2021 has just come to an end, and last year was a special year for the real estate industry.

If the introduction of the "three red lines" in the second half of 2020 is only a "firecracker" under the regulation of "housing and not speculation", then the successive regulatory policies from the supply side and the financing side are another "bomb" in the industry. With the outbreak of risk events for individual housing enterprises, the real estate industry has changed the logic of high leverage and high turnover.

On the other hand, since last November, there have also been signs of marginal easing in property policy. From the policy point of view, there are more and more signals to promote the healthy development and virtuous circle of the real estate market, which has also made the real estate sector pick up.

The author noted that after hours on January 14, Longguang Group (3380. HK) issued an announcement that it had purchased US$20 million in principal 2022 notes on the open market. Generally speaking, the repurchase of housing enterprises can convey a certain confidence to the market when the industry is downturned, so how should the company's investment opportunities be viewed at present?

First, the financial basic situation is stable, and the debt structure is continuously optimized

In the face of the overall pressure of the industry, in the past year, the coldness of real estate stocks has become the consensus of the market. However, Longguang Group is still frequently supported by investment institutions. In the past two months alone, the company has successively obtained the optimism of many major banks at home and abroad, including Citi, Deutsche Bank, BOCOM International, CITIC Construction Investment, CCB International and so on.

Citi pointed out in its December 2021 report that Longguang Group is financially sound, the "three red lines" have fully reached the standard, the proportion of soil storage in first- and second-tier cities accounts for more than 90%, the soil storage development cycle is reasonable, and the contract sales and performance in the next 3 years are expected to pass through the cycle and remain stable, with significant competitive advantages, and will benefit from industry integration and continue to expand market share. At the same time, Citi also believes that Longguang stock is significantly undervalued and is the long-term value choice of investors. On January 5, Citi continued to issue research reports predicting that as market volatility and risks subside, the low valuation of domestic housing stocks will not last long, and it is optimistic about companies with defensive and growth momentum, of which Longguang Group ranks among its first choices.

In the author's view, the underlying logic of the current market investment in housing enterprises is first and foremost its financial quality and the stability of cash flow. This may be an important reason why Longguang, which has always performed steadily, has been unanimously optimistic about the institution.

According to public data, Longguang Group's financial stability maintains a green file, its net debt ratio is 60.8%, the asset-liability ratio after excluding pre-collection is 69%, the cash short-term debt ratio is 1.85 times, and the indicator performance is outstanding, showing that Longguang Group has stable financial management, low capital leverage, reasonable debt structure, abundant working capital, strong solvency, and is a stable housing enterprise.

In addition, in the first half of 2021, the company's new financing cost was 4.60%, and the comprehensive financing cost was 5.40%, down 0.2 percentage points from 2020 and the lowest level since listing. The main rating agencies also maintain the company's rating and are optimistic about longguang group's stable finances and excellent credit level. In this regard, Citi also mentioned in its previous report that the company's high-quality assets and sound financial control have always been highly recognized by financial institutions.

It is noted that since the end of last year, the real estate policy has continuously released positive signals, the financing environment has improved, and in the face of a good market window, Longguang has also actively exerted efforts at the financing level.

On December 28, 2021, Longguang Group also announced that Shenzhen Longguang Holdings Co., Ltd., a wholly-owned subsidiary of the Company, successfully issued RMB665 million of asset-backed securities to qualified investors on December 27. The securities received the highest credit rating from AAAsf for a period of 12 years and a coupon rate of 5.2% per annum. In this regard, BOCOM International commented in the research report that as a small number of developers with stable finances and high-quality assets, Longguang Group's financing channels have continued to remain smooth, and the company has successfully obtained the wholesale bank CMBS, which shows the full recognition of the company by the government and investors. Bocom also believes that the company's performance in 2022 will continue to remain stable, the financial maintenance of the "green file", the dividend will continue to be generous, and the competitive advantage will be expanded during the industry consolidation period, which is the value choice of investors.

In fact, Longguang Group has also had a number of bills repurchased in advance since the second half of last year. In this regard, Longguang said in the announcement that the repurchase of its senior notes will reduce the company's future financial expenses and reduce the level of its financial assets and liabilities, so it is in line with the overall interests of the company and its shareholders. The Company will continue to monitor market conditions and its financial structure and may further repurchase its senior notes in due course.

Longguang's active repurchase notes in the market are also enough to prove the stability of the company's cash flow to a certain extent.

In the author's view, combined with the real estate market environment this year, next year's policy will not change in the intention of stabilizing the market, and with the decline in industry concentration, high-quality private housing enterprises such as Longguang Group are a stage that highlights the core competitiveness. In addition, the corporate financing system is also changing, and high-quality housing enterprises need to continuously optimize the debt structure and improve their ability to cope with market risks on the basis of maintaining high-quality financial fundamentals.

Second, from the two dimensions of core competitiveness to explore the company's long-term investment value

At present, the industry is moving in the general direction of stable and healthy development, large-scale land development, high turnover and high leverage of the operating model has been eliminated by the market, the future housing enterprises if they want to have long-term stable development capabilities under the stock game, or have core competitiveness, and soil storage resources, product strength these two dimensions are in it.

