexible, or to some extent alleviates the market's panic about the "end point" of interest rate hikes. Third, it constantly emphasizes that the job market is strong, and the Fed has a greater chance of achieving a "soft landing".

At present, the Fed may be close to the most "eagle" moment in this tightening cycle in terms of expected guidance. First, the Signal to the market at the May Interest Rate Meeting was more "dovish" than the market expected. Second, U.S. inflation data is close to an inflection point, and economic growth and employment repair are showing signs of slowing. Finally, the market's calculation of the Fed's tightening expectations has been relatively sufficient, the US financial conditions have been tightened in advance, and the need for the Fed to further "let go of the eagle" is not strong. The current 30-year fixed rate on mortgages in the United States has risen above 5.1%, the highest level since 2010; the dollar index has risen above 103 points; and the US stock S&P 500 index has pulled back nearly 10% during the year.

As the Fed is about to pass through its most "eagle" period, the corresponding impact on the allocation of large assets is worth paying attention to. After the May 5 meeting, the CME interest rate futures market's expectations for a Fed rate hike in 2022 fell sharply by 100bp to 2.00-2.25%. 10-year Treasury yield highs or mid-year. Real interest rates on U.S. Treasuries may continue to rise as the Fed shrinks its balance sheet, but inflation expectations may fall back. If the 10-year Treasury yield peaks, the dollar index may also peak quickly (usually within 3 months). The earning power of U.S. stocks may decline significantly, but the magnitude of the adjustment is difficult to determine, depending on whether the U.S. economy will fall into recession, and then whether the Fed will raise interest rates more than the "neutral level" of 2.5% during the year.

1. Monetary policy: raise interest rates by 50bp, and start to shrink the balance sheet in June

The Federal Reserve announced a 50bp increase in the federal funds rate to a target range of 0.75-1.00% in the May 2022 interest rate meeting, in line with expectations. Similar to the March meeting, the Fed raised several other policy rates at the same time to coincide with the new federal funds rate range: 1) raised the reserve requirement rate from 0.4% to 0.9%, 2) raised the overnight repo rate from 0.5% to 1.0%, 3) raised the overnight reverse repo rate from 0.3% to 0.8%, and 4) raised the Tier 1 credit rate from 0.5% to 1.0%.

At the same time, the Fed announced that it will begin to reduce its balance sheet on June 1, with a monthly reduction of $47.5 billion in assets and a monthly reduction of $95 billion in assets three months (in line with the results of the discussions in the March meeting minutes); it did not specify the end of the balance sheet reduction, saying only that it would slow down the pace of balance sheet reduction when it was about to reach the "adequacy level".

Specifically, the Fed separately published the Fed Balance Sheet Reduction Plan document, which gives a more detailed path to the reduction of the balance sheet: 1) Starting June 1, 2022, the Fed will only reinvest in securities held in the System Open Market Account (SOMA) that exceed the monthly ceiling. 2) For treasuries, the initial cap will be set at $30 billion per month, which will increase to $60 billion per month after three months. Under this monthly ceiling, the decline in Treasury bond holdings will include Treasury notes and Treasury bonds, of which the amount of notes due will need to be lower than the monthly cap. 3) For institutional debt and institutional mortgage-backed securities (MBS), the initial cap will be set at $17.5 billion per month, which will increase to $35 billion per month after three months. 4) In order to ensure a smooth transition, the Committee intends to slow and halt the decline in the size of the balance sheet when the reserve balance is slightly higher than it judges to be consistent with the adequate reserve. Once the balance sheet stops flowing, the reserve balance may continue to decline for some time, reflecting the growth of other Fed liabilities until the committee judges that the reserve balance is at an adequate level. Thereafter, the Commission will manage securities holdings as needed to maintain sufficient reserves for a period of time. The Commission is prepared to adjust any details of its approach to reducing the size of its balance sheet in the light of economic and financial developments.

