In the early days of the covid-19 outbreak, the repayment ability of some cardholders declined, and the asset quality of bank credit card business attracted market attention.

Brokerage China reporters combed the information of listed banks that have currently released their annual reports and found that by the end of 2021, the credit card failures of state-owned banks and joint-stock banks have generally declined. Many bank executives said at the performance conference that the asset quality of the current credit card business has been stabilized and improving.

However, from an absolute point of view, the balance of non-performing loans on credit cards in many banks has gone up, coupled with the spread of the epidemic in Omicron, the people's livelihood in many places has been affected to a certain extent. Industrial Bank and China Merchants Bank raised the criteria for identifying overdue loans in credit card business last year. It can be seen that banks still need to remain vigilant about the pressure on retail loans, including credit cards.

In the past year, the credit card business has not only faced professional challenges in risk management and control, but also had to cope with competition in the stock market. Judging from the current financial report, the business income between banks has also diverged, and some banks' credit card business has become a drag on the growth rate of fee income, and some banks still maintain a year-on-year increase of more than 20% in this category.

In order to promote the growth of credit card business, banks on the one hand through accelerating the integration of technology and business, improve customer reach and service efficiency, on the other hand, to "intensive cultivation" of customer groups and subdivision business areas, at the same time, various thematic credit cards and marketing methods are also emerging.

The bad situation has improved

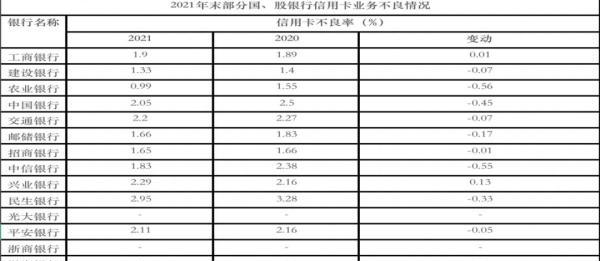

Brokerage China reporters sorted out the annual reports of 11 countries and stock banks that have disclosed relevant data and found that the non-performing rate of credit cards in 2020 generally fell last year, in addition to the Industrial and Commercial Bank of China and Industrial Bank, there are 9 national and stock banks Credit card non-performing rates that have achieved a downward trend ranging from 1 basis point (BP) to 56 basis points.

Among the 11 state and stock banks that have disclosed comparable data, IB's credit card non-performing rate rose most significantly at the end of last year, increasing by 13 basis points to 2.29% from the end of 2020, and the non-performing rate was second only to Minsheng Bank (2.95%); at the same time, the bank's credit card non-performing loan balance also increased by 1.131 billion yuan to 9.985 billion yuan compared with the end of 2020.

In this regard, Zou Jimin, general manager of the risk management department of Industrial Bank, explained at the performance conference that the bank's credit card non-performing "double rise" is active, "one is to support the prevention and control of the new crown epidemic, protect the rights and interests of consumers, appropriately slow down the disposal of customers affected by the epidemic, and encourage customers to take the initiative to repay after the epidemic eases; second, considering that the credit card overdue identification standards in 2021 tend to be strict, it is necessary to give customers a certain adaptation period."

According to the annual report, in the fourth quarter of 2021, Industrial Bank strictly enforced the criteria for the identification of overdue credit card loans in accordance with regulatory requirements, and advanced the time point of overdue recognition compared with the original rules, resulting in an increase in concerned loans and overdue loans.

Zou Jimin further said that last year, the generation rate of non-performing loans on credit cards of Industrial Bank and the amount of new non-performing loans fell year-on-year. Among them, in 2021, the bank's credit card non-performing loan generation rate was 4.17%, down 1.82 percentage points year-on-year; the new non-performing amount was 17.6 billion yuan, a year-on-year decrease of 5.1 billion yuan, a decrease of 22.43%. "Therefore, the overall risk of our bank's credit card is controllable, and the trend of asset quality has not changed." He said.

It is worth noting that although the non-performing rate of credit cards of state and stock banks generally improved at the end of last year, the balance of non-performing loans of many banks still showed an increasing trend. For example, the balance of non-performing loans on credit cards of China Merchants Bank increased by 1.422 billion yuan from the end of the previous year, an increase of 11.45%.

