The world's top ten cosmetics companies have raised 879.2 billion yuan a year, an increase of 10% year-on-year.

Wen 丨 Li Shuo

On March 10, Brazilian cosmetics giant Natura & CO released its 2021 financial report. At this point, the results of the world's top cosmetics companies in fiscal 2021 have all been announced, and the world's top ten cosmetics companies have been released.

Natura & CO's revenue last year was 40.2 billion reais (about 50.6 billion yuan), up 8.8% year-on-year, and sales of its Brands such as Avon, The Body Shop and Aesop all recorded growth.

At the same time, the 50.6 billion yuan revenue also makes the Brazilian cosmetics company ranked seventh in the world after Shiseido (57 billion yuan), and is the only company headquartered in an undeveloped country among the world's top ten cosmetics companies.

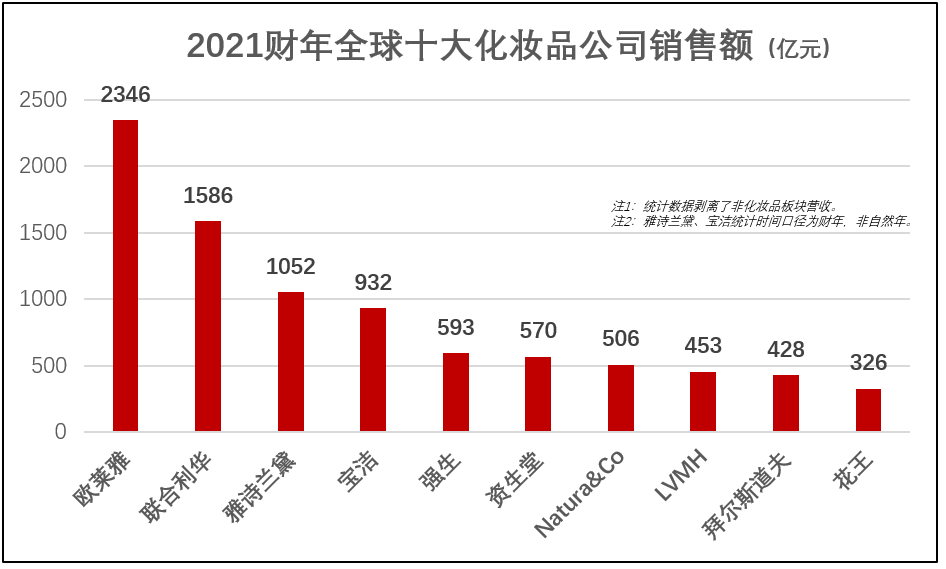

According to the statistics of "Cosmetics News", after the divestiture of non-cosmetics business, in fiscal 2021, the top ten cosmetics companies in the world by revenue are L'Oréal, Unilever, Estée Lauder, Procter & Gamble, Johnson & Johnson, Shiseido, Natura & CO, LVMH, Byersdorf, And Kao, and the total revenue of 10 companies reached 879.2 billion yuan.

In addition to the top ten, Coty's revenue in fiscal 2021 was 30 billion yuan, down 1.9%; driven by the snowflake show, Amorepacific's revenue of 28.3 billion yuan last year rose by 8%; Henkel's cosmetics business, which is composed of brands such as Swarco and Silk Yun, had revenue of 26.4 billion yuan in 2021, down 2%.

There was a lot of noise

In 2021, the cosmetics segment of the world's top ten cosmetics companies will have better revenue than in 2020.

Among them, LVMH has the fastest growth rate, and its cosmetics division, including Dior, Guerlain, Givenchy, Belle Fei, Freches and other brands, has seen a 27% year-on-year increase in revenue, and China's Hainan Duty Free has made an important contribution to this.

"We found in 2021 that although Chinese customers can't travel abroad, they buy more from LVMH than in 2019." BERNARD Arnault, chairman and chairman of LVMH, said.

In addition to LVMH, in fiscal 2021, L'Oréal, Estée Lauder, and Byersdorf all surpassed the 2019 years before the outbreak of the epidemic, and there is a commonality behind them: high-end brands drive growth.

In 2021, L'Oréal's high-end cosmetics division surpassed volkswagen cosmetics for the first time to become the group's largest division, with sales of 89.7 billion yuan, an increase of more than 20% year-on-year, and its Lancome Jingchun series, Helena, Uemura Shu and other strong performance.

Last fiscal year, Estée Lauder's Premium Skincare division saw net sales increase 28% year-over-year to $60.3 billion and operating profit of $19.4 billion, with Double-digit growth in Global Sales.

Last year, La Prairie, Eutherin and Aquaphor became key to Beiersdorf's growth, with La Prairie sales up more than 20% year-over-year.

Last year, based on the continuous growth of the Chinese market, LG's main brand Whoo's life and health brand increased by 12% year-on-year. Amorepacific's Innisfree and Itti House revenue declined, but the revenue of the high-end brand division represented by Snowflake Show and Hera increased by more than 20%.

Sold more expensive

Compared with LVMH and Estée Lauder, Procter & Gamble, Unilever, Kao and other companies that are known for their personal care business have revenue growth rates of less than 10% and lower net profit margins.

However, under the high-end winning rules and cost pressures, most companies have begun to take action and are committed to selling products more expensive. There are two main ways: 1. mergers and acquisitions of high-end brands; 2. price increases.

