U.S. stocks close: technology stocks sold off, the NASDAQ fell more than 1% after last week's plunge, and Tesla fell more than 6%

Last week, the wave of interest rate hikes set off by central banks in the United Kingdom and other places triggered recession fears, and European and American stock markets fell collectively. U.S. stocks started the week with modest volatility in the closing week of June, struggling to find their way as investors weighed whether repeated rate hikes by major central banks would lead to a recession. After its biggest weekly decline in three months, the Nasdaq rebounded and lost on Monday, turning lower during the session, and both the S&P Dow fell to a more than two-week trough.

While chip stocks rebounded overall, many blue-chip tech stocks continued to fall, dragging down the broader market. Tesla's share price tumbled as Goldman Sachs, which is considered highly valued, to fall more than 6 percent in a day for the first time in more than two months. Commented that last week Fed Chairman Jerome Powell was still hinting that higher interest rates would remain longer, U.S. stocks underwent a correction, after a number of blue-chip technology stocks soared, U.S. stocks are now showing a rotation of funds to small-cap stocks and value stocks. In addition, Russia's Wagner "rebellion" on Saturday hit risk appetite.

Germany's IFO business index for June, released on Monday, fell more than expected, falling for the second consecutive month. Key German Bund Yield Curve – The yield curve for two- and 10-year German bonds hit its worst inversion since 1992 for the third straight session, highlighting concerns about the economic outlook.

In terms of foreign exchange markets, Japan's vice minister for international affairs at the Ministry of Finance said that the yen has fluctuated rapidly unilaterally recently, and Japan will not rule out any option that may respond to excessive foreign exchange fluctuations. Kanda warned of a slight rebound in the yen, which briefly recovered 143.00 against the dollar, temporarily halting a six-session streak of hitting a seven-month low and remaining near a seven-month low. The dollar index fell to a one-week high.

Among commodities, the Wagner mutiny has attracted market attention, the geopolitical situation related to Russia has disrupted the outlook for supply, and international crude oil has rebounded, leaving a one-week low hit by a week of consecutive declines. Gold continued to emerge from a three-month trough hit on Thursday, supported by a pullback in the dollar.

Tesla posted its biggest decline in more than two months, and the sectors where Meta and Google were located led the decline, and banks in the S&P region bucked the market higher

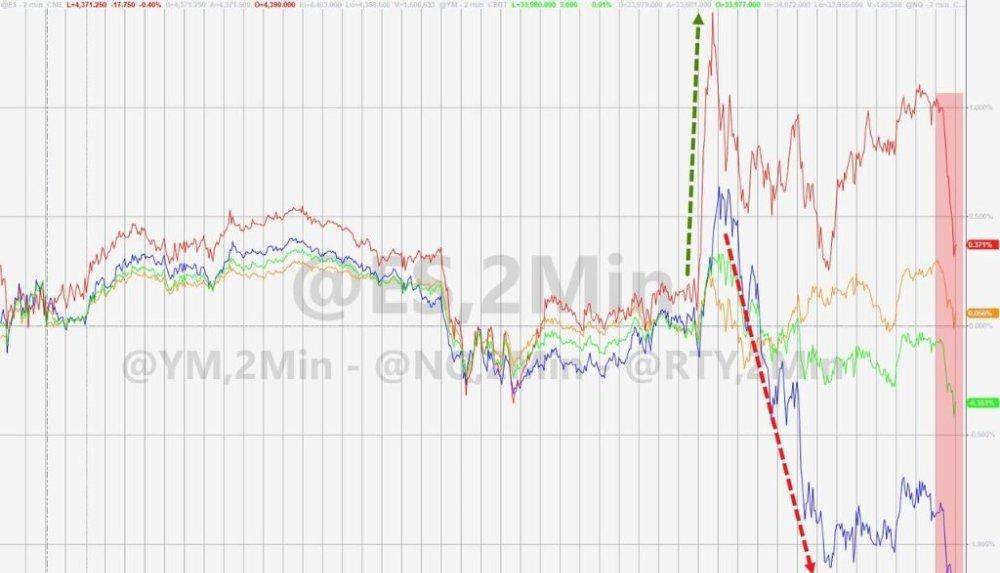

All three major U.S. stock indexes rose in early trading and turned lower later. The low-opening S&P 500 and Nasdaq Composite quickly turned higher and then turned lower. The Nasdaq, which fell nearly 0.2% at the beginning of the session, rose 0.6% after about half an hour after the open, turned lower at the end of the morning and continued to decline, falling nearly 1.2% in late trading. The S&P rose more than 0.3% at the beginning of the session, turned lower after opening more than an hour, and fell nearly 0.5% in late trading. The Dow Jones Industrial Average, which opened slightly higher, turned lower after opening more than half an hour, and since then fell more than 117 points, or more than 0.3%, turned higher at the end of the morning, rose more than 90 points, nearly 0.3%, and turned lower at the end of the day.

