The Paper's reporter Jiang Mengying

At 3:00 a.m. Beijing time on December 16, the Federal Reserve Open Market Committee announced that it would keep the target range of the federal funds rate unchanged at 0-0.25%, in line with market expectations.

At the same time, the Fed removed the phrase "inflation expectations are temporary" from its statement and replaced it with "the imbalance between supply and demand associated with the pandemic and the reopening of the economy continues to lead to higher inflation rates." ”

The Fed said it decided to reduce its monthly net worth of U.S. Treasury bonds and $10 billion less net assets for institutional mortgage-backed securities in light of inflation and further improvements in the labor market. Starting next January, the commission will increase its holdings of at least $40 billion in U.S. Treasuries and at least $20 billion in institutional mortgage-backed securities each month, and will complete the bond reduction in March. In November, the Fed said it decided to start reducing the net worth of monthly asset purchases of U.S. Treasuries by $10 billion and the purchase of institutional mortgage-backed securities by $5 billion.

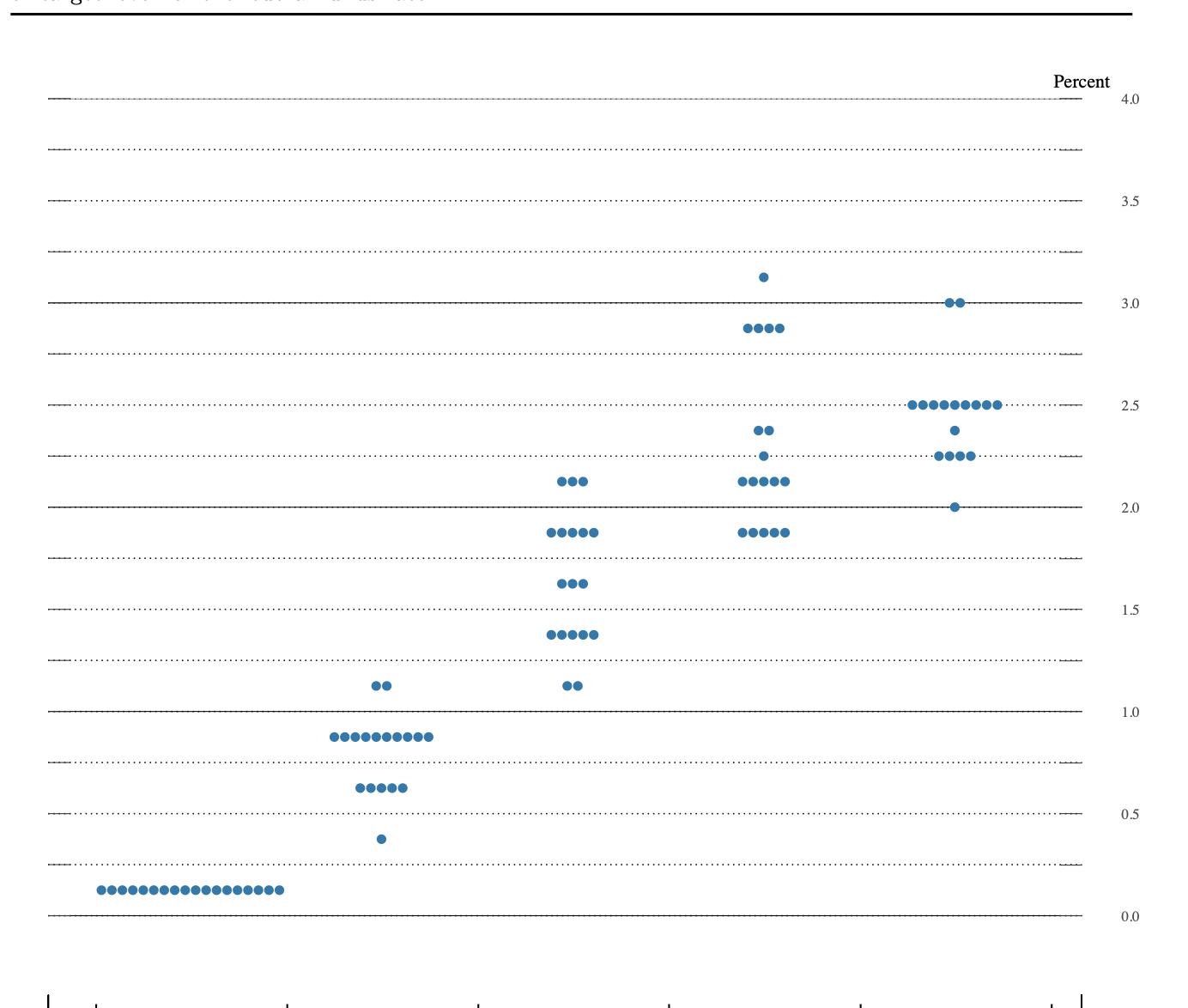

The dot plot also shows that all 18 committee members are predicting a rate hike in 2022, 1 member is predicting a rate hike, 5 members are predicting 2 hikes, 10 members are predicting 3 rate hikes, and 2 members are predicting 4 rate hikes. In September, nine committee members predicted a rate hike in 2022, while another nine members maintained their expectations for 2023.

