21st Century Business Herald reporter Zhu Yiyi reported from Hangzhou

Pharmacy business, what's next?

After more than ten years of horse racing, Yixintang (002727. SZ), Yifeng Pharmacy (603939. SH), ordinary people (603883. SH), Large Ginseng Forest (603233. SH), which landed on the capital market from 2014 to 2017.

They are consistent with the established listed Sinopharm (000028. SZ) together, became the five giants of A-share pharmaceutical retail.

However, just when everyone thought that the pattern had been determined, Gaoji Medical, a wholly-owned subsidiary of Hillhouse Capital, was born in 2017.

In just two years, through mergers and acquisitions of more than 10,000 physical pharmacies, it has become the largest pharmacy chain brand in China and stirred up a pool of spring water.

The addition of capital has made this "pharmacy" battle once hot.

However, with the cooling of asset prices in the industry, the integration problems brought about by large-scale mergers and acquisitions have become prominent, especially in the special context of the "new crown" epidemic, pharmacy operations are also facing higher and higher compliance costs.

Public data shows that the number of pharmacies nationwide reached a record of more than 550,000 in 2020.

What kind of governance problems does this cash-rich business face?

On October 23, Beijing Changping reported that the two confirmed cases of the "new crown" epidemic in the Hongfuyuan community of Beiqijia Town had purchased Lianhua Qing plague capsules, licorice tablets and other drugs at the "Eleventh Branch of Beijing Desheng Kangda Pharmacy Co., Ltd." and "Beijing Gaoyuan Baikang Zhu You Health Pharmaceutical Co., Ltd."

When selling "four types of drugs" such as fever reduction and cough suppression, the two pharmacies did not register customer identity information, did not require customers to scan health codes, temperature measurements, etc., and purchased "four types of drugs" without real-name registration of drug sales information.

In stark contrast, in August 2021 and September 2021, the Market Supervision Institute of Beiqijia Town, Changping District, conducted several supervision and inspections of the above two pharmacies, and did not find relevant problems, until the outbreak of the "new crown" epidemic in the Hongfuyuan community of Beiqijia Town.

Beijing Gaoyuan Baikang Zhuyou Health Pharmaceutical Co., Ltd., the indirect major shareholder is Gaoji Pharmaceutical Co., Ltd., after penetration, it is Gaoji Medical under Hillhouse Capital that lays out the field of big health.

This is not the first time that Gaoji Medical has been on the official "blacklist".

On February 10, 2020, the Shanghai Municipal Administration for Market Supervision and Administration exposed a number of typical cases of "masks" violating the law, including a Xincun Road store of Shanghai Wanyun Pharmacy Chain Co., Ltd. that was investigated and punished for "suspected price gouging". The pharmacy imported 200 boxes (50 packs) of "disposable non-woven masks" from its corporate headquarters at a purchase price of 35 yuan / box, and finally sold them at a price of 98 yuan / box.

Coincidentally.

In June this year, the Shanghai Municipal Food and Drug Administration released an administrative penalty information showing that the Shanghai Chain Store of Guoda Fumeida Pharmacy Shanghai Chain Co., Ltd., a subsidiary of Sinopharm Holdings, was suspected of selling prescription drugs and Class A non-prescription drugs when a practicing pharmacist was not on duty, and the Shanghai Municipal Food and Drug Administration issued a warning penalty to the pharmacy.

In addition, in July 2020, due to the sale of inferior drugs, Lao people's wholly-owned subsidiary Of Lao People Pharmacy Chain (Shanghai) Co., Ltd. was fined 3665.4 yuan.

Although compliance issues arise from time to time, there is no doubt that the "capital side" has paid more attention to the revenue growth brought about by the high-flying mergers and acquisitions for a long time.

According to public data, Gaoji Medical, which has the largest chain of pharmacies in China, has a retail revenue of more than 30 billion yuan in 2018, while Yixintang, which was founded in 2000 and has a history of 18 years, had a revenue of 9.176 billion yuan in 2018, and the revenue of the people who came out in 2005 was 9.47 billion yuan.

Moreover, in the case of "financing difficulties" in many industries in 2018, the downstream of the pharmacy retail field directly faces consumers, with less advance receipts and still abundant cash, which is obviously a business that serves as a "cash cow".

As of the end of the third quarter of 2021, the monetary funds on the books of Yixintang were 2.117 billion yuan; the monetary funds on the books of Yifeng Pharmacy were 2.121 billion yuan; and the monetary funds on the books of Dasanlin were 2.658 billion yuan.

From the price trend of pharmacy assets, we can also see the change of the "acquisition expansion" heat of pharmacy leaders.

Public information shows that from 2014 to 2017, four major chain pharmacies of Yixintang, Yifeng Pharmacy, Ordinary People and Da ginseng lin have been listed one after another.

After the listing, these companies switched from self-construction to mergers and acquisitions, and began to acquire, pushing the PS (price-to-sales ratio, that is, total market value/sales) of pharmacies from 0.5 to about 0.8.

