Financial Associated Press (Shanghai, editor Xiaoxiang) - Those who have long hoped to lower their national currencies to stimulate economic growth, senior central bank officials, who have long hoped to depress their currencies, are now counting on exchange rate appreciation to help combat the threat of inflation – this unusual scene presented by the global foreign exchange market at the beginning of 2022 is making many people in the industry sigh...

Almost 11 years ago, Brazil's finance minister, Guido Mantega, accused rich countries of launching a "currency war": by lowering interest rates and devaluing their currencies to lift their economies out of recession, while countries like Brazil, which have a relatively small voice in the foreign exchange market, have to bear the bitter fruit of currency appreciation.

But today, countries are taking very different approaches than they were a decade ago.

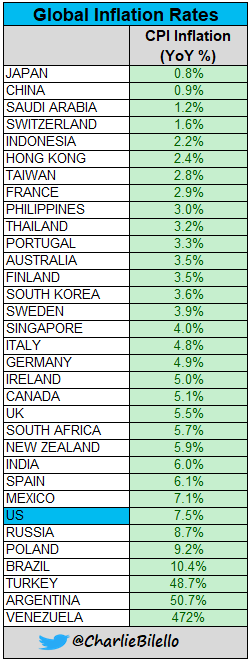

Rising inflation has replaced sluggish economic growth and has become the primary concern for many economies – while the year-on-year increase in the U.S. CPI reached 7,5% in January to refresh the nearly 40-year high, people in many parts of the world are also suffering from inflation: the CPI in Germany has reached 4.9%, the CPI in the UK has reached 5.5%, the CPI in Brazil has exceeded 10%, and the CPI in Turkey is close to 50%....

Against this backdrop, the exchange rate seems to be the most immediate and direct intervention for countries: an appreciation of the local currency can make imports cheaper, thereby helping to drive down domestic prices.

In other words – the higher you stand in the forex market, the less likely you are to be overwhelmed by the "tsunami" of global inflation.

Goldman Sachs: The world is fighting a reverse currency war

According to Bloomberg's SHOK model, if the dollar rises by 10% on a trade-weighted basis in the second quarter, U.S. inflation is expected to be depressed by 0.4 percentage points over the next two quarters. And if the euro appreciates by 10% on a similar trade-weighted basis, the suppression of eurozone inflation will be more pronounced.

Although neither Federal Reserve Chairman Jerome Powell nor ECB President Christine Lagarde and other global central bankers endorse the recent appreciation of local currencies, they have not backed it.

As a result, strategists at Goldman Sachs and many other Wall Street institutions believe that a "reverse currency war" may be playing out, with central bank policymakers using exchange rate appreciation to find tools to curb inflation.

George Cole, head of Interest Rate Strategy for Europe at Goldman Sachs, said this week that "the big shift is that people no longer think that local currency appreciation is undesirable." I wouldn't be surprised if we increasingly see G10 central banks recognize that strong currencies in this tightening cycle could actually be your friend. ”

In a client report this week, Cole and his colleague Michael Cahill also hinted that as the Fed tightens monetary policy harder than previously expected, other central banks will try to keep pace to keep up with the pace so as not to move their currencies lower.

Goldman Sachs estimates that major central banks would need to raise interest rates by an average of about 10 basis points to offset a 1 percentage point increase in the trade-weighted exchange rate. This "new model" of resistance to currency depreciation should be most beneficial to the euro, the Swedish krona and the Swiss franc.

Bank of America strategist Shusuke Yamada and economist Izumi Devalier also wrote in a report this week that "no one wants the local currency to depreciate while costs drive inflation." ”

(The outperform of many emerging-market currencies during the year released the expected us dollar for interest rate hikes)

How should countries manage the "red line"?

The exchange rate could also become a topic of conversation as G20 central bank governors and finance ministers hold online and face-to-face meetings in Jakarta this week, with senior G20 political and economic officials releasing a communiqué on the meeting on Friday. Officials last met in October and said they would examine "temporary" price pressures, but the term has now been deprecated by the Fed.

It is worth mentioning that the exchange rate has always been a sensitive topic among governments, and all countries do not want to be accused of stimulating trade by depressing the exchange rate of their local currency, and they do not want "beggar-thy-neighbor" competition. The impact of exchange rates is particularly important in smaller open economies such as Poland and Switzerland, as it will directly affect the performance of domestic inflation and economic growth in these countries.

SNB Governor Thomas Jordan's rare statement in December last year is undoubtedly worthy of "play" by market participants.

Jordan pointed out at the time that the strengthening of the Swiss franc had at least helped Switzerland avoid inflation spikes like those in the eurozone and the United States. "By allowing a certain degree of nominal appreciation, we have been able to prevent further inflation in Switzerland – which makes imports cheaper," Jordan said.

The remarks have come as a surprise to investors who have been familiar with the tone of the central bank's policies for many years: the SNB has long complained that the high Swiss franc exchange rate is a drag on the Swiss economy.

Adam Glapinski, governor of the Central Bank of Poland, has also recently said that he welcomes the strengthening of the Polish zloty to "support monetary tightening."

The Monetary Authority of Singapore, which uses the exchange rate as its main monetary policy tool, also unexpectedly announced tightening measures last month, saying it would slightly increase the appreciation rate of the Singapore dollar's nominal effective exchange rate (NEER) policy range, joining the ranks of the global fight against inflation, which pushed the Singapore dollar exchange rate to its highest level since October last year.

Aaron Hurd, portfolio manager at State Street Global Advisors, said, "The exchange rate is a key lever in monetary policy. Therefore, as part of the overall tightening cycle, these economies are right to tolerate or encourage the strengthening of their currencies. ”

Of course, if a different kind of "reverse currency war" does break out in the future, how countries can control the "red line" will obviously be worth the consideration of global policymakers.

To be sure, not every economy will enjoy an inflation buffer as a result of a stronger currency – much will depend on the composition of their inflation basket and local and domestic dynamics – such as wage growth. For economies that are particularly dependent on domestic services growth, local currency appreciation will not do much to curb inflation.

But for central banks that need to control prices, allowing local currencies to appreciate in combination with higher interest rates will be a key tool. Priyanka Kishore of Oxford Economics said it was expected to be a topic of conversation at the G20. "G20 officials are likely to discuss the potential impact of a hawkish shift in central banks in many major economies, especially as currency depreciations become an additional source of imported inflation."