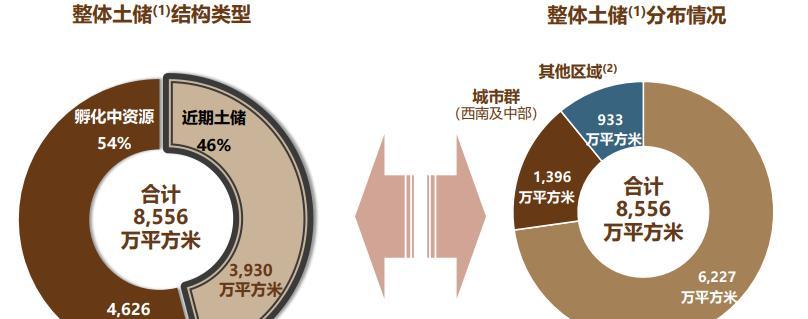

1) High-quality and reasonable soil storage structure as a source of power

Judging from the public data, Longguang Group uses the strategic focus of "urban comprehensive service provider" to seek differentiated advantages rather than blind expansion.

(Photo: Soil storage data for the first half of 2021 Source: Company's official website)

It is worth mentioning that most of Longguang Group's urban renewal projects are located in areas with great value potential, about 93% are located in the core cities of the Guangdong-Hong Kong-Macao Greater Bay Area, the project has performed outstanding in continuous expansion and transformation of value capabilities, and has successfully converted goods with a value of more than 90 billion yuan in the past three years, and the sustainable development capabilities of core urban renewal projects will continue to promote the long-term development of the company.

As an important asset reserve of housing enterprises, the value of soil storage cannot be ignored, when the soil storage is converted into a saleable real estate, its value can be further released, but the value of different regions varies greatly, from the perspective of soil storage, Longguang Group's soil storage resource structure is reasonable, high-energy city layout is of high quality, and the development cycle of soil storage is reasonable, which is one of the company's well-deserved core competitiveness.

2) The product strength is highlighted, and the multi-project inspires the future growth

The post-real estate era can be said to be the era of competitive products, and product strength, as the core competitiveness of housing enterprises, is expected to help enterprises seize more market share and break through in the stock competition.

The author believes that the measurement of the product strength of housing enterprises needs to consider the marketability of their products, or it can be measured by the speed of product sales.

On January 10, Longguang announced its sales results, and the company achieved equity contract sales of approximately RMB13.05 billion in December 2021, an increase of 18% month-on-month. As of December 31, Longguang achieved equity contract sales of about 140.2 billion yuan in 2021, an increase of 16.2% year-on-year. In this regard, the degree of dematerialization of its products is quite high.

At the same time, it is understood that Longguang Group has abundant sellable resources and continues to create refined products, and its product strength has been recognized by the industry. Since the second half of last year, Longguang Group has won a number of awards related to product power, such as on December 19, it ranked 15th in the "2021 China Real Estate Enterprise Super Product Power Top 100" in the "2021 Super Product Power Innovation Conference" hosted by Yihan Think Tank.

In this regard, the relevant person in charge of Longguang Group also mentioned, "Customer demand is the driving force for Longguang's product exploration." With the change of the times, people's living needs are also constantly upgrading and changing, around the positioning of urban integrated service providers, these changes will continue to become an important basis for Longguang polishing products. In the future, Longguang will continue to focus on product innovation and upgrading to create value for customers. ”

In addition to development business, Longguang Group actively enhances its sustainable management capabilities, and its commercial projects are also continuously empowered. Its commercial real estate projects were also recognized, and in late December, the company's Shenzhen Bright Blue Whale World was awarded the "2021 China TOD Commercial Complex Benchmarking Project TOP5". After the opening of Bright Blue Whale World at the end of last year, it attracted more than 220 brands to settle in, and the average passenger flow on the first sunday of opening exceeded 100,000 people, which was quite hot.

It is reported that Shenzhen Guangming Blue Whale World is a large degree of excavation and exploration of Longguang's todd function value, which organically integrates shopping malls with theme shopping streets, selected hotels, best residences, ecological parks and other formats to form a three-dimensional micro-urban space integrating transportation, commerce, commerce, culture, parks, residences and other functions, improving the land premium rate and enhancing the core competitiveness of products and regional support.

(Photo: Shenzhen Bright Blue Whale World)

III. Conclusion

From the perspective of the industry, the intention of policy regulation to promote the healthy development of the real estate market is obvious, and the financing end may usher in a temporary relaxation and alleviate the financial pressure of housing enterprises, but the tone of housing and housing is always unchanged. Just like the current continuous signal transmission, the worst year of the real estate industry is about to pass, and the future will move towards an exploration model of high-quality development. In the competition of supply-side reform of the industry, high-quality private housing enterprises such as Longguang Group have demonstrated their steady financial management capabilities, high-quality soil storage resources and differentiated product strength, which are the indispensable core competitiveness of housing enterprises. It is worth mentioning that in the recent Hurun Research Institute released the "2021 Hurun Top 100 Private Enterprises sustainable development list in China", listing 100 Chinese private enterprises that are most in line with the 17 sustainable development goals of the United Nations, Longguang Group (03380. HK) is also among them, once again proving its comprehensive strength.

Looking forward to 2022, Longguang Group's leading ability in profitability is worth looking forward to, and its high dividend payout ratio is also one of the investment attractions, which deserves long-term attention.