Zhu Jiangtao, vice president of China Merchants Bank, said that the bank advanced the identification standard of credit card defects from 90 days overdue to 60 days overdue last year; at the same time, according to regulatory requirements, the identification of credit card overdue points was set from the next bill date to the repayment deadline of this bill, with an average of about 8 days in advance. "If these two factors are restored, the amount and rate of credit card attention and overdue are lower than at the beginning of the year, and the substantive risk shows a downward trend." He said.

Looking forward to 2022, Zou Jimin said that many factors such as economic downward pressure and local epidemic impact still exist, but there is still a lot of room for consumption growth after the epidemic eases, and the quality control of credit card assets is facing new opportunities and challenges at the same time.

Zhu Jiangtao also mentioned that from the perspective of early asset quality indicators of credit cards, such as the intake rate, the M1-M3 grace daily recovery rate and the M1-M3 slope rolling rate, these early risk indicators have returned to the pre-epidemic level, and the overall judgment of credit card risk is currently in a continuous stable and good trend.

Revenue from the credit card business is differentiated

From the perspective of card issuance, ICBC, China Construction Bank and Bank of China are still in the top three, with a cumulative number of cards issued at the end of last year of 163 million, 147 million and 135 million, respectively; but from the perspective of new card issuance, the growth rate of Postal Savings Bank card issuance can be described as "riding the dust" among a number of state-owned banks, the bank issued 8.0222 million new credit cards in 2021, and the number of year-end balance cards was 41.5587 million, an increase of 12.93% over the end of 2020; and the industrial and industrial workers who have already entered the ranks of "100 million-level card issuers" have already entered the ranks of "100 million-level card issuers". The growth rate of card issuance of the three state-owned banks in Jianshe and China last year remained at a low level of less than 3%.

Postal Savings Bank said in its annual report that last year the bank carried out the reform of the system and mechanism of the credit card center franchise and was officially registered in Beijing in May 2021. Last year, the postal savings bank card business fee income was 11.951 billion yuan, an increase of 3.78% year-on-year, of which the bank's credit card business revenue increased by 21.22% year-on-year.

In 2021, the bank's bank card fee increased by 1.760 billion yuan over the previous year, an increase of 11.96%, and the bank also mentioned in the annual report that this was mainly due to the increase in credit card fees.

But at the performance conference, Wang Kang, vice president of China CITIC Bank, also said that in fact, due to the impact of mortgage loan policies, retail loans have slowed down last year, "the increase in credit card loans is not very much, so the increase in public loans is slightly more than that of retail loans."

It is worth noting that under the adjustment of credit card business, the growth of credit card fee income of some banks has slowed down. The Bank of Communications is on par with the situation in 2020.

Guo Mang, vice president of the Bank of Communications, also said at the performance conference that in 2022, the bank will also focus on improving customer experience, enhancing the activity of credit cards, and improving the ability of omni-channel customer acquisition, "such as launching some credit card products with a strong sense of the times and great influence." He said that through data-driven + online operation, continue to increase brand marketing activities, and from the first two months of this year, the bank's credit card consumption and card loan balance growth rate is faster than the same period last year, the relevant work has begun to bear fruit.

China Merchants Bank's bank card fee income has also declined, and the bank's annual report said that this is mainly due to the reduction in the volume of credit card offline transactions. In 2021, CMB's bank card fee income was 19.377 billion yuan, down 0.89% year-on-year.

Accelerate digital transformation

The pandemic has catalyzed the digital transformation of banking, and credit cards are no exception. A number of bank executives said that they need to accelerate digital capabilities to empower business lines, broaden the reach of credit card customers, and improve customer acquisition, service and operational efficiency.

"Technology has become an important support for the transformation and development of banking." Qi Ye, vice president of Everbright Bank, said at the performance conference that in 2022, the bank should enhance the service support of science and technology for credit card business and branches, focusing on promoting the upgrading of three system platforms: first, intelligent risk control platform, real-time approval will be accelerated, and risk customer early warning disposal will be more accurate; second, intelligent sales platform, which integrates tools such as fine operation of traffic pools, accurate profiling of big data, and digital customer acquisition models to create customer acquisition growth points; third, intelligent customer operation platform, with digital transaction operation + customer operation as the core To achieve intelligent iteration of customer insight, strategy execution, strategy monitoring and evaluation, and improve operational efficiency.