In the past few years, high-end brands represented by CPB, Shiseido, and NARS have become the main growth drivers of Shiseido. Last year, after setting high-end skin beautification as its core business, Shiseido sold Pomei, Za, Sanko, UNO and Mizunomi, and this year transferred its professional hairdressing business to Henkel.

In the past two years, Shiseido has successively sold nearly 20 popular cosmetics brands, and has also launched high-end brands such as Myoya no Hikari and Bohm.

In addition, Procter & Gamble acquired high-end skincare brand Tula Skincare and hair care brand Ouai; last year, Beiersdorf acquired the parent company of the lady-class beauty brand Chantecaille; and LVMH acquired century-old fragrance brand Officine Universelle Buly last year.

Unilever has prioritized its high-end cosmetics business of about $5 billion, most of which are acquired from mergers and acquisitions, including Dermalogica, Garancia, Tatcha and so on.

In addition to acquiring high-end brands, Unilever will also increase the price of its original product line. "The main challenge in 2021 is the sharp rise in costs." Unilever CEO Joanna Said Unilever responded with pricing action, with prices up 2.9% for the full year.

Procter & Gamble also said at the latest quarterly earnings report that in 2022, all ten major categories, including cosmetics, will raise prices. In addition, at the beginning of this year, brands such as Estée Lauder, Aquamarine Mystery, and Lancôme also reported price increases.

In addition to the rising costs of raw materials and transportation, global inflation is also an important reason for the collective price increase of cosmetics. According to data released by the U.S. Bureau of Labor Statistics, the U.S. CPI rose 7.5 percent year-on-year in January, the highest since March 1982.

The year of reorganization

Within the enterprise, change is also happening.

Layoffs, departures, restructuring... The personnel and organizational structure of international cosmetics companies is undergoing dramatic changes in the recent year.

In terms of business structure, in order to find new growth momentum outside of SK-II and OLAY, procter & Gamble announced the establishment of a high-end cosmetics division, Specialty Beauty, which will operate brands including Ouai, First Aid Beauty and SK-II's North American business.

Also due to business focus considerations, at the end of 2021, Johnson & Johnson announced plans to divest the consumer health business including Shirono Doctor, Dabao, Lu deqing and Avanade from the group and establish a new listed company.

Johnson & Johnson expects the new consumer health corporate structure to be completed by the end of 2022.

In January, Unilever announced that it would lay off around 1,500 jobs worldwide, and that its main business units would also be adjusted from three to five, namely Beauty & Health, Personal Care, Home Care, Nutrition and Ice Cream, with the five business units responsible for their respective global strategies, growth and profits.

It is reported that this simpler, focused organizational structure will be fully operational by 2020 and is expected to save the company about 4.3 billion yuan in costs within two years.

In contrast to Unilever's "split" initiative, Henkel plans to merge the cosmetics business unit, including Swarco, with the home care business unit to form the "Henkel Consumer Brand Business Unit". In this regard, Henkel believes that this move will allow Henkel to achieve significant synergies and efficiency gains, and will facilitate its future investment in innovation, sustainability and digitalization.

In terms of personnel changes, in October last year, Xu Min took over from Marius as chairman and CEO of P&G Greater China, and became the first locally trained CEO in P&G's history. A month later, Procter & Gamble's president and CEO was handed over to Jon Moller by David Taylor.

In February this year, Gao Xiangqin stepped down as president of Amorepacific China, and former vice president Huang Yongyu took over the baton. Since joining Amorepacific in October 2013, Gao Xiangqin has been at the helm of the Group's China team, and under his leadership, Amorepacific has achieved a huge breakthrough in its online layout in the Chinese market.

Also in February, L'Oréal USA CEO Spouthan announced his departure from L'Oréal Group, with David Greenberg taking over. Prior to his role as CEO of the United States, Spunhan served as CEO of L'Oréal China from 2016 to 2019, and promoted the accelerated implementation of L'Oréal China's digitalization and global localization transformation.

It is too early for Chinese companies to be shortlisted

In 2021, L'Oréal achieved double-digit growth in China, twice the growth rate of the global cosmetics market; in the past year, Estée Lauder's single-brand retail sales in China's online channels alone exceeded 10 billion yuan.

With the help of e-commerce channels, Kao, which owns brands such as Birou and Kerun, has achieved strong growth in China; Natura & Co is currently preparing for the full entry of its two brands, Aesop and The Body Shop, into the Chinese market. The Body Shop's first store in China may land in 2022...

At present, the strategic significance of the Chinese market to achieve the performance growth of global cosmetics companies needs no further explanation.

Overall, among the world's top 10 cosmetics companies, there are 3 cosmetics companies in the United States, 2 in France, 1 in the United Kingdom, 2 in Japan, 1 in Germany, and 1 in Brazil, however, China, as the world's second largest cosmetics market, has not yet been shortlisted.

If calculated according to the threshold of 30 billion yuan, there is still a big gap between Chinese cosmetics companies and international giants, among the local listed cosmetics companies, Shanghai Jahwa predicts that the revenue in 2021 will be 7.6 billion yuan; Yixian e-commerce revenue will be 5.8 billion yuan last year; Bloomage Bio's revenue will be about 4.9 billion yuan; Polaria estimates 4.5 billion yuan; bethany's revenue is expected to exceed 4 billion yuan.

In the next three years, for local cosmetics companies, it may be more realistic to break through the revenue threshold of 10 billion yuan first.