In June 2018, Yifeng Pharmacy acquired 86.31% of the equity of Shijiazhuang Xinxing Pharmacy Chain Co., Ltd. for 1.384 billion yuan (issuing shares and paying cash), known as "the first case of merger and acquisition in the pharmacy industry".

The deal set a record for acquisitions in the chain pharmacy industry at that time, with a PS of 1.87.

The overall valuation of 475 pharmacies in Xinxing Pharmacy is 1.603 billion yuan, and the average purchase price of single-room pharmacies has risen to 3.3684 million yuan.

In stark contrast, three months ago, in March 2018, Yifeng Pharmacy acquired 15 chain pharmacies affiliated to Hunan Xinbaikang Pharmaceutical Chain Co., Ltd. and 6 single pharmacies such as Yuanjiang Kangtai Pharmacy and Yuanjiang Renxin Pharmacy, with 21 retail pharmacies with a purchase price of 62.202 million yuan, excluding inventory of 7.202 million yuan, and the average purchase price of a single pharmacy was 2.92 million yuan.

In the golden age of retail pharmacies, pharmacy-listed companies are almost close to hand-to-hand combat, and in just a few months, the acquisition price has risen.

Yifeng Pharmacy, which is active in the market with the image of "mergers and acquisitions", said in its 2018 annual report, "Since its listing in February 2015, there have been nearly 40 mergers and acquisitions integration projects, involving more than 1,500 stores, and all projects have achieved performance expectations." ”

During the reporting period, Yifeng Pharmacy signed 13 new mergers and acquisitions projects, completed the delivery of 6 mergers and acquisitions projects in the previous year, added 959 new mergers and acquisitions stores, and successfully completed the major asset restructuring of emerging pharmacies.

Another listed pharmacy company, Dashanlin, also accelerated the pace of mergers and acquisitions in the same industry in 2018.

In that year, Dashanlin participated in 14 mergers and acquisitions in the same industry, including 8 wholly-owned or controlled acquisition projects, involving 146 stores (including 57 undelivered stores that have been signed); 6 equity investment projects, with an investment cost of 82.3272 million yuan.

In the second half of 2018, Gaoji Medical passed through large-scale acquisitions, and the number of pharmacies under it exceeded 10,000, which was much higher than that of several major listed pharmacy companies.

With fewer buyers and a return to rationality in the industry, the valuation of pharmacy assets fell significantly in the first half of 2019.

Take, for example, a acquisition by Dashanlin in March 2019, which acquired a 46% stake in Baoding Shengshi Huaxing Pharmaceutical Chain Co., Ltd. for 74.245 million yuan.

At this point, PS has dropped to 0.872.

Pharmacies are an important part of the "last mile" of people's livelihood.

On October 21 this year, the Ministry of Commerce issued the "Guiding Opinions on Promoting the High-quality Development of the Pharmaceutical Circulation Industry during the 14th Five-Year Plan Period", proposing the goal of "cultivating 1-3 large-scale digital and comprehensive drug circulation enterprises of more than 500 billion yuan and 5-10 large-scale digital and comprehensive drug circulation enterprises of more than 500 billion yuan by 2025, 5-10 specialized and diversified pharmaceutical retail chain enterprises of more than 50 billion yuan, and about 100 intelligent, characteristic and platform-based pharmaceutical supply chain service enterprises".

On May 17, Jointown (600998. SH) Vice Chairman Liu Zhaonian also stated at the 2020 shareholders' meeting that the company will continue to strengthen the layout of the pharmaceutical retail network.

Jointown attracts individual pharmacies and small and medium-sized chain enterprises to join through the "10,000 stores alliance model", and strives to sign 5,000 franchised pharmacies in 2021, and plans to add 30,000 pharmacies in 3 years.

Among the five listed chain pharmacy enterprises with obvious "regional" characteristics: the pharmacies of the common people are mainly distributed in central China and east China, the deep ploughing area of Dashenlin is based in South China, and Yixintang focuses on the development of southwest China and South China, while taking into account the development of stores in North China, and the core market of Yifeng Pharmacy is concentrated in Central China, East China and North China.

In addition, Sinopharm's Guoda Pharmacy has formed a network of pharmacies covering the coastal urban agglomerations of East China, North China and South China, and has gradually spread into the Northwest, Central Plains and Inland City Clusters.

These five companies have not given up the pace of mergers and acquisitions.

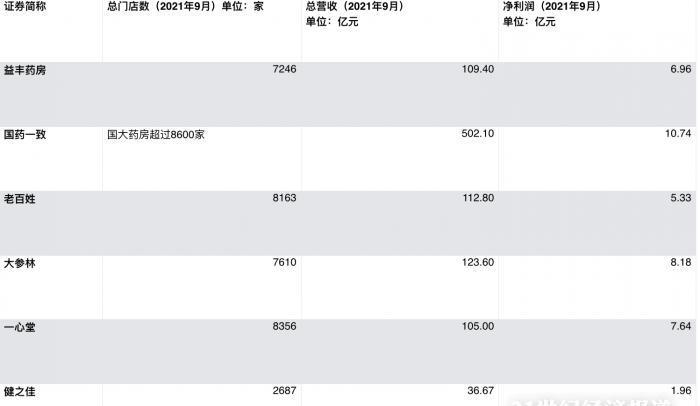

The 21st Century Business Herald reporter combed the annual reports of listed companies and found that as of the end of September 2021, the total number of stores of Yifeng Pharmacy, NUS Pharmacy, Ordinary People, Dashanlin and Yixintang was 7246, more than 8600, 8163, 7610 and 8356 respectively.