In the end, the three major indexes closed down collectively for two consecutive trading days. The Nasdaq closed down 1.16% at 13,335.78, the S&P closed down 0.45% at 4,328.82, and the Nasdaq hit its lowest close since June 9. The Dow closed down 12.72 points, or 0.04%, at 33,714.71, falling for six consecutive days and updating its lowest level since June 7 for two consecutive days.

The tech-heavy Nasdaq 100 index closed down 1.36%, underperforming the broader market, posting its biggest closing decline since June 7 and falling for two consecutive days to its lowest level since June 9. The Russell 2000, a value-based small-cap index, closed up 0.09%, bidding farewell to the five-day losing streak and refreshing its two-day streak since June 5.

Major U.S. stock indexes turned lower for most intraday sessions on Monday, with small-cap indexes closing slightly higher

Five of the S&P 500 sectors closed lower on Monday, led by Meta and Google's communications services closing down nearly 1.9 percent, Tesla's consumer discretionary down nearly 1.3 percent, Nvidia's IT down about 1 percent, and healthcare and financials down 0.6 percent and 0.2 percent, respectively. Among the six sectors that closed higher, property led the way with a 2.2 percent rise, energy up 1.7 percent, materials and utilities up about 1 percent, industrials up 0.8 percent and consumer staples edged higher.

Leading technology stocks closed lower across the board. Tesla, which was downgraded by Goldman Sachs from buy to neutral in early trading, returned to the downtrend after turning up in the short term, closing down nearly 6.1%, the biggest daily decline since the next day after the 24% drop in net profit in the first quarter announced on April 20, and fell for two consecutive days to close the lowest since June 8.

Among the six major technology stocks of FAANMG, Facebook's parent company Meta, which updated its high since January last year for two consecutive days, closed down nearly 3.6%, falling back to its lowest level since June 14; Google's parent company Alphabet closed down nearly 3.3%, falling for two consecutive years to its lowest level since May 15, after UBS downgraded its rating from buy to neutral because it believed that future upside was limited and that the shift to AI could affect financial results in the near term.

Chip stocks that underperformed the broader market on Friday generally rebounded, with the Philadelphia semiconductor index rising more than 2 percent in early trading before giving up most of its gains to close up nearly 0.3 percent, and semiconductor industry ETF SOXX closing up about 0.3 percent. Among the individual stocks, Globalfoundries closed up 3.8%, Qualcomm rose more than 3% at midday, closed up 2.8%, ON Semiconductor, Intel closed up more than 1%, Micron Technology rose nearly 0.3%, Broadcom, which had risen more than 1% in early trading, closed slightly lower, and Nvidia, which had risen more than 1% in early trading, turned down, fell more than 4% at midday and closed down more than 3.7%, and will fall for four consecutive days to the lowest level since June 12 after hitting a record high on Tuesday, and AMD, which had risen more than 2% in early trading, closed down about 2.3%, falling for seven consecutive days to the lowest level since May 19.

Most AI concept stocks continued to fall. C3.ai (AI), which rose more than 6% at the beginning of the session, turned lower in early trading and closed down 4.3%, falling for six consecutive years to its lowest level since May 25; BigBear.ai (BBAI), which had risen more than 3% at the beginning of the session, closed down 2.6%; Palantir (PLTR), which had risen nearly 3% in early trading, turned lower at midday, closing down 0.6%, while Adobe (ADBE), which had risen 0.5% in early trading, closed down nearly 1.1%. The SoundHound.ai (SOUN) closed up 10.7%.

Banking indices rebounded after five consecutive days, with regional bank stocks doing better. The KBW Bank Index (BKX), a banking benchmark that repeatedly updated its lowest level since June 1 on Thursday and Friday, closed up more than 0.6%. The regional banking index KBW Nasdaq Regional Banking Index (KRX) and the regional bank stock ETF SPDR S&P Regional Banking ETF (KRE) both rose more than 2% at midday, closing up 1.2% and 1.3%, respectively, coming out of their lows since June 1 and May 31, respectively.

Among the big banks, Bank of America closed up nearly 1.2%, Citi rose nearly 0.5%, JPMorgan Chase rose more than 0.2%, while Morgan Stanley almost closed flat, Wells Fargo edged down and Goldman Sachs closed down nearly 0.8%. Among the banks in key regions, Western Pacific United Bank (PACW) rose more than 5% in midday trading and closed up 4% after selling a $3.5 billion asset-based mortgage portfolio to asset management company Ares Management Corp. to boost liquidity. WSFS Financial (WSFS) also rose more than 5 percent at midday to close up nearly 4.8 percent after Davidson upgraded its rating from neutral to buy, believing it could benefit from a longer-lasting environment with high interest rates.

