In the US stock market, there is such a company, the gross profit margin is almost 100%, the net profit margin is 60%, the profit margin stands out in the US stock market, there is no competition, and it is doing a business that is more monopolistic than the monopoly - landlords.

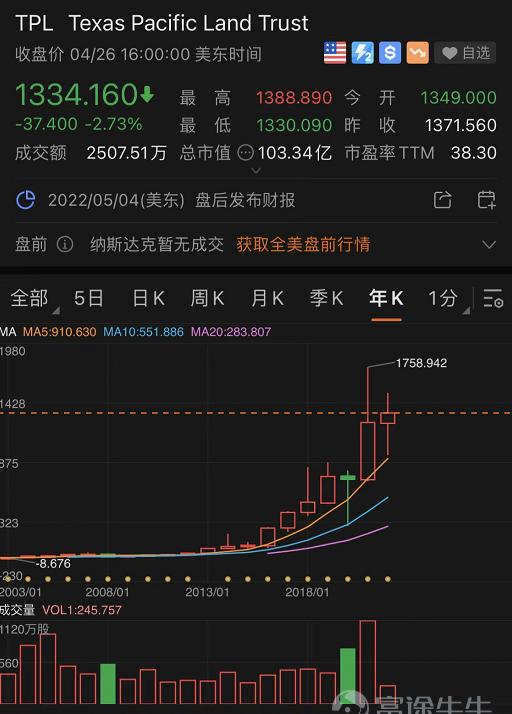

In the past 10 years, the company has relied on this capitalless business to achieve a 38-fold increase in stock prices in 10 years, which is better than most growth stocks.

This strange company is Texas Pacific Land, which has 880,000 acres (about 3,500 square kilometers) of land in Texas, and since the additional oil reserves in the area were discovered in 2010, the company's land has become an appreciating resource, and the company itself does not produce oil, but only provides services for oil development companies on its own land, engaged in low-risk businesses such as selling water and collecting rents, although closely related to the oil cycle. But the company is rising almost every year.

Today, oil prices have entered the high area and are still rising, as an oilfield landlord, the value of TPL still seems to have a huge room for release?

First, from wasteland to oil fields

Land in the United States has always been private property, many individuals or institutions own a large amount of land in the United States, of course, there is land in the United States is not a great thing, because the United States is sparsely populated, has no development value, no geographical advantages and no resources of land is just meaningless assets, because there is no commercial value, but the development has to pay land taxes.

Landlords are not a positive word in the United States, and so is TPL, although sitting on a city-sized land ownership, founded in 1871, but for more than a hundred years, the company has only a market value of hundreds of millions, except for a small amount of land with a little resource, most of the rest of the assets seem to have little value.

The company's land used to have a small amount of oil reserves, but it didn't make much sense, but in 2010, more oil was found on the company's land by unconventional means, and it could be extracted at a lower cost. The substantial increase in reserves has turned the company's land into a large oil field, and since then, the company has begun the road of value-added.

Discovering that there was a huge amount of oil in its own field, it was logical to develop it itself, and then transformed into an oil tycoon, but the company chose a more conservative approach, not to participate in the development, but to sell the development rights, to provide services for the oil company itself, and to make some risk-free money.

Therefore, after the discovery of a large amount of oil, the company's value release is not explosive, with the investment promotion, so that oil developers began to slowly lay drilling on the ground, the company slowly began to increase rent and equity expenses, the company's income also appeared a relatively even sustained growth.

In 2017, the company added water services to the original rent and commission, building a water treatment plant near the oil production equipment to provide the pure water and raw water required for the oil company's process of processing crude oil.

The company is completely what people often say about the business of selling water to the extreme, do not undertake the work of crude oil extraction, is to do services for oil production companies, of course, the reason why the company can do this kind of business of selling water, the reason is also TPL, although the oil company also has its own water plant ability, but can not stand the landlord want to do it themselves.

Relying on the development of the water treatment business, the company's revenue has also continued to maintain higher growth, and it is the company's business model to earn as much service fees as possible in the drilling cycle process.

About 63% of the company's current revenue structure is an equity share (the oil price is higher in 2021, so it accounts for a large proportion), which is a 4.4% from the revenue from the oil dug. And 9% is rent and 28% is water. This revenue structure allows the company to fully benefit from oil extraction while minimizing risk.

The company also implemented the idea of anti-risk into the asset-liability structure, the current company's balance sheet is extremely clean, there is no interest-bearing liability, that is, the financial risk is 0, as a landlord, land is the most valuable asset, but because the company was founded more than a hundred years ago, so in the financial terms have long been these fixed assets depreciation, so the company's balance sheet fixed assets have been empty, which is why the company has no cost reasons, It was also after the boiling water plant in 2017 that some machinery and equipment were added to increase fixed assets.

Therefore, the company can be said to be an asset-light company with a huge amount of invisible assets, and the existence of these hidden assets is the company's safety cushion, but at the same time it causes distortion in the price-to-book ratio.

All of the company's expansionary growth is based on its own profits, not borrowing, while free cash flow is all used for buybacks and dividends. Therefore, from a long-term perspective, TPL does not have the various common risks of cyclical industries.