On November 11, Sinopharm unanimously said on the investor interactive platform that as of the end of the third quarter of 2021, the total number of stores of NUS pharmacies exceeded 8,600, becoming a listed pharmacy with a relatively large number of stores.

In addition, in the first three quarters of this year, Yifeng Pharmacy had a total of 7246 stores (including 877 franchised stores).

From January to September 2021, Yifeng Pharmacy added 1255 stores, including 1051 new stores (including 242 newly opened franchise stores), 280 M&A stores, and 76 closed stores.

Among them, Yifeng Pharmacy had 7 M&A investment businesses in the same industry during the reporting period, of which 4 were M&A delivery projects and 3 projects were in progress; 133 stores were involved, of which 66 were completed.

From the performance point of view, Yifeng Pharmacy achieved revenue of 10.940 billion yuan in the first three quarters of 2021, an increase of 16% year-on-year, and a net profit of 696 million yuan, an increase of 21% year-on-year.

Will companies continue to expand their revenue through mergers and acquisitions?

On November 15, the 21st Century Business Herald reporter called the securities affairs department of Yifeng Pharmacy as an investor, and the other party only said that "it is necessary to consult the investment department of the company, and the specific situation is not clear."

As of the third quarter of 2021, Dashanlin has 7610 stores (including 738 franchise stores), and in the first three quarters of 2021, Dashanlin has a net increase of 1590 stores, of which: 829 new stores, 416 acquired stores, 423 franchised stores, and 78 closed stores.

In the first three quarters of 2021, Da ginseng forest achieved revenue of 12.360 billion yuan, an increase of 18% year-on-year, but the net profit was 818 million yuan, down 5% year-on-year.

For the situation that the increase in revenue does not increase profits, on November 15, a person from the Securities Affairs Department of Dashanlin explained that "the base of last year was too high" .

As for the distribution of the company's self-built and acquired pharmacies, the person mentioned that "(the company)'s self-built stores will be more, because the cost is relatively low, and the cost of the acquired pharmacies will be higher." ”

Another listed pharmacy leader, Yixintang, disclosed that as of the end of the third quarter of 2021, the company's chain of directly operated stores reached 8356. In the third quarter, Yixintang built 1,300 new stores, closed 26 stores due to urban transformation and strategic location adjustments, relocated 123 stores, and added 1,151 stores.

As of the end of the third quarter of 2021, the people have 8163 stores (6055 directly operated stores and 2108 franchised stores), of which in the third quarter of 2021, the people have added 1866 stores, of which 1259 are directly operated (724 are self-built, 143 are asset acquisitions, 392 are equity mergers and acquisitions), and 607 are franchised new stores.

On October 29, when the people accepted a telephone survey of 113 institutional investors such as CITIC Securities, Industrial Securities, Bocom Schroders, Huatai Assets, Xingquan Fund, Harvest Fund, etc., some investors asked, "The company began to implement the regional focus strategy in 2019, and mergers and acquisitions in Inner Mongolia, Shanxi, Gansu and other provinces continued to advance, what is the effect of the implementation of the regional focus strategy at present?" ”

In this regard, the people said, "At present, the concentration of pharmaceutical retail in China is not high enough, which is also a development opportunity for the entire industry." The company's gathering strategy focuses on relatively low-competitive markets, creating a moat by increasing regional market share. For the original layout of the "7 + 1" provincial capital city, the company does not intend to increase the density of stores next, but to quickly do e-commerce integration, through the flatness of each single store and the coverage of public domain traffic to quickly improve, online and offline integration to seize the market share of competitors. ”

In addition, Xie Zilong, chairman of the people's board, also mentioned in a public statement that drug collection is more beneficial to the retail industry, "pharmaceutical companies that have not entered the collection will be more inclined to choose to cooperate with pharmacies, which will bring more gross profit margins to retail pharmacies."

According to data from the intranet, in 2020, the sales of drugs in the six major markets of China's three major terminals reached 1,643.7 billion yuan, and from the perspective of the sales distribution of the three major terminals, the public hospital terminal market share is the largest, accounting for 64.0% in 2020; the retail pharmacy terminal market share will account for 26.3% in 2020; and the public primary medical terminal market share will account for 9.7% in 2020.

Although the proportion of medical terminals is still several times that of retail pharmacies, pharmacies are obviously attracting attention from the perspective of growth rate.

Another set of data shows that the terminal market size of public hospitals reached 1,051.2 billion yuan in 2020, down 12% year-on-year; while the retail pharmacy terminal market reached 433 billion yuan in 2020, an increase of 3.2% year-on-year.

For more information, please download the 21 Finance APP

!["Dog Head Loli" returns, the cow swimsuit shows off her figure, netizens: Selling pancakes is not as profitable as this industry[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)