2. Statement statement: Emphasize the additional inflation risks brought about by geopolitical and supply chain factors

In its May statement, the Fed remained highly vigilant about inflation risks, but weakened the disruption to economic activity. The main changes in this statement compared to the March statement include: 1) a more cautious judgment of the current state of the economy. The statement removed the general description of "economic activity and employment indicators continue to strengthen" and referred to the fact that the margin of economic activity declined in the first quarter, and the description of job growth was adjusted from strong to robust. 2) Believe that the impact of the Russian-Ukrainian conflict is more reflected in inflation than economic growth. Compared to the previous one, the statement confirmed that the Russian-Ukrainian conflict was "on" (not "probably") putting additional upward pressure on inflation, but argued that it was "likely" (rather than "being") to put pressure on economic activity. 3) The risk of inflation caused by the disruption of international supply chains is newly mentioned.

After the announcement of the meeting, the market performance was relatively flat. In 10 years, the US Treasury yield remained in a narrow range near 2.98%, the US stock S&P 500 index once turned from 0.7% to fall, and the US dollar index fell slightly but did not fall below the 103 mark.

3. Powell's speech: Eliminate the concerns of "faster interest rate hikes" and consolidate market confidence

Overall, most of the issues at this press conference still revolve around inflation, but the market has paid more attention to the impact of Fed tightening and whether it will cause a recession. But Powell's remarks reassured the market to some extent: First, he said that he was not actively considering a 75 basis point hike, and mentioned that he might return to the usual rhythm of a 25 basis point hike after several 50 basis point hikes, dispelling concerns about a faster rate hike. Second, it said that the definition of "neutral interest rate" is flexible, or to some extent alleviates the market's panic about the "end point" of interest rate hikes. Third, it constantly emphasizes that the job market is strong, and the Fed has a greater chance of achieving a "soft landing", which continues to consolidate the market's confidence in the economy.

After Powell's speech, the market felt "doves": in 10 years, the US Treasury yield fell sharply by 10bp to 2.90%, and finally closed at 2.94%; the three major US stock indexes collectively turned from falling to rising and continued to rise, the Nasdaq Index, the S&P 500 index and the Dow Jones Industrial Index closed up 3.19%, 2.99% and 2.81% respectively; the US dollar index plunged from a high of 103.4 to near 102.5, a daily decline of 1%; gold prices rose from falling to rising, up about 0.9% during the day.

Specifically:

1) About the pace of hikes. The second question at the press conference was whether the Fed would consider raising interest rates by more than 50 bp (e.g. 75 bp) in a single way. Powell said a 75bp rate hike is not an option that the Fed is actively considering; the option of a 50bp rate hike will still be discussed at next meetings; the pace of rate hikes will depend on future economic data and financial conditions; if inflation starts to see easing, or other progress, it may return to a 25bp hike; but one month's inflation data is not enough (the core inflation rate has eased in the past two months), so it is not expected to return to a rate hike of 25bp anytime soon.

2) About the end of the hike. There will be multiple questions for the fed about the end of this round of interest rate hikes. First, Powell made it clear that the current goal is to reach a "neutral rate," but this is a concept, not a particular level, which will depend on financial conditions and the impact of higher interest rates on the economy. Second, on whether a "restrictive level" needs to be reached, Powell said it is too early to discuss the decision, and will be decided after the interest rate reaches a neutral level. But it has also stressed more than once the Fed's determination to curb inflation, saying it would do so if the committee deemed it "appropriate," that price stability is a prerequisite for u.S. economic stability, and that the Fed has the courage to do the right thing.

3) About the rhythm and impact of shrinking the table. Powell said that the opening point of the balance sheet reduction (June 1) is only a date and there is not much other consideration; the impact of the balance sheet reduction is uncertain. However, in the opening statement of the press conference, he stressed that the balance sheet reduction is an important part of the current Fed's tightening stance, and the balance sheet reduction decision will also be guided by the "double goal" (price stability and maximum employment), and the Fed's policy will remain flexible.

