Main types of taxes

* Gain tax (16.5%)

※ Property tax (15%)

※ Royalties (0.2%)

※ Salaries tax (progressive tax rate: 2%/7%/12%/17% and standard tax rate of 15%)

Note: Profits tax, salaries tax, and property tax have a provisional tax obligation in common.

Hong Kong does not levy: turnover tax (VAT, business tax, consumption tax), inheritance tax (suspended in February 2006), import and export tax (except special products such as tobacco and alcohol), capital value-added tax (such as dividends, dividends).

Gain tax

Profits tax is a tax levied on the basis of all profits derived from or from Hong Kong derived from the business when conducting business in Hong Kong. The profits tax rate for limited companies is 16.5%.

1. Profits tax adjustment

Hong Kong's two-tiered profits tax regime will be applicable to the year of assessment for the year of assessment on or after 1 April 2018. The tax rate on the first HK$2 million profit will be reduced to 8.25%, while the profit after the period will continue to be paid at 16.5%. The two-tiered profits tax system will benefit eligible enterprises with assessable profits, regardless of their size.

Remarks: Customers with multiple Affiliated Hong Kong companies can only choose one to use and enjoy a tax concession of 18/19 and a 75% reduction, with a maximum of 20,000 HKD per case.

※Hong Kong Profits Tax is only levied on profits derived from Hong Kong (16.5% of total profits).

※The Hong Kong Inland Revenue Department will issue a profits tax return about 18 months after the establishment of the new company, and the company will have three months to deal with it after receiving the tax form:

The tax filing of a Hong Kong company must be audited. The new Companies Ordinance clearly stipulates that Hong Kong companies should conduct annual account audits and then file taxes with the Inland Revenue Department. Select the year-end date (fiscal period). Hong Kong companies can choose any day as the end of the year. However, companies with the closing date of the two years can apply for an extension to 8.15/11.15/11.15 respectively after receiving the tax return, either 12.31 (consistent with the domestic accounting period) or 3.31 (Hong Kong fiscal year). Other companies on the end of the year, after receiving the tax return, cannot apply for an extension, and only have 1 month to file taxes.

The first year of the Accounting Audit of a Hong Kong company shall not be more than 18 months; the subsequent years shall be 12 months (a full financial year). If the first year is more than 18 months, a qualified opinion audit report will be issued, which will not affect tax filing, but may have an impact on corporate investment and financing.

※ Hong Kong companies with operating years of losses can be compensated indefinitely in subsequent years, domestic is five years. Losses in yearless operations cannot be brought back to future years.

※ Provisional tax: Profits tax is levied on the basis of assessable profits for each year of assessment, and assessable profits cannot be determined until the end of the relevant year. Therefore, the Inland Revenue Department will levy a provisional tax before the end of the relevant year. When the Inland Revenue Department subsequently assesses the assessable profits of the relevant year of assessment and makes an assessment, the provisional tax paid will be used to offset the assessed profits tax.

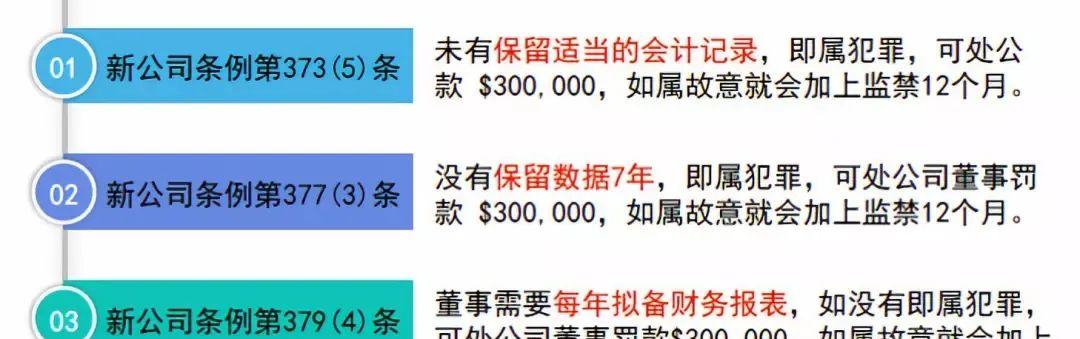

※Audit reports and accounting audit materials need to be retained for at least 7 years.

2. Legal responsibility for data preservation and accounting audit

3. Profits tax declaration method

No operational audits

During the year of assessment required by the Inland Revenue Department, the Company did not have any commercial transactions and did not have any bank access related to commercial transactions.

The audit report will disclose that the company has not operated during a certain tax period, only a small amount of necessary expenses (such as: company formation fee, annual audit fee, etc.), and the net profit is negative, no tax is required, but it is not allowed to delay losses.

Accounting audit and tax filing (with operation)

Submit corporate accounts, issue financial reports, fill in profits tax forms, and submit them to the Inland Revenue Department. Upon receipt of the Profits Tax Return issued by the Inland Revenue Department of Hong Kong, the tax return must be completed within the time limit and submitted to the Inland Revenue Department of Hong Kong together with the audit report reviewed and signed by the Hong Kong accountant.

Note: To avoid overdue tax forms, we generally notify you in advance.

Offshore exemption

Specifically, you can verify whether the business is taking place in Hong Kong from the following points:

(1) Neither the supplier nor the customer is a Hong Kong merchant;

(2) The signing process of the order does not take place in Hong Kong;

(3) Customs declaration, receipt and delivery, etc. have not occurred in Hong Kong;

(4) offices that do not have an entity in Hong Kong and employ Hong Kong employees;

(5) There are no business records left by the Hong Kong Government, etc.

Note: Companies need to pass the accounting audit before they can apply for an offshore exemption.