Compared with September, the Fed further cut the US economic growth rate this year to 5.5% (5.9% of the September forecast) and recovered to 4.0% in 2022 (3.8% of the September forecast). The unemployment rate is expected to be 4.3% this year (4.8% forecast for September this year) and 3.5% in 2022 (3.8% for September this year). Further sharply increase PCE (personal consumption expenditure) inflation to 5.3% (4.2% forecast for September this year) and will fall back to 2.6% in 2022 (2.2% forecast for September this year). Core PCE inflation rose to 4.4% this year (3.7% forecast for September this year) and will be 2.7% in 2022 (2.3% forecast for September this year).

The following is the full text of the statement and how it compares to the November statement:

The Fed is committed to using all its tools to support the U.S. economy, thereby achieving its goal of promoting maximum employment and price stability.

With vaccine rollout and strong policy support, indicators of economic activity and employment continue to be strong. (November original: Indicators of economic activity and employment are strong.) The industries hardest hit by the pandemic have also improved in recent months, but the rise in COVID-19 cases in the summer has slowed the recovery (original for September: but the rise in COVID-19 cases has slowed the recovery). Job growth has been solid in recent months and unemployment has fallen sharply. The imbalance between supply and demand associated with the pandemic and the reopening of the economy continues to lead to higher inflation. (November original: Rising inflation levels largely reflect the fact that expectations are temporary.) The imbalance between supply and demand associated with the COVID-19 pandemic and the reopening of the economy have led to significant price increases in some sectors. Overall, financial conditions have continued to ease, partly reflecting the effects of policies that support the economy and credit flows into U.S. households and businesses.

The economic return to the right track continues to depend on the spread of the virus. Progress in vaccination and easing of supply constraints are expected to support continued growth in economic activity and employment, as well as lower levels of inflation. Risks to the economic outlook remain, including from new variants of the virus. (November: Risks to the economic outlook remain.) )

The Commission seeks to achieve maximum employment and a 2% inflation target over the long term. In support of these goals, the Committee decided to keep the target range of the federal funds rate at 0-0.25%. Since inflation has been in excess of 2 per cent for some time, the Commission expects that it will be appropriate to maintain this target range until labour market conditions reach levels consistent with the Commission's assessment of maximum employment. (November original: As inflation remains below this long-term target, the committee will work to get inflation moderately above 2 percent for some time to come, thereby bringing inflation to an average of 2 percent, with long-term inflation expectations anchored at exactly 2 percent.) The Committee wants to maintain an accommodative stance on monetary policy until these targets are reached. The Committee decided to maintain the federal funds rate at 0-0.25% and considered it appropriate to maintain this target range until labor market conditions reached the maximum employment level assessed by the Commission and inflation rose to 2% and will moderately exceed 2% for some time to come. Given the development of inflation and further improvements in the labor market, the commission decided to reduce its net worth of monthly purchases of U.S. Treasury bonds by $20 billion and its net worth of institutional mortgage-backed securities by $10 billion. (November original: Given the substantial further progress the economy has made in meeting the Commission's goals since last December, the Commission decided to begin reducing the net assets of monthly asset purchases of U.S. Treasury bonds by $10 billion and the net assets of institutional mortgage-backed securities by $5 billion.) Starting in January, the commission will increase its holdings of at least $40 billion per month in U.S. Treasury bonds and at least $20 billion per month in institutional mortgage-backed securities. The Committee judged that a similar monthly reduction in the rate of net asset purchases might be appropriate, but that it was prepared to adjust the pace of purchases if the economic outlook changed. (November original: Starting later this month, the commission will increase its holdings of at least $70 billion in U.S. Treasury bonds and at least $35 billion per month in institutional mortgage-backed securities.) Starting in December, the commission will increase its holdings of at least $60 billion per month in U.S. Treasury bonds and at least $30 billion per month in institutional mortgage-backed securities. The Committee judged that a similar monthly reduction in the rate of net asset purchases might be appropriate, but that it was prepared to adjust the pace of purchases if the economic outlook changed. The Fed's ongoing purchase and holding of securities will continue to facilitate the smooth running of the market and accommodative financial conditions, thereby supporting credit flows to households and businesses.

In assessing a suitable monetary policy stance, the Committee will continue to monitor the impact of future economic data. If risks arise that prevent the Achievement of the Committee's dual objectives, the Committee will be prepared to adjust the appropriate monetary policy stance. The Committee's assessment will take into account a wealth of information, including public health, labour market indicators, inflationary pressures and inflation expectations indicators, and data on financial and international developments.

The votes were: Jerome H. Powell, Chairman of the FOMC Committee (Fed Chairman); John C. Williams, Vice Chairman of the Committee (New York Fed Chairman); Thomas I. Barkin, Chairman of the Richmond Fed; and Raphael W. Bostic, President of the Atlanta Fed. ;(Febal Governor) Michelle W. Bowman; (Fed Governor) Lael Brainard; (Fed Governor) Richard H. Clarida; San Francisco Fed President Mary C. Daly; Chicago Fed President Charles L. Evans ;( Fed Trustee) Randal K. Quarles; (Fed Governor) Christopher J. Waller。

Editor-in-charge: Zheng Jingxin Photo Editor: Shen Ke