On March 2, Zaiding Pharmaceutical Hong Kong Stock released its 2021 annual report.

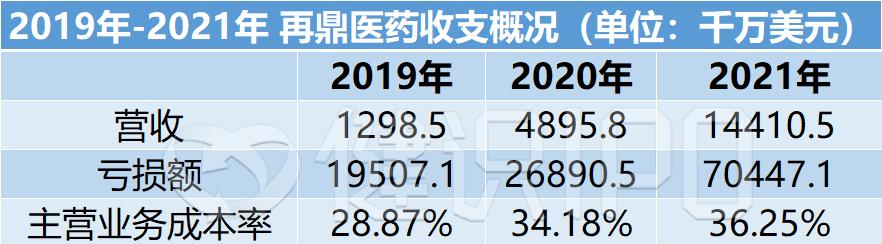

In 2021, zaiding pharmaceutical total revenue of 144 million US dollars, an increase of 194.77% year-on-year, but it is still far from profitability, in 2021 Zaiding loss of 704 million US dollars, an increase of 161.98% year-on-year.

On the day the news was issued, Zaiding Pharmaceutical's Hong Kong stocks plunged 9.83%, and the US stocks fell slightly by 0.04%; on March 3, Zaiding Hong Kong stock prices rebounded.

How should the License in model go in China?

It has been losing money for 9 years, and the licensing fees have remained high

Zaiding's annual report is very frank: "Since our establishment in 2013, we have not made a profit and have lost money in all periods. ”

In 2021, zaiding pharmaceutical's total revenue was 144 million US dollars, up 194.77% year-on-year. While revenue is rising, spending is also increasing. Among them, the main business cost was 522 million US dollars, an increase of 212.14% year-on-year; research and development expenses were 573 million US dollars, an increase of 157.42% year-on-year; operating costs were 219 million US dollars, an increase of 96.59% year-on-year.

The difficulty of balancing the payments has led to the continuous expansion of Zaiding Pharmaceutical's losses, from $269 million in 2020 to $704 million.

The reasons for the continuous expansion of Zaiding's total loss are worth exploring. From the book figures, the rapid growth of R&D expenses is a major reason for the continuous expansion of Zaiding Pharmaceutical's losses, rising from $223 million last year to $573 million. Among them, the sharp rise in licensing expenses has become the main reason for the growth of research and development expenses, which is the main cost of License in.

In 2020, Zaiding Pharma's licensing fee was US$108 million, and in 2021, this expense increased by 255.1% to US$384 million, accounting for 67% of the annual R&D expenditure.

The increase in licensing fees is closely related to the continuous introduction of Zaiding Pharmaceutical. According to the annual report, even though the License in model has cooled down a lot in China, the leader Zai Ding Pharmaceutical still built 8 new partnerships to further expand the authorized product pipeline.

At the same time, the proportion of main business costs increased from 28.87% in 2019 to 36.25% in 2021, which also had an impact on the profit and loss of Zaiding Pharmaceutical.

Is License in a pseudo-proposition?

Zaiding not only has License in, but also has self-research. But in China, Zaiding is undoubtedly the commercial innovation leader of the License in model. If the frontrunner on one track does not perform well, the industry may start to wait and see for the entire track.

When he started, Zaiding Pharmaceutical held the License in pipeline. According to Zaiding's plan, it is necessary to take the profits of the imported products to feed back and develop themselves, so as to achieve a virtuous circle and maximize economic benefits.

At that time, domestic innovative pharmaceutical companies had just emerged, and Zaiding Pharmaceutical did go faster with the License in model, and successfully landed on nasdaq in 2017. After three years of listing, Zaiding's US stock price rose by more than 300%; after Zaiding landed in Hong Kong stocks in 2020, its stock price also rose from HK$602 to HK$1512, and it was even called "the most expensive Hong Kong stock".

In April 2021, Zai Ding Pharmaceutical completed a round of global additional issuance, raising US$858 million. However, the good times are not long, in the second half of 2021, since the sci-tech board rejected the Haihe drug IPO, the domestic view of the License in model has changed.

It was also from that time that Zaiding's stock price went all the way down.

Zaiding Pharmaceutical Hong Kong stock trend

Zaiding Pharmaceutical's external caliber has also begun to change, from the "1.0 era of introducing mature products" to the "2.0 era of introduction + research and development".

Iteration takes time, and all the market can see at the moment is performance. In 2021, zaiding pharmaceuticals will achieve commercialization of four products, all of which are imported products, namely PARP inhibitor "Zele", tumor electric field treatment "Aipu Dun", gastrointestinal stromal tumor targeting drug "Qingle", and anti-infective drug "Nu zaile".

"Zele" has been included in the national medical insurance, and the sales amount in 2021 is 93.579 million US dollars. In the same year, AstraZeneca sold $1.13 billion in the world's PARP inhibitor Olapally in china, and its new generation of PARP inhibitor AZD5305 has opened clinical trials in China. In addition, the domestic counterparts of similar drugs also include Hengrui Pharmaceutical, BeiGene and so on.

In fact, the backbone of zaiding pharmaceutical commercialization comes from well-known multinational pharmaceutical companies such as AstraZeneca, Roche, Novartis and BMS. However, from the full year of 2021, the luxury configuration did not bring corresponding market surprises.

Also regarded as a representative of innovative pharmaceutical companies, and the introduction of beiGene with self-research revenue of 1.2 billion US dollars in 2021, the loss narrowed by 13%; followed by Zaiding's "little brother" Cstone Pharmaceutical, the 2020 revenue has exceeded the 1 billion yuan mark, although it is also a loss, but the revenue capacity is stronger than Zaiding Pharmaceutical.

Internal iteration takes time, external opponents are not weak, and the current Zaiding needs better wisdom and efficiency: if you can't rely on self-developed products to "make blood", it is difficult to get out of the high-cost introduction model. But from introduction to introduction + self-research, it will not be easy for any company.

How does the License in model run more calmly and better in China's pharmaceutical innovation environment? The track desperately needs more good news.