Salaries tax

Any person whose income derived from or derived from a position or employment in Hong Kong, less the allowable deductions (personal allowances or charitable contributions, etc.), is required to file salaries tax at the rate of tax. If the annual salary per person does not exceed the basic allowance and the eligible allowance (see details below), there is no salary tax (but still needs to be declared).

1. Year of assessment From April 1 to March 31, the centralized tax filing period is April.

2. The company shall submit the employee information to the tax bureau, and the tax bureau shall issue a tax form; if the employer does not submit it, the individual shall take the initiative to declare. Hong Kong companies have no withholding obligations.

3. The basic allowance for 2018/19 is HK$132,000 per year, and if the individual receiving the remuneration does not provide services in Hong Kong, he can apply for offshore and full tax exemption. However, directors are excluded, i.e. regardless of whether they are in Hong Kong or not, as long as they exceed the sum of 132,000 and other eligible allowances, they are taxed.

4. Ensure that the salary expenses in the financial statements match the declared salaries tax. (Many of them only remember that there are salaries when customers do accounting audits)

5. Standard tax rate: 15%

6. Progressive tax rate: the principle of lower than the ladder standard tax rate and the progressive tax rate.

Rin-ying tax

Real estate transactions and share transfers involve the measurement of the actual transaction price (transfer price) and the share capital, two thousandths (one thousandth of each buyer and seller).

Property tax

Hong Kong's tax on property income from owners of land and buildings is taxed at a rate of 15%. That is, only on-site operations need to be paid.

After the Hong Kong company applies, it needs to make an account and tax declaration to maintain the normal operation of the Hong Kong company. These details must not be ignored!

Audit the time of tax returns

(1) Newly established Hong Kong company: The first time to receive the profits tax return: From the 18th month after the date of incorporation, after receiving the tax return, the audit tax return must be completed within 3 months (the financial year end date can be freely selected).

(2) Tax filing time for non-newly established Hong Kong companies: Submit audit reports and tax forms on time according to the company's financial year-end date. (The grace period varies from year to year, please consult AC International Professional Consultant for details).

Note: Sometimes due to various reasons, Hong Kong companies do not receive profits tax forms from the Inland Revenue Department of Hong Kong during the tax filing period, which does not mean that Hong Kong companies do not have to file accounts and taxes. In this case, the Hong Kong company should consciously complete the tax filing work within the tax filing period.

Preparation before filing a declaration

(1) Although the Hong Kong government requires annual tax filing, enterprises generally cannot wait until the end of the year to start processing accounts, and should generally start preparing accounting information when there is a business occurrence;

(2) Classification and sorting of bills: The sales invoices, cost invoices and expense invoices are classified, sorted and placed in chronological order. If there are more bills, you can add a pencil number in the upper right corner of the ticket, and note that the dates of all documents provided match the dates of the accounting period;

(3) Recognized Bills: Compared with Chinese mainland, the Hong Kong government recognizes all invoices (which can be self-made), receipts and notes with the company's signature.

Information to be submitted

(1) Bank statements and water bills;

(2) Sales notes, invoices, contracts;

(3) Cost bills, invoices, contracts;

(4) Expense bills, wages, rent (lease contract or agreement must be provided), freight, etc.;

(5) Other relevant documents: an original copy of the Articles of Association, an annual return, all company changes (if any), fixed assets notes

Filing methods

1. No operation declaration

A. Applicable circumstances

During the assessment year required by the Inland Revenue Department to report, the Company did not have any business transactions, including any bank entry and exit, collection of any income or payment of any fees.

B. Procedures

Upon receipt of the Profits Tax Form issued by the Inland Revenue Department, it shall be completed and returned within the time limit. Generally after receiving the Profits Tax Return, it can be completed within a week after it is submitted.

2. Do accounting audit and tax declaration

Applicable to all Hong Kong registered limited companies.

Upon receipt of the Profits Tax Return issued by the Inland Revenue Department of Hong Kong, the tax return must be submitted to the Inland Revenue Department of Hong Kong together with the audit report audited by a Hong Kong accountant within the time limit. If there is a profit, you will receive a tax payment notice from the Inland Revenue Department within three months after submitting the audit report, with the tax and collection account number.

3. Offshore exemption

Neither the supplier nor the customer is a Hong Kong merchant; the order signing process does not take place in Hong Kong; the goods do not undergo customs declaration, receipt and shipment in Hong Kong; there is no physical office in Hong Kong and hong Kong employees are hired; and no business records are left by the Hong Kong government.

B. Application Procedure

Accounting audit → Submit the audited statements and reports to the TaxAtion Bureau for application→ Tax issuance of offshore issues letter → Write a reply letter and related materials to the Taxation Bureau → the tax bureau to issue the approval results.

Tax filing process

1. Audit the tax filing process

Signing the accounting and tax declaration agreement→ paying the money→ sorting out the documents, accounting processing→ and after the accounting is completed→ it is handed over to the auditor audit → the audit is completed→ the report is submitted to the shareholders for signature→ the accountant holds the signed audit report to the government to file the tax → the relevant documents to return to the customer.

2. Offshore tax exemption process

After receiving the tax return→ the accounting → the audit → to report the tax offshore→ answer the government's questions→ the government issue an offshore tax exemption notice.

Copyright note: The relevant content of this article is for reference only, please refer to the current tariff, the content of this article originates from the network, only for sharing reference, the copyright of the article belongs to the original author and the original source. The article reproduced on this public account, we pay tribute to the author of the article and have indicated the source of the author as much as possible, if for any reason it is omission or involves copyright and other issues, please contact the background to agree to delete.

![Zhu Yin: The goddess is 52 years old, and the Zixia Fairy was the peak of her appearance in the past, and she lived the happiest life" After Zhu Yin, there is no Zixia. "The Zixia Fairy played by Zhu Yin is like a bright star,[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)