4) About inflation. Reporters noted that the statement of the meeting further emphasized the impact of the "supply factor" on inflation. As monetary policy is difficult to directly solve the supply problem, the market has shown more concerns about whether the Fed can effectively curb inflation. There is a clever question: whether the Fed needs to solve the supply problem first to achieve its 2% inflation target. The implication is whether the continuation of the supply problem means that the Fed will struggle to achieve its target inflation levels. Powell said that first, the Fed is currently mainly targeting the problem of excess demand. Second, the Fed will focus primarily on core PCE indicators, as they primarily reflect inflation caused by non-supply factors. Finally, the Fed will work on anchoring inflation expectations (around the 2% target).

5) About the recession. Reporters will have more than one question expressing concern about whether the U.S. economy will fall into recession. For example, the first question mentions whether the Fed's confidence that the US economy will not decline has changed. Powell responded mainly with a strong job market, saying that the current job market is particularly strong, and future job growth is expected to slow down, and then the job market is more balanced between supply and demand, which is conducive to inflation easing. Since then, it has also expressed its views directly after another question, still believing that there is a greater opportunity for US inflation to be moderated, but not accompanied by a recession.

6) Regarding the credibility of the Fed. A reporter sharply asked whether the Fed has lost credibility. This is a difficult question to answer because its answers can be too subjective and unconvincing. But Powell responded well with objective facts, saying that the Fed still has good standing and that financial markets have reacted in advance to future interest rate hikes, which reflects the market's trust in the Fed's interest rate hike path.

4. Has the Fed's most "eagle" period passed?

In our view, the current Fed may be close to the most "eagle" moment in this tightening cycle in terms of expected guidance.

First, the Signal to the market at the May Interest Rate Meeting was more "dovish" than the market expected. In the may meeting statement, the Fed was a little more cautious about employment and economic growth, and placed more emphasis on supply factors in terms of the causes of inflation. If "excess demand" plays a limited role in the current U.S. economy and inflation problems, the need for aggressive fed tightening will be difficult to further enhance. As in this Powell speech, the possibility of another acceleration of the pace of interest rate hikes (a single rate hike of 75bp) and greater flexibility for the end of this round of rate hikes may be a signal that "hawks" are expected to lead closer to the inflection point.

Second, U.S. inflation data is close to an inflection point, and economic growth and employment repair are showing signs of slowing. In terms of inflation indicators, the US core PCE price index, the Fed's most concerned inflation indicator, recorded 5.2% year-on-year in March, down from 5.3% in February. The core CPI and PCE have fallen back to their lowest levels since September 2021. We estimate that if the U.S. April CPI does not exceed 0.7% month-on-month, the April CPI year-on-year reading will not exceed 8.5% of March. In terms of inflation expectations, the 5-year and 10-year TIPS implied inflation expectations reached highs on March 25 (3.59%) and April 21 (3.02%) respectively, while the University of Michigan's inflation expectations for the next year recorded 5.4% in April and flat in March. In terms of economic growth and employment, the downward pressure on the US economy has been highly concerned by the Federal Reserve and the market, as mentioned at the opening of the statement of this meeting, the real GDP of the United States in the first quarter of this year "edged down". According to our analysis, although the economic data of the first quarter of the United States is disturbed by "technical factors" such as the decline in private inventories and the easing of supply chains, the weak consumption of goods and the decline in fiscal expenditure are also hidden dangers of the economic downturn (for details, please refer to the report "Temporary Recession" or Insufficient Fear in the United States)." The latest US ISM manufacturing PMI employment index recorded only 50.9, the lowest since September 2021.

