Seat belts, an ordinary object that is extremely common in daily life, but have saved countless lives in traffic accidents.

The protective effect of seat belts on drivers and passengers is recognized by most people, and wearing seat belts on the road has become a social consensus.

However, if we compare the course of life to a car trip, do we also need to wear the "seat belt of life" to escort our long journey.

01

Multiple risks on life's path

The journey of life, like driving, also has many potential risks. Behind these risks, there are also various complications.

Therefore, we need to classify risks, prioritize them, and configure different defense systems.

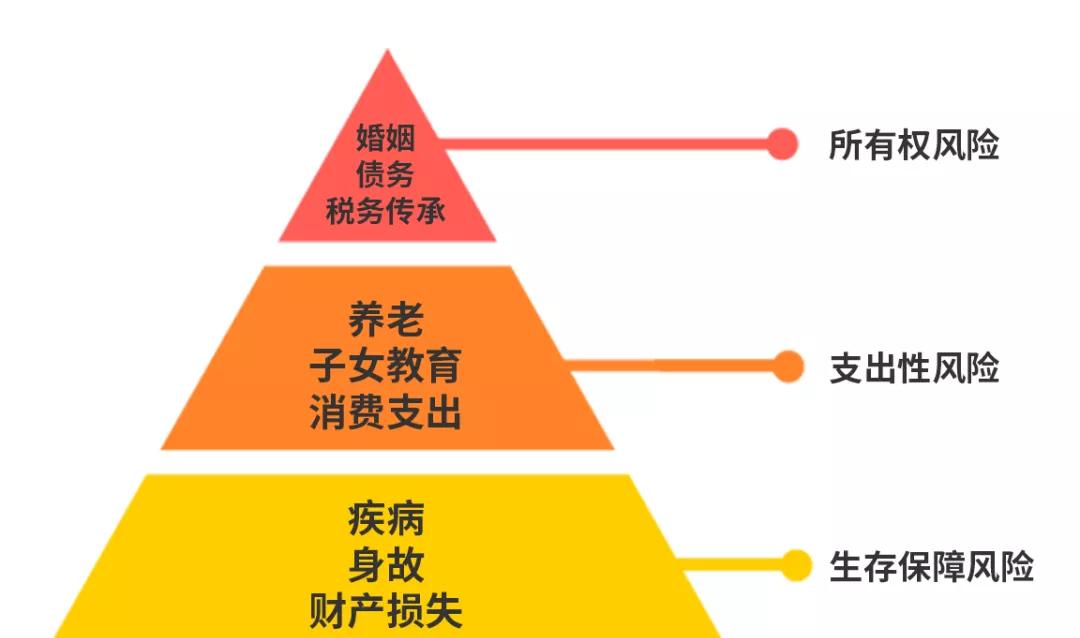

According to the risk pyramid chart, the risks that we may have in our lifetime can be divided into three types: ownership risk, expenditure risk, and survival guarantee risk.

1. Survival guarantee risk

As shown in the chart above, the risk of survival guarantee is the most basic risk, and once it occurs, it will have a huge impact on our quality of life.

Especially for the economic pillar of the family, if the family is unfortunate to suffer from serious illness or death, the whole family will lose its main source of income, and even fall into a debt crisis, which will seriously hinder the survival and development of the family.

2. Expenditure risk

Expenditure risk refers to the risk of large capital expenditure, such as the pursuit of a high-quality pension life, or the creation of superior educational conditions for children, which requires large amounts of financial support.

If there are not enough wealth reserves, you can only deal with large capital expenditures by "demolishing the eastern wall to make up for the western wall", resulting in a household financial deficit.

3. Ownership risk

Such risks refer to the risk of disputes that may arise from the ownership of property. Such risks are particularly prominent in wealth management and family wealth inheritance.

For example, once the marriage changes, even if the husband and wife sign a personal property ownership agreement before marriage, they are prone to mix with the common property of other couples after marriage, thus facing the risk of property being divided when the marriage changes.

02

Insurance is the seat belt of life

By recognizing the types of risks, we can manage risks in a targeted manner according to the type of risk. Using the analogy of driving is to wear a seat belt for our lives, but there is more than one seat belt.

1. The first seat belt: protect yourself

The insurance configuration should follow the principle of first protection and then financial management, and the following insurance can bear the responsibility of protection.

Medical insurance

Many people have such a misunderstanding: "With social security, there is no longer a need for commercial insurance." But in fact, families with serious illnesses in the family will understand that this is a wrong view.

Medical insurance is called social basic medical insurance, because the medical insurance policy benefits nearly 1.4 billion people in the country, so the focus is on "basic", in order to meet the basic medical needs of all people, but it can not meet the needs of all people, especially for the risk of major diseases, medical insurance alone is not enough.