Most of the popular Chinese concept stocks rebounded during the session. The Nasdaq Golden Dragon China Index (HXC), which has been falling for five days, rose more than 1% in early trading and closed up nearly 0.2%. Chinese ETF KWEB closed up 0.5 percent, while CQQQ closed down 0.4 percent. Among individual stocks, Xpeng Motors closed up more than 2%, Li Auto rose about 2%, Alibaba rose more than 1% intraday, closed up 0.7%, JD.com rose more than 1% at the beginning of the session, closed up 0.3%, Station B also closed up 0.3%, Baidu rose 0.2%, while NIO fell nearly 0.4%, Pinduoduo fell 0.2%, and Tencent Pink fell less than 0.1%.

Among the volatile stocks, Lucid Group (LCID), which announced that it will provide powertrain and battery systems for the British luxury car Aston Martin, rose 14.8% in early trading and closed up 1.5%; Despite a lower-than-expected second-quarter loss, Carnival Cruises (CCL) fell as much as 12 percent intraday and closed down 7.6 percent, while its peers Norwegian Cruise Line (NCLH) and Royal Caribbean Cruises (RCL) closed down 4.5 percent and 0.7 percent, respectively.

In European stocks, the pan-European stock index fell for six consecutive trading days. The Euro Stoxx 600 index updated its closing low since May 31 for three consecutive sessions. Stock indexes of major European countries were mixed on Monday. German and French stocks fell for six consecutive days, British stocks fell for five consecutive days, and Spanish and Italian stock indexes fell for three and two consecutive days respectively.

Among the Stoxx 600 sectors, the healthcare sector fell 1.1% to lead the decline, reflecting fears that the interest rate hike cycle will last longer and hit the economy. The oil and gas sector, which benefited from the rebound in oil prices, rose 0.8%.

Among individual stocks, after the withdrawal of the profit guidance for the current fiscal year on Friday and the estimated cost of wind turbine component failure exceeded 1 billion euros, Siemens Energy continued to fall, closing down nearly 2.1%, a significant reduction from 37.3% on Friday; After announcing that it would file for bankruptcy protection in the UK as part of a restructuring plan and suspend trading in shares next month, Cineworld Group, a British cinema chain, fell 26% intraday and closed down 17.9%; After the Russian Wagner mutiny quickly subsided, several major European defense companies Leonardo SpA, Saab AB and Rheinmetall AG all fell by more than 4%; Aston Martin, which has reached a deal with Lucid to produce high-performance electric vehicles, jumped 10.8%.

The yen rebounded slightly, temporarily halting the trend of hitting a new seven-month low The dollar index fell away from a one-week high

The ICE dollar index (DXY), which tracks the dollar against a basket of six major currencies including the euro, maintained its decline throughout the day on Monday and failed to regain 130.00, and U.S. stocks had been close to a daily low of 102.60 before the market, falling nearly 0.3% on the day, falling more than 0.5% from the intraday high since June 15 set by rising above 103.10 on Friday, and U.S. stocks narrowed losses in early trading, rising above 102.80 at the end of the morning, approaching the pre-market update intraday high in European stocks.

By Monday's close, the dollar index was below 102.80, down more than 0.1%; The Bloomberg Dollar Spot Index, which tracks the greenback against ten other currencies, fell less than 0.1 percent, saying goodbye to its high since June 13 and halting a two-day winning streak.

The Bloomberg dollar spot index has been trending since Tuesday

The yen rebounded slightly after Masato Kanda, an official of Japan's Ministry of Finance, spoke. USDJPY briefly fell below 143.00 in European stocks in the morning to refresh the daily low, down about 0.5% on the day, U.S. stocks rebounded before the market, U.S. stocks turned higher in early trading, once rose above 142.70 to refresh the daily high, approaching Friday's close to 143.90 and the sixth consecutive trading day to refresh the seven-month high, U.S. stocks closed at the 143.50 line, down about 0.1% on the day.

Other non-U.S. currencies turned higher overall, with the euro rising to a daily high of 1.0920 in U.S. stocks before the session, rising nearly 0.3% on the day, off Friday's intraday low since June 15. The pound against the dollar was close to a new daily high of 1.2750 in European trading in early trading, rising about 0.3% on the day, and U.S. stocks turned higher in early trading after European stocks turned lower in early trading, not close to Friday's intraday low since June 15 when it fell below 1.2690.

The offshore yuan (CNH) rose to a daily high of 7.2063 against the dollar in early Asian trading, and then continued to fall, and U.S. stocks fell to 7.2465 after hours, refreshing the low since November 29 last year for four consecutive trading days and losing 7.20 for three consecutive days. At 4:59 Beijing time on June 27, the offshore yuan was quoted at 7.2429 yuan against the US dollar, down 272 points from the end of New York on Friday, and fell for three consecutive trading days.