Finally, the market's calculation of the Fed's tightening expectations has been relatively sufficient, the US financial conditions have been tightened in advance, and the need for the Fed to further "let go of the eagle" is not strong. For example, the current 2-year and 10-year Treasury yields have largely reached 2018-2019, when the federal funds rate was already at a neutral level of 2.5%. The current 30-year mortgage fixed rate in the United States has risen below 5.1%, the highest level since 2010. The rapid rise in interest rates in financial markets is cooling demand for home purchases and durable goods consumption. At present, the dollar index has risen below 103 points, and the negative impact of the "strong dollar" on US exports may continue to appear, just as net exports have caused a significant drag on the US economy in the first quarter. At present, the US stock S&P 500 index has pulled back by nearly 10% during the year, and the deflationary effect brought about by the shrinkage of US residents' assets will also become an important driver for the cooling of personal consumption expenditure in the United States.

5. Has the most "panic" period in the market passed?

We believe that as the Fed is about to pass through its most "eagle" period, the corresponding impact on the allocation of large assets is worth paying attention to.

After the Fed's May meeting, expectations of rate hikes in the interest rate futures market have cooled sharply. As of May 4, the CME interest rate futures market is betting on the Fed's cumulative rate hike (weighted average) of about 300bp this year, corresponding to a policy rate level of 3.00-3.25%, significantly exceeding the "neutral level" of about 2.5%, and also exceeding the 2023-2024 interest rate finish line (2.75%) shown on the March Fed dot plot. After the May 5 meeting, the CME interest rate futures market's expectations for a Fed rate hike in 2022 fell sharply by 100bp to 2.00-2.25%.

10-year Treasury yield highs or mid-year. The current 2-year and 10-year Treasury yields are basically close to the peak of the previous round (the end of 2018), and the space for continued upside (even considering that the pace of this round of rate hikes is faster and the end of the rate hike may be farther) has been limited. In the report "Four Forces of US Treasury Yields Soaring", we calculated that the US Treasury yield may peak in the middle of this year, with a high point of about 3.1%, corresponding to a real interest rate high of about 0.4-0.5% (there is still about 40bp upside from the current level), and inflation expectations may fall to about 2.5% (there is still room for decline from the current level of about 30bp). We expect that as the Fed shrinks its balance sheet, the real interest rate on US Treasuries will continue to rise, but inflation expectations may fall in tandem, and then the upside of the 10-year nominal yield of US Treasuries will remain limited.

If the Fed's expected guidance becomes more "dovish," the 10-year Treasury yield could peak first, followed by a cap in the dollar index. First, historical data shows that the US Treasury market is the most sensitive to changes in Fed policy (expectations). If U.S. inflation eases or economic downside expectations strengthen, the U.S. Treasury market may be factored in the Fed's slowdown in the pace of tightening, followed by a cap and retreat in Treasury yields. Thereafter, the gap between the U.S. economic outlook and monetary policy tightening and its major trading partners could narrow further, followed by an inflection point in the dollar appreciation cycle. After the financial crisis, in the four cycles in which US Treasury yields rose in tandem with the US dollar index, once the US Treasury yield peaked in 10 years, the US dollar index may also peak quickly (usually within 3 months).

After the U.S. Treasury yield is turned around, the earning capacity of U.S. stocks may decline significantly, but the adjustment is still difficult to determine. With the weakening trend of the US economy and the high level of interest rates in financial markets, the earning power of US stocks may decline significantly. Historical data also show that after the 10-year US Treasury yield peaked, the earning power of US stocks tended to decline sharply, and may even encounter a deep correction (negative year-on-year earnings growth). However, whether the current round of US stocks will experience a deep correction will ultimately depend on whether the US economy will fall into a serious recession. In our view, if the Fed raises interest rates no more than a "neutral level" of 2.5% during the year, the risk of a U.S. recession and a deep correction in U.S. stocks this year may be relatively limited.

Risk warning: International geopolitical conflicts have uncertainties, US inflation pressure exceeds expectations, downward pressure on the US economy exceeds expectations, and The Fed's policy tightening is more than expected.

This article originated from the Financial Associated Press

![Xiaolan tips: "May Day" holiday, a safe holiday[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)