At present, the drugs in the hospital are divided into three categories, of which 100% of class A drugs are reimbursed, class B drugs are partially reimbursed, and class C drugs are not reimbursed at all, and can only be paid at their own expense. Most imported drugs and self-funded drugs for serious diseases require self-payment.

Medical insurance and health insurance are complementary and non-conflicting, so that patients can receive better treatment and families will not be impoverished by illness.

When buying medical insurance, focus on whether the basic protection is comprehensive, value-added services, sum insured and deductible amount.

Critical illness insurance

The sum insured amount of critical illness insurance should include two parts:

(1) In addition to medical insurance, self-borne medical and convalescent expenses;

(2) Income compensation;

The second part is precisely the original intention of setting up critical illness insurance: "Doctors can heal patients physically, but if the patient is 'dead' financially, the doctor's previous work will be abandoned." ”

Critical illness insurance can not only solve the cost of treatment in the early stage of major illness, but also compensate for the loss of income caused by illness, the loss of not being able to continue working, the cost of rehabilitation treatment, etc., to prevent the decline in quality of life due to illness.

Accident insurance

Accident insurance is used to transfer financial losses resulting from death, disability or other accidents agreed upon in the insurance contract due to an accident.

First of all, the coverage should cover all accidental disabilities, not just traffic accidents, accidental deaths, and accidental total disabilities.

Second, the sum insured should be high. Disability can cause loss of income or interruption, long-term recovery, nursing expenses, and financial losses are sometimes greater than death.

Life

Life insurance is to allow us to fulfill our financial responsibilities to the family regardless of whether we are there or not. If a person has 1 million life insurance, then when he leaves, he can leave 1 million for his family.

The sum insured for life insurance should cover the following parts:

(1) Debts, including housing loans, car loans, etc.;

(2) child support (until they become financially independent);

(3) Parental maintenance;

(4) If the other half's income is lower than that of the insured, the basic living expenses of the family in the next 10 years should also be considered.

2. The second seat belt: manage wealth

The protection of existing wealth can rely on home property insurance, car insurance, etc., but the management wealth is not limited to this, but also involves the appreciation and inheritance of wealth. Therefore, the following insurance instruments are also necessary.

Annuity insurance

(1) Continuous cash flow

The payment of life annuity insurance is conditional on survival, as long as it is alive, the insurance company needs to pay the insurance premium in accordance with the agreement of the insurance policy, ensuring a steady stream of cash flow.

(2) Mandatory savings

According to the insurance contract, if the purchase of annuity insurance is cut off or surrendered to cash, it will bear losses. As a result, annuity insurance indirectly plays the role of compulsory savings.

(3) The benefits are clear

Annuity insurance has a cash value. The amount of money received corresponds to how much money can be received in the future, locks in the income in advance, writes it into the insurance contract, and the income is guaranteed.

Increased whole life insurance

Incremental whole life insurance is essentially a life insurance product, and "increased" means that its sum insured will increase, and the higher the corresponding cash value in the future. In the same year, like gold insurance, it also has the advantages of safety and stability, stable income and so on.

In addition, since the assets of the incremental whole life insurance policy belong to the insured, the insured has absolute control over it. Therefore, in actual life, it can play a role in debt isolation, asset inheritance, marriage wealth planning, tax planning, etc., and is very suitable for wealth inheritance and asset planning by high-net-worth individuals.

Insurance Fund Trust

If there is a higher demand for family wealth management, you can use the insurance fund trust.

An insurance fund trust is a family trust with the right to the proceeds of the policy as the trust property, and its advantages are as follows.

(1) Help high-net-worth individuals complete more complex wealth management needs

The insurance fund trust is an insurance plan during the validity period of the policy, when the claim conditions are met and the policy is paid, the insurance premium enters the trust account, the insurance contract is terminated, and the trust property begins to really operate, so the insurance fund trust can be regarded as a tool for the remanagement of the insurance premium.

(2) Prevent the risk of asset division brought about by marriage changes

The breakdown of a marriage is often accompanied by the division of property, and an insurance fund trust can be used to provide pre-existing conditional isolation and distribution of the child's marital risk.

(3) To a certain extent, help the insured or beneficiary to achieve asset isolation protection

There are no tax issues with insurance benefits, no problems with matrimonial property conforring, and no debt disputes. Therefore, the insurance premium is the least controversial and exclusive property of the beneficiary, and based on this legal structure, the insurance fund trust is superior to other single financial instruments in terms of asset segregation protection.

03

epilogue

As a "safety belt of life", insurance not only protects our present, but also protects our future. There may be ditches and bumps on the road of life, but wearing seat belts and configuring insurance can protect us all the way to a better future.