Fosun Pharma recently released its 2021 annual report, the annual report data shows that the company's annual R & D investment of 4.975 billion yuan, an increase of 24.28%; of which, R & D expenses of 3.834 billion yuan, an increase of 1.039 billion yuan, an increase of 37.17%, such a large R & D investment directly approached Hengrui Pharmaceutical.

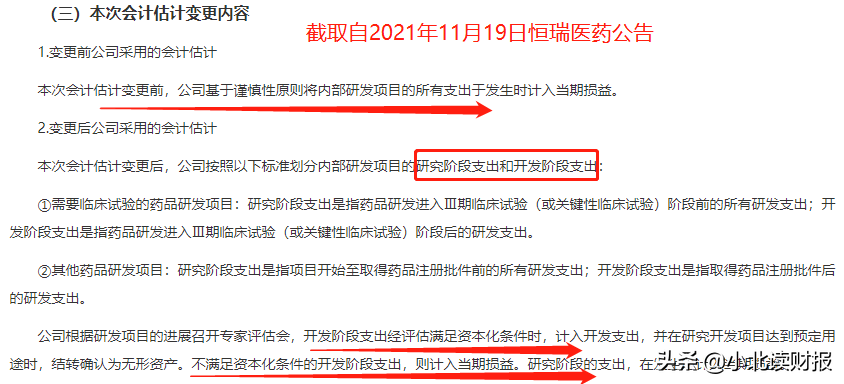

Although Hengrui Pharmaceutical has not yet released its 2021 annual report, according to the company's announcement, Hengrui Pharmaceutical, which has been investing in R&D for 20 years as the profit and loss of the current period, also revised its own accounting estimate change in November 2021 because of "forced performance pressure", proposing that when the expenditure in the development stage of the R&D project meets the conditions for capitalization, it will be included in the development expenditure, and when the R&D project reaches the intended purpose, it will be carried forward and recognized as an intangible asset, which will lead to a significant reduction in the R&D expenses on hengrui pharma's books.

It can be said that Fosun Pharma not only has money, but also nearly 4 billion yuan of R & D expenses are also solid, as of 2021, the company's R & D expense rate reached 9.83%.

Today we will focus on Fosun Pharma's R&D investment to see what this big pharmaceutical company is doing?

First, Fosun Pharma's research and development achievements are remarkable, helping enterprises get rid of the dilemma of collection and procurement

Fosun Pharma's R&D achievements we can know a little bit from the company's performance in 2021, in the context of large-scale collection of generic drugs, Fosun Pharma's new products have promoted the performance growth of the company, making it successfully get rid of the dilemma faced by the collection.

In 2021, Fosun Pharma achieved operating income of RMB39.005 billion, an increase of 28.7% year-on-year, net profit of RMB4.735 billion, an increase of 29.28% year-on-year, and non-net profit of RMB3.277 billion, an increase of 20.6% year-on-year.

Among them, from the perspective of the income structure of the enterprise, the main business pharmaceutical sector has performed prominently, and the growth rate of foreign business income is relatively fast.

Specifically, the anti-infection core products and anti-tumor and immunomodulatory core products under the pharmaceutical business contributed the main force, of which the net revenue of anti-infection core products increased by 4.681 billion yuan, and the net revenue of anti-tumor and immunomodulatory core products increased by 2.331 billion yuan.

The substantial increase in the revenue of anti-infective core products is mainly due to the growth of the revenue of Fubitai (mRNA new crown vaccine, licensed introduction pipeline) in Hong Kong, Macao and Taiwan and the growth of other anti-infective drugs, and The cumulative vaccination of Fubitai in Hong Kong, Macao and Taiwan exceeds 20 million doses (the mainland is in the second phase of clinical practice), which has become a blockbuster variety of enterprises with more than 1 billion yuan;

mRNA new crown vaccine is considered to be the most expensive vaccine of various vaccine types at present, and the authorized introduction of this vaccine is the German BioNTechSE, whose 1 dose of vaccine is purchased by the US government at a purchase price of about 19.5 US dollars, so it is not excluded that Fubitai has contributed more than 2 billion yuan to Fosun Pharma's total revenue.

In addition, the operating income growth of anti-tumor and immunomodulatory core products is mainly due to the growth contribution of self-developed products Such as Hanlikang (rituximab injection) and Hanquyou (trastuzumab for injection), in 2021, Hanlikang achieved revenue of 1.69 billion yuan and net revenue growth of 940 million yuan, and Hanquyou achieved revenue of 930 million yuan and net revenue growth of 790 million yuan;

Hanlikang is the first domestic biosimilar approved for marketing (approved in May 2019); Hanquyou is the first domestic approved biosimilar of trastuzumab (approved in August 2020), and it is also the first domestic monoclonal biosimilar in China and Europe.