"In terms of internal management, Everbright Bank should build 'operation + technology' composite talents, adjust the team structure, etc., and jointly support the transformation and development of the credit card business." She said.

Ping An Bank is also strengthening the digital operation capabilities of credit cards and other products in 2021, and gradually applying the "five-in-one" business model explored by the bank to the credit card business sector. According to the annual report, the total credit card transaction amount of Ping An Bank in 2021 will be 3.8 trillion yuan, ranking the forefront of joint-stock banks. The retail "five-in-one" model is the culmination of Ping An Bank's scientific and technological capabilities in the past five years, the core is to train an AI account manager team through deep learning of various knowledge bases, and organically combine with remote banks and offline outlets to form an ATO service model (AI bank, remote bank, offline bank) to drive operations with digitalization.

In recent years, with the attention of financial institutions to consumption scenarios, the expansion of financial consumption scenarios is also known as a part of the acceleration of the digital transformation of credit cards. Compared with the traditional commission fee income, loans based on the expansion of financial consumption scenarios have become the main force in the growth of credit card business of some banks.

In terms of the integration of scene customer acquisition and payment, several large banks, including the Bank of China and the Agricultural Bank of China, mentioned in their annual reports that credit card business is integrated into the main battlefield of the consumer finance "scene", including large consumption scenarios such as automobiles and home improvement.

Qi Ye also mentioned at the performance conference that the bank, under the premise of strictly adhering to the risk bottom line, accelerated the innovative development of consumer staging, promoted the staging of automobiles, home appliances, decoration and other scenarios, and built a commodity staging platform relying on WeChat Mini Programs to tap the potential value of consumer customers. According to reports, last year, after the bank improved the card environment of the online Internet platform and offline consumption scenarios, the proportion of high-quality customers newly introduced was 65%, a significant increase from the beginning of the year; online transaction volume increased by more than 40% year-on-year.

Thematic innovation cards are emerging in an endless stream

As credit cards enter the stock competition market, banks are more meticulous in their operations for different customer groups and different segments of business, and marketing methods are also frequent. Among them, combined with different current affairs backgrounds, the launch of the theme credit card, co-branded credit card has become the standard of almost every bank.

For example, in 2021, green and low carbon has also received attention from many parties, and new theme credit cards related to it have also been developed, and the Bank of China will issue green and low-carbon theme digital credit cards. In addition, the bank also took the opportunity of the Beijing Winter Olympic Games, which is of concern to the whole people, to give full play to the advantages of the bank's Winter Olympic partners, issue and promote the Beijing 2022 Winter Olympics theme debit cards and credit cards, provide overseas bank card acceptance services to cross-border customers, and provide winter Olympic acceptance environment construction services for Beijing and Zhangjiakou in Hebei Province.

When the Chinese reporter of the securities company visited the bank of China's offline credit card promotion booth, he found that the card face of the bank's Winter Olympics theme credit card was printed with the popular "net red grade" IP ice pier, and if the user applied for the card, he had the opportunity to get the ice pier gift, so the bank's credit card booth seen by the reporter was quite lively.

Since last year, CCB has also accelerated the construction of a digital virtual credit card product system, innovated and launched new products such as Gemme Card, Transformers Leader Credit Card, and Yuntong Yaohong Card, explored the cooperation and drainage model of Internet head enterprises, and promoted the extension of credit card customers to young inclusive customers.

In fact, young customers are a group that many banks want to reach. Qi Ye, vice president of Everbright Bank, said at the performance conference that the bank's credit card development in 2022 should pay attention to the two key points of young customers and practical customers to enhance customer value contribution.

"On the one hand, we will focus on the introduction of young consumer-oriented high-quality customers, improve the construction of young customers' products, scenes, brands, and reach, and increase the proportion of young customers." On the other hand, it focuses on the improvement of the scale of customers, launches the "About Hui Friday" normalized theme marketing activities, builds a merchant system, covers e-commerce, catering, car life and other card use scenarios, and comprehensively applies customer business means such as activities, rights and interests, and points to carry out precision marketing and enhance the stickiness of customer cards. She said.

Column Editor-in-Chief: Gu Wanquan Text Editor: Dong Siyun Title Image Source: IC photo Image Editor: Shao Jing

Source: Author: Brokerage China