Second, a different cycle model

Most cyclical companies have income elasticity, that is, performance explosive power, when commodity prices rise, the cost of these companies is relatively fixed, so a slight change in revenue can bring about sharp fluctuations in profits, such as oil developers in low oil prices, performance may lose money or even small profits, and oil prices double, often the performance can be several times or even dozens of times. Therefore, for these companies, it is often not open for ten years, and the opening of ten years may be a particularly high product price for 1-2 years, which is enough, so that the company can generate profits in the past 10 years.

Unlike them, while revenue sharing is the company's largest source of revenue, TPL's performance is positively correlated with high oil prices, but large profit fluctuations do not exist, because there is a gross margin of nearly 100% in itself, and revenue fluctuations are unlikely to produce particularly large profit fluctuations.

For TPL, what matters is not how high the price of oil can be, because even if the price of oil suddenly soars, its profit change is not large, and it will not be like the oil stock suddenly dropped from 30 times PE to 2 times, and suddenly made a few more years of profit in a quarter.

The key to the company's valuation is the sustainability of oil prices, because the continuous high oil prices will lead to the company's development cost of higher oil fields can begin to be drilled, and the capacity of existing low-cost oil fields will also increase, which leads to more use of its land, whether it is water, rent, or share, will increase with the increase in production capacity, and the long-term life cycle profit can be higher.

The disadvantage to the company is the continuous downturn in oil prices, the average development cost of the company's oil field is about 40 US dollars a barrel, when the oil price is below this range and lasts for a period of time, the longer it lasts, the oil development company on the land may choose to stop part of the production capacity, and for the company, this will be a problem, because if the production capacity declines, even the rent and water charges collected by drought and flood protection have the risk of falling.

In 2020, there have been stress tests when the company faces the downturn of the oil cycle, remember that there was a negative oil price of some futures at that time, and the average WTI value of Q2 in 2020 is about 20 US dollars, and the company achieved revenue of 0.96, 0.5, 0.74, 0.74 billion in the four quarters of 2020, and the net profit was 0.57, 0.27, 0.56, 0.55 billion, it can be said that 0.27 billion a quarter, which is the company's profit bottom in a very low oil price state.

Of course, the low oil price below $40 did not last long, so the company did not have a real logical test, and soon the oil price returned to more than $40, and as of today, the oil price has exceeded 100, so the company's current stock price has increased by nearly 5 times compared with the low in 2020.

At this point, we can also understand why the company has continued to rise over the past 10 years, the company is slow to release the value of its land, as long as the oil price is maintained above $40, the company will begin its own organic growth, as oil developers continue to increase production capacity, the company's risk-free income has also risen, and this rate is not slow, and from 2012 to now, oil prices have been above $40 for the most part.

The company's revenue increased by 13.6 times from 2012 to 2021, and the annualized income was about 30%, which is one of the largest revenue growth rates in the world capital market, which also explains the company's ultra-high stock price increase, of course, high income and high oil prices will definitely be related, which makes the revenue share higher, resulting in a certain cyclical high profit, but that is not the focus of the company's valuation.

The company made a profit of 270 million in 2021, while the average crude oil in 2021 is $73, so assuming that the future oil price remains around $70, then the company clearly has the opportunity to continue to maintain a higher annualized growth rate on the basis of 270 million.

The company's current development cost of less than $40 reserves is expected to be available for exploitation for about 19 years, but there are more undeveloped reserves above $40 and below $60, and it is now profitable to develop these reserves at oil prices, so looking ahead, for decades, as long as the price of crude oil does not continue to fall below $40, the company's oil will not be recovered, and the entire business model will remain sustainable.

In addition, the company's management is aggressive, only 102 employees, the cost control is appropriate, after collecting rent and water charges, the company is still thinking about how to increase revenue, such as the introduction of similar to "selling water" charging services in terms of energy conservation and carbon reduction, and, high and sustained oil prices, the company's commission and rent charges are not without room for price increases for a long time.

III. Conclusion

So, TPL is a very weird company, is it a growth stock or a cyclical stock? When oil prices fluctuate, the company's revenue will also fluctuate, and the stock price is also, in 2020 Q2, oil prices plummeted, the company's profits halved, the stock price retraced by 60%, it is certainly a cyclical company related to the oil industry, but, 10 years 38 times, basically every year is rising, this is not a growth stock?

The key is to understand the company's business model and long-term release value, if investors see that between 2010 and 2020, the average price of oil will not be less than $40, and the company's model is based on this can maintain long-term high growth, then obviously, we do not need to care about the fluctuation of oil prices, which can be held for a long time. Assuming that in the next 10 years, if the international oil price continues in the range of more than 50 US dollars, according to the current model, the company will certainly have a good room for growth, of course, it is now an area with ultra-high oil prices, and it is also the best time for resource stocks to rise, so the company's valuation of 11 billion is undoubtedly a high premium at present.

But the key is how we understand it, staring at the fluctuations of oil prices every day, paying too much attention to its cyclicality, it is difficult to understand the logic of the company's long-term value growth.