Bitcoin (BTC) rose above $30,600 at the beginning of the U.S. stock market to refresh the daily high, and then quickly retreated, the U.S. stock market fell below $30,000 to refresh the daily low at midday, down more than $700 from the daily high, down more than 2%, the U.S. stock market closed above $30,200, down less than 1% in the last 24 hours, continuing to fall from the high since June last year set by last Friday's rise of $31,400.

Two- and 10-year German bonds hit the worst yield inversion since 1992

European government bond prices rose in unison, and the yield on the 2-year British bond, which climbed more than 10 basis points sharply against the market on Friday, also retreated. The yield on the UK 10-year benchmark government note closed at 4.29%, down 2 basis points on the day, continuing to move away from the high since October last Tuesday that approached 4.50% to refresh; The yield on the 2-year British note closed at 5.12%, down 2 basis points on the day, and closed to 5.20% on Friday near the high since 2008; The yield on the benchmark 10-year German Bund, which fell more than 10 basis points on Friday, closed at 2.31%, down 5 basis points on the day, and European stocks fell below 2.30% at the beginning of the session, refreshing the low since June 2; The yield on the 2-year German bond closed at 3.07%, down 2 basis points on the day, continuing away from the March 9 high that approached 3.29% on Thursday.

In the European session, the spread between the 2-year and 10-year German bonds widened to -79.872 basis points, continuing to refresh the worst inversion in more than three decades, and the largest yield inversion since September 22, 1992.

The yield of the U.S. 10-year benchmark Treasury bond fell below 3.68% before the U.S. stock market, refreshing the low since Tuesday, June 13, last Friday, and fell more than 6 basis points during the day, and the decline narrowed after the opening of the U.S. stocks, standing above 3.70% at the beginning of the session, and tested 3.74% in early trading, smoothing the intraday decline, and about 3.72% by the end of the bond market, down nearly 2 basis points on the day.

The 2-year U.S. Treasury yield, which is more sensitive to the outlook for interest rates, fell below 4.70% to a daily low in U.S. stocks, flattened the decline in early trading and turned higher, rising as much as 4.76% at the end of the morning, starting close to the three-month high that was updated after rising above 4.80% last Thursday, and turned lower at midday, reaching about 4.74% by the end of the bond market, roughly unchanged from Friday's level.

U.S. Treasury yields of all maturities moved on Monday

Crude oil out of one-week low, intraday rose more than 1%

International crude oil futures have turned lower in both European and U.S. stocks, but the overall rebound momentum has not changed, when U.S. stocks updated their daily highs at midday, U.S. WTI crude oil broke through the $70 mark to $70.11, up nearly 1.4% on the day, and Brent crude rose to $75, up nearly 1.6% on the day.

WTI crude oil futures for August ended up $0.21, or 0.30 percent, at $69.37 a barrel. Brent crude oil futures for August ended up $0.33, or 0.45 percent, at $74.18 a barrel, and U.S. oil both broke away from the lowest levels since Wednesday, June 14, set on Thursday and Friday, but failed to erase the losses of the previous two days. On Thursday, U.S. oil and cloth oil closed down nearly 4.2% and 3.9%, respectively.

U.S. WTI crude futures turned lower more than once during the session on Monday before finally closing higher

U.S. gasoline and natural gas futures rose in unison. NYMEX July gasoline futures, which fell for two consecutive days, closed up 0.8% at $2.5375 per gallon, bidding farewell to the closing low since June 12 at $2.4826; NYMEX July natural gas futures closed up 2.3% at $2.791/MMBtu, refreshing the closing high since $2.84 on March 7 for two consecutive trading days, rising for four consecutive days.

London nickel fell more than 5% to 11-month low Gold continues to walk out of three-month lows

London base metals futures fell almost across the board on Monday, with only copper rising slightly, down from Friday's two-day losing streak to hit a more than one-week low. Nickel, which led the decline, fell more than $1,000 or more than 5% in one day, not only erasing Friday's rebound, but also closing near the $20,300 mark, a new low since July last year. Lunxi fell more than 3%, and Lunxi fell for three consecutive days, hitting new lows in more than two weeks and nearly three weeks, respectively. Lun aluminum fell for six consecutive days, after hitting a new low since October last year on Friday, and then closed at a new low since the end of September last year.

New York gold futures, which ended a three-day losing streak on Friday, continued to rally, and European stocks updated their daily high to $1943.4 in early trading on Monday, rising more than 0.7% on the day, and gradually gave up most of their gains since then.

Finally, COMEX gold futures for August ended up 0.22% at $1933.80 an ounce, continuing to walk out of the closing low since the March 16 closing at $1923, which fell below $1924 last Thursday.

New York gold futures moved from Friday to Monday