Note: Biosimilars are not bioinductives.

It has to be said that for Fosun Pharma, although due to the epidemic situation, joining medical insurance and other reasons to promote the rapid release of these blockbuster products, the essence lies in the high value of product research and development, that is, whether it is an imported licensed product (mRNA new crown vaccine) or a self-developed biosimilar product (not the first of the same kind), Fosun Pharma relies on its R&D investment to keep itself at the forefront of domestic research and development.

In January and March 2022 this year, Fosun Pharma, as a domestic enterprise, successively obtained the qualifications of merck's imitation of the new crown oral drug Molnupiravir and Pfizer's new crown oral drug Paxlovid, and the only domestic enterprises that obtained the qualification of two new crown oral drug imitation qualifications were Fosun Pharma and Shanghai Disano, providing Paxlovid generic drugs to 95 low- and middle-income countries/regions.

It is worth mentioning that although generic drugs may not bring higher profits to Fosun Pharma, Fosun Pharma's recent stock price performance is indeed due to the new crown generic drugs and the new crown mRNA vaccine;

Because the evolution of the epidemic is still uncertain, the only thing we are sure of is the fact that Fosun Pharma "has epidemic-related prevention and treatment drugs".

We believe that it is Fosun Pharma's internationalization that has helped it obtain the license of these two generic drugs, compared with Hengrui Pharma, Fosun Pharma's international revenue in 2021 has reached 13.599 billion yuan, but Hengrui Pharma's foreign revenue in 2020 is only 758 million yuan.

2. Fosun Pharma's business layout and R&D pipeline outlook

Fosun Pharma's R&D is also a considerable part of the introduction, which makes me think of Huadong Pharma, which practices the "buy, buy and buy" strategy, Fosun Pharma has also begun to lay out medical beauty business in the past two years, but the two give people a different feeling, Huadong Pharma's R&D strength is not as strong as Fosun Pharma, and the focus of drug R&D innovation is insufficient.

Therefore, even if Fosun Pharma has a lot of R&D introduction pipelines, its self-developed innovative drug pipelines are still worth looking forward to;

And because of the company's self-research strength, the R&D efficiency and success rate of the projects licensed may be higher.

(As of the end of 2021, Fosun Pharma mainly has the number of drugs under research, for details, please refer to Fosun Pharma's 2021 annual report.) )

However, as of the end of 2021, the number of innovative drugs listed by Fosun Pharma is not much, still inferior to Hengrui Pharma, and because of the introduction of licensing projects, the profitability is weaker than that of Hengrui Pharma, but the company is catching up with the pace of R&D of Hengrui Pharma, which is the current gap between Hengrui Pharma and Fosun Pharma.

However, although the number and speed of fosun Pharma's new drug listing lag behind Hengrui Pharma, we believe that Fosun Pharma also has one of its advantages, that is, it has more biological drug pipelines, whether it is biosimilars or bio-innovative drugs, Hengrui Pharma's biological drug pipeline is not so dense.

Therefore, based on the two characteristics of biological drugs, the research and development barriers are higher and the prospects are broader, perhaps like a longer period of time to see, Fosun Pharma will not be worse than Hengrui Pharma.

In 2021, Fosun Pharma has obtained a total of 6 product registration approvals (through marketing approval), all of which are biological products, including 5 therapeutic biological products and one preventive biological product, which may be the reason why Fosun Pharma has not been greatly affected by the collection: its chemical drug research and development is not so strong.

In the first half of 2021, Hengrui Pharmaceutical obtained a total of 14 registration approvals for drugs, including two chemical innovative drugs (Class 1), 7 other chemical drugs, and 3 biological products.

Third, to sum up

In general, through the analysis of Fosun Pharma's R&D achievements and research pipelines, we have found many of its advantages, that is, although there is still a big gap between the R&D amount and the R&D speed of Hengrui Pharma, Fosun Pharma also has its own advantages, including more mature internationalization, seizing the opportunity of the new crown epidemic, and more adequate biological drug R&D pipelines, which not only makes it avoid the risk of collection in the past two years but also continuously releases new vitality, looking forward to a farther future, perhaps Fosun Pharma will not necessarily be worse than Hengrui Pharma. What do you think? Welcome to talk to me ~~