In the U.S., anyone who has ever bought a new or used car through a car dealership knows that while it's often fun to look for a car and find the one that works best for them, most people are afraid of the finance office, according to SlashGear. In the finance office, car buyers are often asked to add various ancillary guarantees and services, which can cause people to pay a big price for a new car each month.

SlashGear said anyone who has sold a car is probably familiar with the tactics called "holding points" that take place in the finance office. For example, when someone's credit score matches the 1.9% interest rate, the phenomenon of "holding points" occurs. However, many dealers and banks allow treasury offices to add percentage points to this rate, where the term "holding points" comes from. If the buyer agrees, the buyer's interest rate may be significantly higher than their credit qualification. So people's hard work and good credit make them get an interest rate of 1.9 percent, rather than eventually paying 3.9 percent, 4.9 percent, or even more, depending on the dealer and the state. This extra money usually goes to the dealer.

Most dealers won't say they're doing this to buyers, and it's a common practice. However, the people of Consumer Reports have investigated auto loans over the past year and confirmed that many auto buyers pay a lot of money for their loans. Perhaps the most disturbing thing the survey found was that, in some cases, consumers with good credit who were eligible for preferential interest rates were placed on subprime loans.

One example given in the survey is that a Maryland resident bought a 2018 Toyota Camry at a 19 percent rate two years ago, despite his good credit. Of course, in such a situation, many people will put the blame on the buyer because he agreed to such a high interest rate and did not understand the car purchase process and their credit before buying a car. In contrast, the survey found that in similar transactions, buyers with similar credit scores received interest rates of about 4.5 percent. This means that despite the buyer's good credit, he paid 14.5% more interest in the first case.

While it may be rare to hit a person who is eligible for a quality loan with such a high interest rate, the process of increasing the annual interest rate by a few percentage points is certainly not the case. For some dealers, "holding points" is an extremely common practice that happens in every transaction they think they can do.

Often, the best way to combat something like this is to understand the buyer's own credit score, and what the interest rate might be. Credit Karma, and many of the credit scores offered by banks and credit cards through their apps and websites, are not based on the types of scores commonly used by auto lenders. Buyers can learn their ratings by using the services of credit scorers directly.

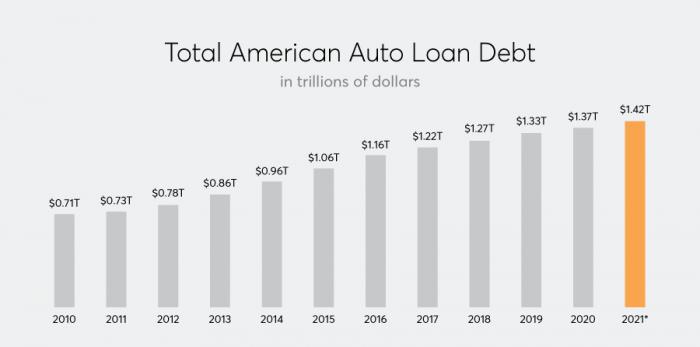

Another interesting fact in the survey is that average monthly car payments have risen a lot compared to a decade ago. Today, buyers pay an average of nearly $600 a month, a 25 percent increase compared to 10 years ago. Although the average loan term has been greatly extended, the average monthly payment has increased by 25%.

Most automakers' lenders will lend cars up to 84 months, and many typically opt for a 72-month loan. For those who plan to keep their cars after the loan repayment period ends, such a long loan term may not be a problem. However, for many buyers who only intend to keep the car for a few years, a longer loan term means paying more interest and more negative equity when they are ready to change cars.

![This village chronicle records many touching stories of "filial piety and love for relatives......[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)